What Is Delta Neutral Trading?

Delta neutral trading is a strategy where a trader constructs a portfolio with a net delta of zero. In options and derivatives theory, "delta" measures how much the value of a position changes for every $1 move in the underlying asset. A delta of +1 means your position gains $1 for every $1 BTC rises. A delta of -1 means you gain $1 for every $1 BTC falls.

When you combine positions so that their deltas cancel each other out, you reach delta neutrality. The portfolio no longer has meaningful directional exposure to price movements. Whether BTC pumps 20% or dumps 30%, your net P&L from price movement is close to zero.

This does not mean you earn nothing. Delta neutral traders earn from other sources: funding rates in perpetual futures markets, time decay in options, the spread between spot and futures prices, and volatility itself. The goal is to isolate these income sources while removing the random directional guess.

Delta neutral strategies are well established in traditional finance, but crypto has made them far more accessible and, in many cases, far more profitable. The reason comes down to the market's unique characteristics.

Why Delta Neutral Works in Crypto

Crypto markets create unusually favorable conditions for delta neutral strategies, primarily through three factors.

High and Persistent Funding Rates

Perpetual futures contracts do not expire. To keep them anchored to spot prices, exchanges use a funding rate mechanism: longs pay shorts (or shorts pay longs) every 8 hours. During bull markets, funding rates skew heavily positive because retail traders love to go long with leverage. Rates of 0.01% to 0.05% every 8 hours are common. At 0.01% per 8-hour period, that annualizes to roughly 10.95% APR. At 0.03%, you are looking at 32.85% APR, simply for sitting in a neutral position.

Extreme Volatility Creates Options Opportunities

Bitcoin regularly moves 5% to 15% in a single day. This level of volatility makes options expensive. When implied volatility is high, selling options (or structuring straddles and strangles) can generate premium income that far exceeds anything available in traditional markets. Delta neutral options strategies capture that elevated premium.

Futures Basis Gaps

Crypto futures often trade at a notable premium or discount to spot prices, especially quarterly contracts. This spread, called the "basis," is essentially free money for traders who can simultaneously hold spot and short the futures at the elevated price, then converge the two at expiry.

All three factors are driven by the same underlying reality: crypto markets have millions of highly leveraged, directionally biased retail participants. Delta neutral traders earn from being on the other side of that bias, without actually positioning against it.

Delta Neutral Strategy 1: Funding Rate Harvesting

Funding rate harvesting is the most accessible delta neutral strategy for most crypto traders. The mechanics are straightforward.

You buy the underlying asset on spot (gaining positive delta), then simultaneously open an equal short position on the perpetual futures contract (gaining negative delta). The two positions cancel each other out directionally. But you collect the funding payment every 8 hours from the long side of the perpetual market.

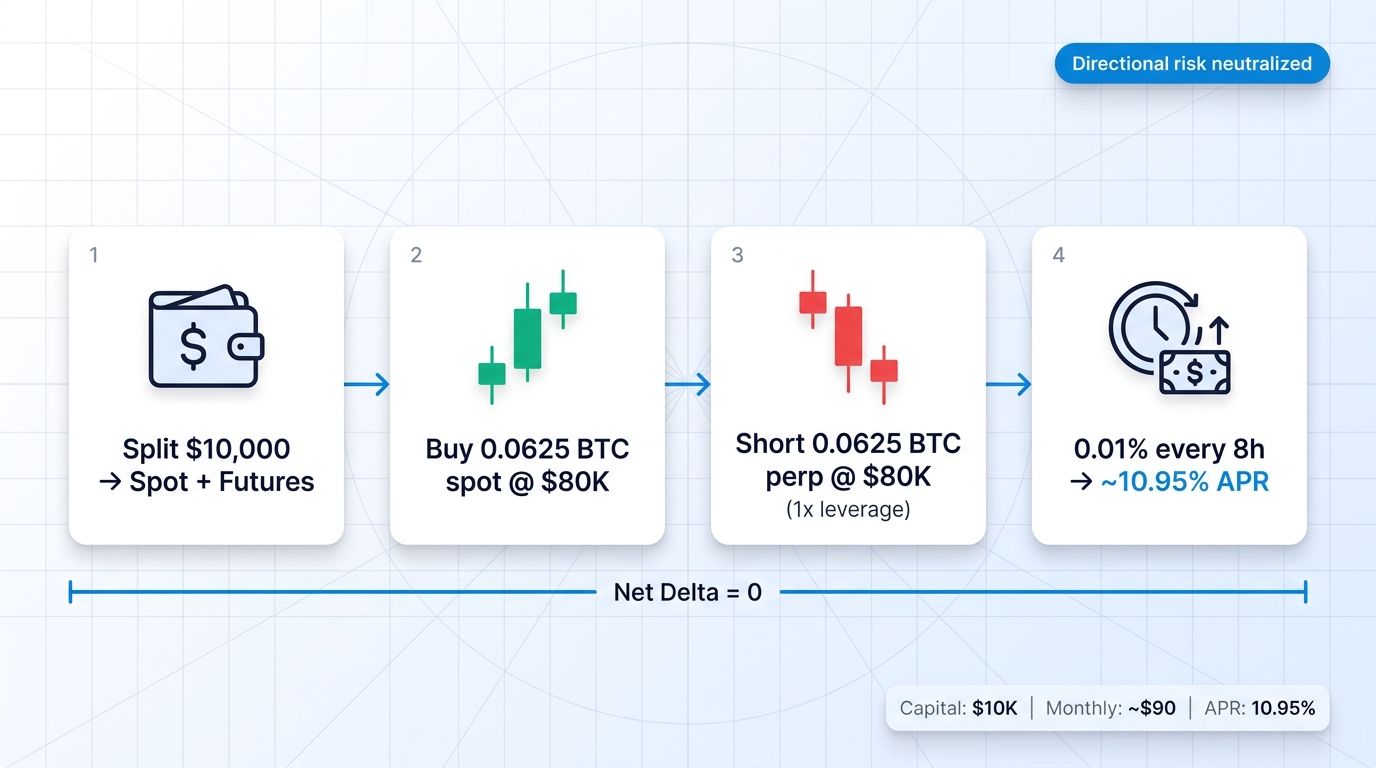

Step-by-Step Example with $10,000 Capital

Assume BTC is trading at $80,000.

1. Allocate $5,000 to purchase 0.0625 BTC on spot. 2. Allocate $5,000 as margin to open a short position of 0.0625 BTC on the perpetual futures contract. 3. Your net delta is zero: +0.0625 (spot) plus -0.0625 (perp) equals 0. 4. Current funding rate: 0.01% every 8 hours, paid by longs to shorts. 5. Your short position receives funding. Notional value of your short: 0.0625 BTC x $80,000 = $5,000. 6. Funding earned per period: $5,000 x 0.01% = $0.50 every 8 hours. 7. Daily earnings: $0.50 x 3 = $1.50. 8. Annual projection: $1.50 x 365 = $547.50 on a $10,000 position, or roughly 5.5% APR at a flat 0.01% rate.

When funding rates spike to 0.03% or 0.05% during bull markets, the same position can yield 16% to 27% APR. During peak bull cycles, rates have regularly exceeded 0.10%, pushing potential returns above 100% APR on the notional.

Monitoring and Rebalancing

The position is not fully set-and-forget. If BTC price rises significantly (say from $80,000 to $100,000), your spot holdings are now worth more in USD terms, but your short perpetual position has unrealized losses. The deltas can drift slightly due to leverage ratios, margin usage, and mark price differences. Traders should monitor the position daily and rebalance when the notional values diverge by more than 5% to 10%.

Different exchanges offer different funding rates at the same time. This creates a cross-exchange opportunity: if Exchange A pays 0.03% funding while Exchange B pays only 0.005%, a trader can hold spot on Exchange B and short the perp on Exchange A to capture the higher rate.

Delta Neutral Strategy 2: Options Straddle and Strangle

Options-based delta neutral strategies profit from large price movements in either direction, or from the passage of time when volatility is high.

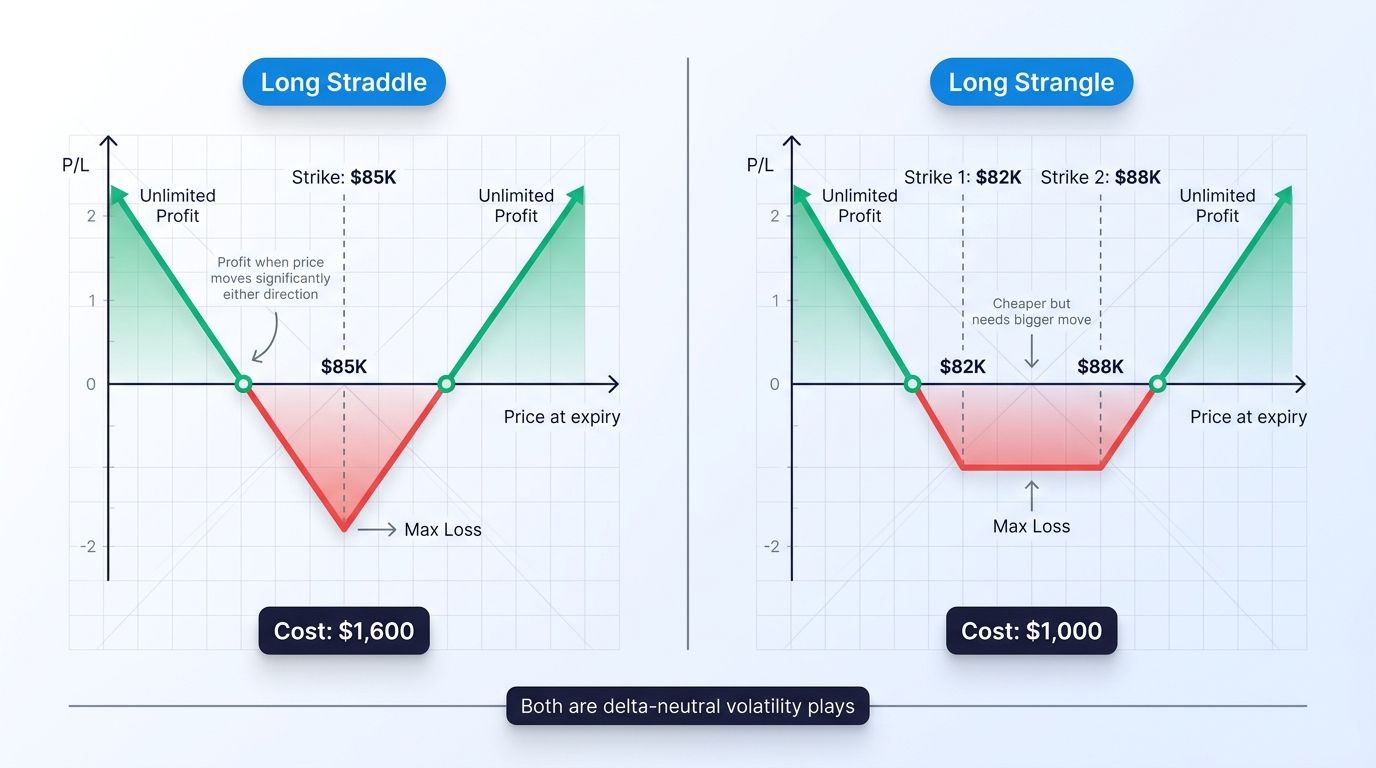

The Long Straddle

A long straddle involves buying a call option and a put option at the same strike price and expiry. At the time of purchase, the combined position is approximately delta neutral (the call has positive delta, the put has negative delta, and at-the-money options have roughly equal and opposite deltas).

If BTC makes a large move in either direction before expiry, one of the options gains enough value to cover the cost of both premiums. You profit from volatility itself, regardless of direction.

This strategy works best in crypto when you expect a major catalyst (a protocol upgrade, regulatory announcement, or macro event) but cannot predict which direction the market will move.

The Short Strangle

A short strangle involves selling an out-of-the-money call and an out-of-the-money put simultaneously. You collect premium upfront and profit if BTC stays within a range.

For example, with BTC at $80,000, you might sell a $70,000 put and a $90,000 call. You keep the combined premium as long as BTC stays between those strikes at expiry. The risk is that a large move beyond either strike can result in significant losses, so active management and defined stop-loss levels are essential.

Rebalancing Options Delta

As BTC price moves, the deltas of your options shift. A straddle that was delta neutral at $80,000 will develop directional bias if BTC moves to $85,000. Traders manage this by adding or reducing hedge positions (spot or perp) to bring delta back to zero. This is called "delta hedging" and requires active management, typically done daily or when delta drifts beyond a defined threshold.

Delta Neutral Strategy 3: Basis Trading

Basis trading, also called cash-and-carry arbitrage, captures the spread between spot prices and futures prices.

How the Spread Forms

Quarterly futures contracts in crypto often trade at a premium to spot. During bullish sentiment, traders pay a premium to lock in a long futures position. If BTC spot is $80,000 but the quarterly futures contract is priced at $82,400, a basis of $2,400 (3%) exists.

Executing the Trade

1. Buy 0.0625 BTC on spot for $5,000 (at $80,000 per BTC). 2. Sell 0.0625 BTC worth of the quarterly futures contract at $82,400, receiving $5,150 in notional value. 3. Hold both positions until futures expiry. 4. At expiry, futures converge to spot price. The $2,400 spread is captured as profit. 5. On a $10,000 total position, capturing a 3% basis over 3 months annualizes to roughly 12% APR.

The advantage of basis trading over funding rate harvesting is predictability. Basis is locked at entry. Funding rates fluctuate and can even go negative (meaning shorts pay longs), eliminating income or turning the position negative temporarily.

The disadvantage is capital lock-up until expiry and the opportunity cost if funding rate harvesting would have yielded more.

How to Set Up a Delta Neutral Position

The following is a practical walkthrough for a funding rate harvesting position using $10,000 in capital.

Step 1: Select Your Assets and Exchanges

Choose a liquid asset with consistently positive funding rates. BTC and ETH perpetuals typically have the most data history and tightest spreads. Review funding rate history across exchanges to identify where rates are highest.

Step 2: Divide Capital

Split $10,000 roughly 50/50: $5,000 for spot purchase, $5,000 for perpetual margin. The exact split depends on the leverage used on the perpetual side. At 1x effective leverage, a 50/50 split keeps the notional values matched.

Step 3: Open Both Legs Simultaneously

Buy 0.0625 BTC on spot at market price ($80,000). Immediately open a short perpetual position for 0.0625 BTC on the same or higher-rate exchange. Time is important here because price can move between legs and create unintended directional exposure.

Step 4: Verify Delta Neutrality

Confirm your long spot notional equals your short perp notional. Both should be approximately $5,000. Net delta should be zero.

Step 5: Record Entry and Set Monitoring Alerts

Note the entry prices for both legs, the initial funding rate, and the total cost (exchange fees, spread). Set price alerts for a 5% to 10% move in BTC so you know when to review the position for rebalancing.

Step 6: Collect Funding and Rebalance as Needed

Check funding payments every 8 hours. Rebalance the position if notional values drift significantly due to price movement. Close both legs simultaneously when you want to exit.

Risk Management for Delta Neutral Positions

Delta neutral does not mean risk-free. Several specific risks require active management.

Liquidation Risk on the Perpetual Leg

Your short perpetual position can be liquidated if BTC price rises sharply and your margin becomes insufficient. Never use high leverage on the short perpetual side. At 1x to 2x effective leverage, a 50% price increase would not cause liquidation. Add maintenance margin buffers and consider using cross-margin carefully.

Funding Rate Reversal

Funding rates can flip negative, especially during market downturns when traders scramble to short. A position designed to earn funding will instead pay funding when this happens. Monitor funding rates at least daily. If rates stay negative for more than a few periods, consider closing the position temporarily.

Execution Risk

Slippage between opening the spot leg and the perp leg can leave you with brief, unintended directional exposure. In fast-moving markets, a few seconds between leg execution can introduce meaningful P&L variance. Use limit orders where possible and execute during lower-volatility periods.

Rebalancing Frequency and Cost

Frequent rebalancing to maintain delta neutrality incurs transaction fees. On-chain or high-fee exchanges make this expensive. Factor in rebalancing costs when calculating net returns. A position earning 15% APR gross but requiring 5% in annual rebalancing fees nets only 10%.

Counterparty and Exchange Risk

Holding large balances on centralized exchanges introduces custodial risk. Diversifying across two or more reputable exchanges reduces single-point exposure. Never hold more than you can afford to lose at any single exchange.

Pros and Cons of Delta Neutral Trading

Advantages

Delta neutral strategies generate returns that are largely independent of market direction. During sideways or ranging markets where directional traders struggle, funding rate harvesters and basis traders continue earning steady income. The strategies can be highly capital-efficient when leverage is used carefully. The income streams (funding, basis, options premium) are mechanical and repeatable.

These strategies also reduce psychological stress. There is no need to predict whether BTC goes up or down next week. The focus shifts to execution quality, rate monitoring, and risk management.

Disadvantages

Delta neutral strategies require active monitoring, especially the perpetual short leg. Missing a funding rate reversal or an approaching liquidation level can turn a profitable position into a losing one quickly.

Returns can be limited during bear markets or low-volatility periods when funding rates collapse. Basis trading carries opportunity cost if the market moves strongly in one direction.

Options-based delta neutral strategies require deeper knowledge of Greeks and are less accessible to beginners. Rebalancing options positions incurs costs and requires real-time attention.

Finally, the strategies carry hidden correlation risk. In a severe market crash, exchange infrastructure can fail, spot and perp prices can diverge temporarily, and liquidity can disappear exactly when you need it most.

Execute Delta Neutral Strategies with Altrady

Managing a delta neutral portfolio across multiple legs, multiple exchanges, and multiple assets is operationally demanding. Keeping track of spot positions, perpetual shorts, funding accruals, and rebalancing triggers across tabs and spreadsheets is a recipe for errors.

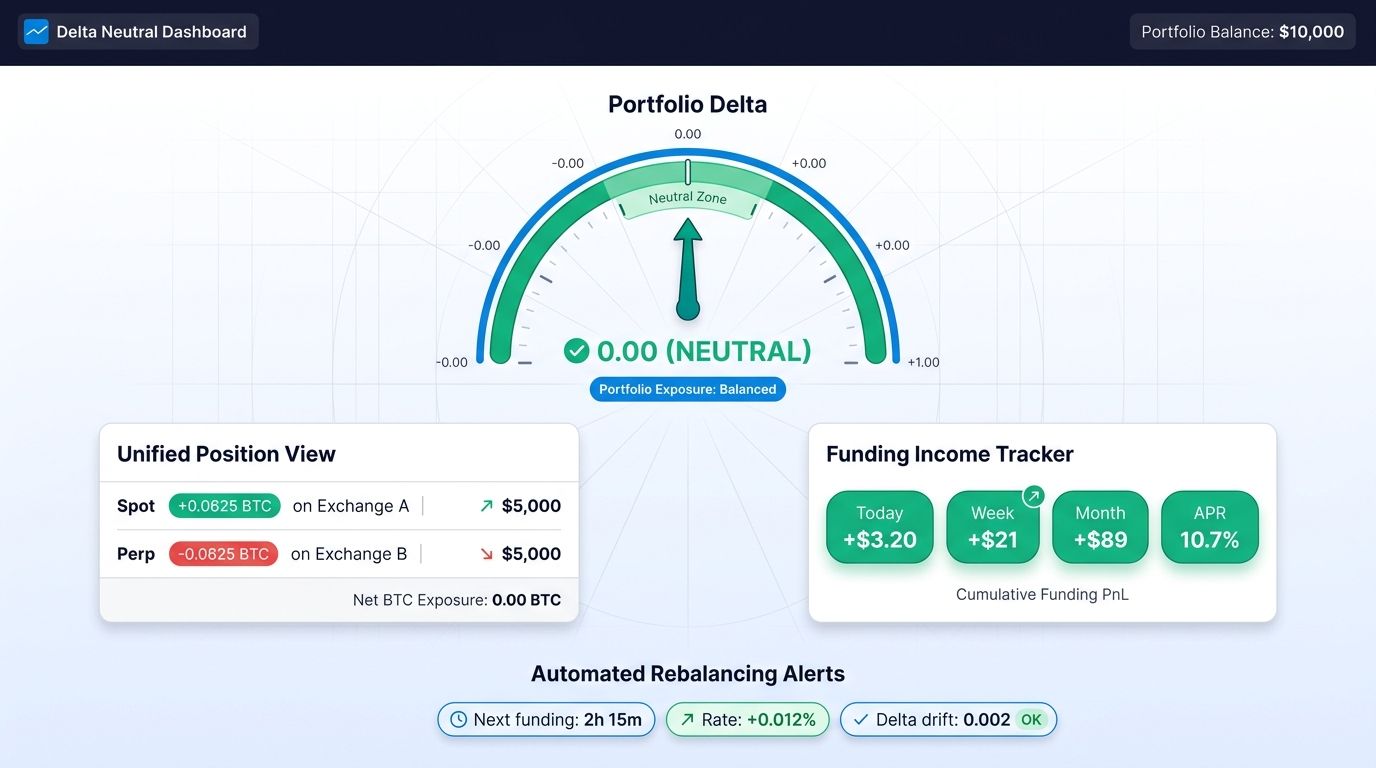

Altrady centralizes all of this. With Altrady's unified portfolio view, you can monitor all legs of your delta neutral position in a single dashboard, regardless of which exchanges hold each leg. Real-time P&L tracking lets you see exactly whether your position remains delta neutral or has drifted, so you know when to rebalance without guessing.

Smart order tools let you execute both legs of a new position near-simultaneously, minimizing the slippage and execution risk that can undermine delta neutrality at entry. Funding rate data aggregated across connected exchanges makes it easy to identify where rates are most favorable for your harvesting strategy.

Altrady supports multi-exchange connections, so you can place your spot leg on one exchange and your perpetual short on another, capturing the best rates across the market.

Start building and managing your delta neutral strategies with a free trial. See how much clearer and more controlled your execution becomes when all your positions live in one place.

Frequently Asked Questions

What does "delta neutral" actually mean in practice?

In practice, delta neutral means your portfolio has no meaningful profit or loss from the underlying asset moving up or down in price. You achieve this by combining positions with opposing deltas, such as a long spot position (positive delta) and a short perpetual position (negative delta) in equal notional amounts. The result is a portfolio that earns from other sources, like funding rates or basis, while being largely insulated from price direction.

How much capital do I need to start a delta neutral strategy?

There is no strict minimum, but practical considerations suggest starting with at least $1,000 to $2,000. Below that level, exchange fees, spread costs, and minimum order sizes can eat into returns significantly. The $10,000 example in this article represents a comfortable starting point that makes the math easier to manage and keeps fees as a small percentage of earnings.

What happens if funding rates go negative?

If funding rates go negative, your short perpetual position pays funding instead of receiving it. This turns your income stream into a cost. Most experienced traders set a rule to close or pause the position if funding turns negative for two or more consecutive periods. The spot position can be held or sold depending on your broader outlook. The key is to monitor rates daily and not assume they will remain positive indefinitely.

Can delta neutral trading guarantee profits?

No strategy in trading is guaranteed. Delta neutral trading reduces directional risk but introduces other risks including liquidation on the perpetual leg, funding rate reversals, execution slippage, and exchange risk. The strategies described here are designed to generate consistent income when market conditions are favorable, but they require active monitoring and risk management to remain effective.

How often do I need to rebalance a delta neutral position?

For a simple funding rate harvesting position, rebalancing is typically needed when the spot and perpetual notional values diverge by more than 5% to 10%, which usually happens after a significant price move. In calm markets, you might go days or weeks without needing to rebalance. For options-based strategies, delta hedging is more frequent and may be needed daily or after any 2% to 3% move in the underlying asset. The right frequency depends on your risk tolerance and the cost of rebalancing.