Berachain launched mainnet in early February 2025 with significant fanfare. The project had raised $100 million in venture funding, attracted a passionate community through its NFT-driven distribution model, and introduced a novel consensus mechanism called proof-of-liquidity. Then the price action turned brutal: BERA fell approximately 97% from its post-launch peak.

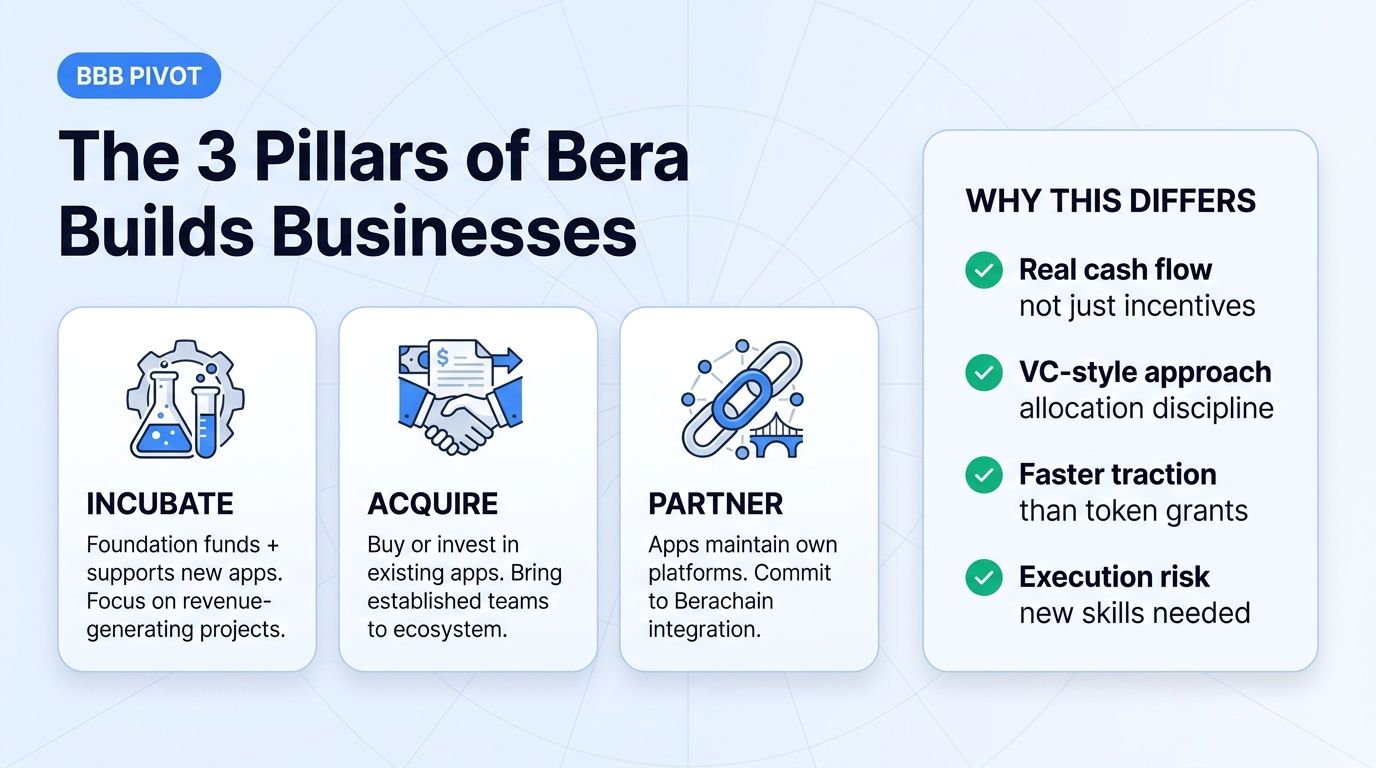

By May 2026, the Berachain Foundation announced a major strategic pivot called "Bera Builds Businesses" (BBB). The new model focuses on incubating, acquiring, or partnering with applications that generate real cash flow for the ecosystem, rather than relying on token incentives alone.

For traders, Berachain offers one of the more interesting comeback narratives of 2026. The technical foundation is sound. The community is committed. The macro environment for L1s is mixed but improving. And the strategic pivot, if executed well, could mark the turning point.

This guide explains what Berachain is, the proof-of-liquidity consensus mechanism, the tri-token system, what went wrong post-launch, the BBB pivot, and how traders should think about BERA exposure today.

What Is Berachain?

Berachain is an EVM-compatible Layer 1 blockchain with a unique consensus mechanism called proof-of-liquidity (PoL). The project was founded by a team operating under pseudonyms (Smokey the Bear, Papa Bear, and others maintaining bear-themed identities), reflecting the community's irreverent culture.

The project's technical architecture combines:

- EVM compatibility (smart contracts work identically to Ethereum)

- Proof-of-liquidity consensus (described below)

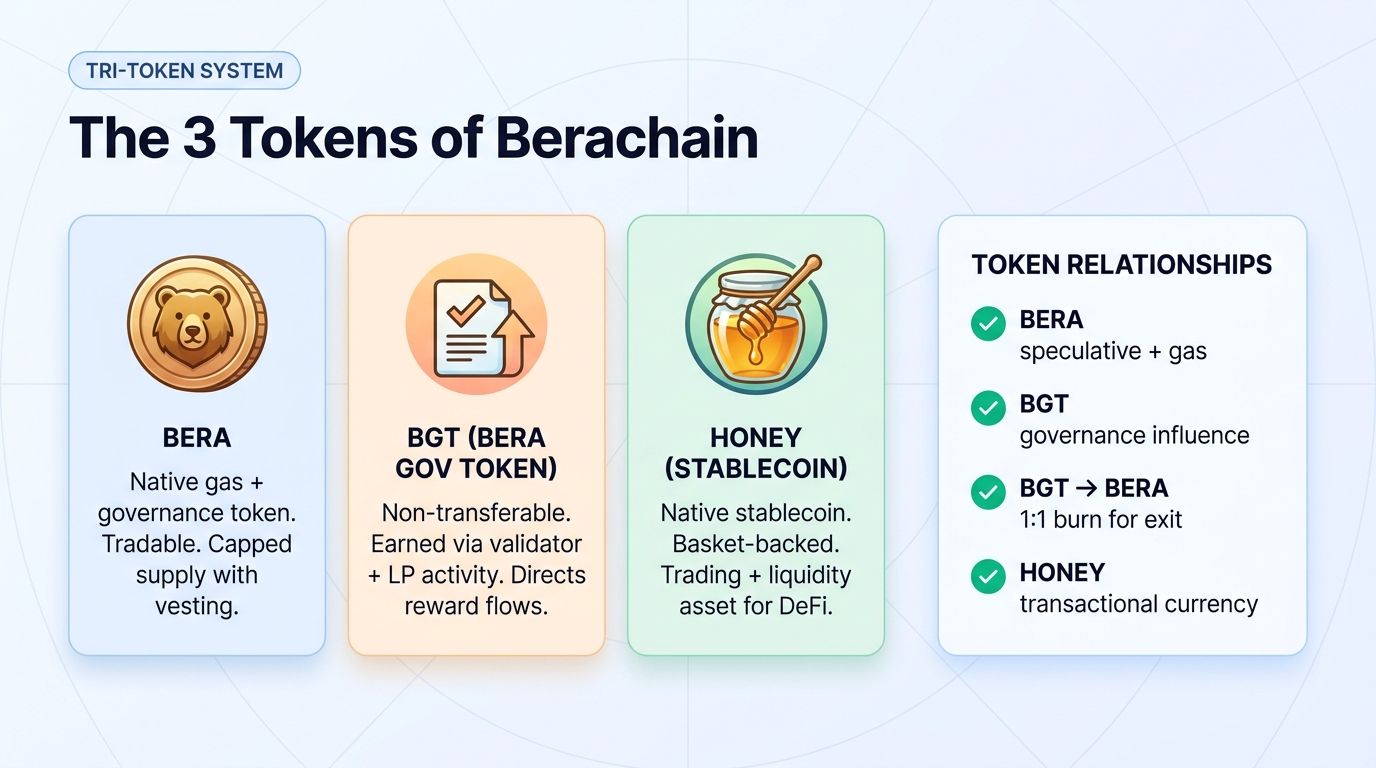

- Tri-token system: BERA (gas + governance), BGT (governance + liquidity rewards), HONEY (native stablecoin)

Berachain raised $100 million in funding from Polychain, Brevan Howard Digital, and others. The team has been technically credible from inception, with the foundation issues being market dynamics rather than technical execution.

Mainnet launched in February 2025 after extensive testnet phases and community building. The launch was technically successful, but token price action was difficult.

Why Berachain Matters

Three structural reasons.

First, proof-of-liquidity is a genuinely novel consensus mechanism. Most L1s use proof-of-stake (security through bonded tokens) or proof-of-work (security through computational expense). Proof-of-liquidity ties consensus security to actual liquidity providing in the network's DEXs. The mechanism aligns validators with the network's economic activity rather than just security.

Second, the tri-token system creates interesting economic dynamics. BERA, BGT, and HONEY each serve different functions, with carefully designed flows between them. The complexity creates more design surface than simpler L1s but also more opportunities for differentiation.

Third, the community is unusually committed. Berachain's NFT-driven early distribution attracted a passionate user base that remained engaged even during the 97% drawdown. Strong community is a real asset for L1 ecosystems and can support eventual recovery.

For traders, Berachain represents the higher-risk, higher-reward end of the L1 spectrum. The downside has largely played out; the question is whether the upside materializes.

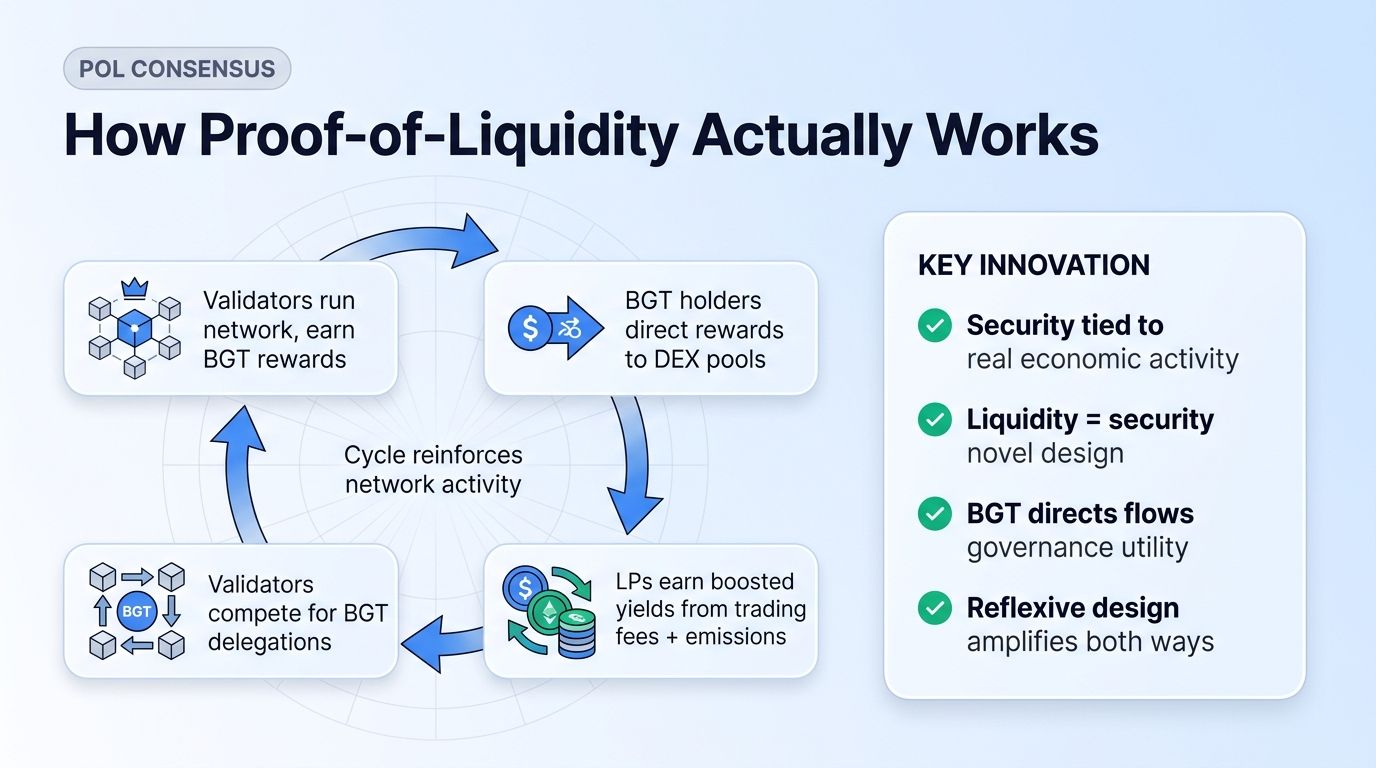

The Proof-of-Liquidity Consensus

Proof-of-liquidity (PoL) is the core innovation. The mechanism works as follows.

Step 1: Validators Run BGT-Earning Operations

Validators on Berachain run the network and earn block rewards in BGT (Bera Governance Token). The amount of BGT earned per block depends on the validator's bonded stake and performance.

Step 2: BGT Directs Liquidity Rewards

BGT holders direct where additional liquidity rewards flow. By staking BGT to specific DEX pools, BGT holders decide which pools receive bonus emissions.

Step 3: Liquidity Providers Earn Boosted Yields

DEX liquidity providers (LPs) earn yields from trading fees plus the directed BGT emissions. The boosted yields incentivize liquidity provision in the pools that BGT holders prioritize.

Step 4: Validators Compete for BGT Delegations

Validators compete to attract BGT delegations by offering competitive returns, governance influence, and other benefits. The best validators attract more BGT delegations and earn more rewards.

The net effect: consensus security, liquidity provision, and governance are tightly coupled. The network's security depends on real economic activity, not just bonded stake.

The critique of PoL is that it creates complexity and reflexivity. If economic activity declines, BGT rewards decline, liquidity declines, and the cycle can compound negatively. Berachain's 2025 price action arguably demonstrated this reflexive dynamic.

The Tri-Token System

Three tokens with different functions.

BERA (Native Token)

BERA is the native gas token. All transactions on Berachain pay fees in BERA. BERA also serves as the bonded token for validators (similar to ETH for Ethereum or SOL for Solana).

Total supply: capped, with multi-year vesting schedules for team, investors, and ecosystem incentives.

Price action: BERA fell approximately 97% from its post-launch peak through mid-2026. The decline reflected several factors: aggressive token unlocks, declining DeFi activity on Berachain, and broader L1 underperformance.

BGT (Bera Governance Token)

BGT is non-transferable (cannot be sold) and earned through validator operations and other network activity. BGT holders direct liquidity rewards to specific DEX pools.

The non-transferability means BGT cannot become a speculative asset. Its value comes from the influence over liquidity allocation it provides.

Holders can burn BGT to receive BERA at a 1:1 ratio. This provides exit liquidity for BGT holders who want to monetize.

HONEY (Native Stablecoin)

HONEY is Berachain's native stablecoin, backed by a basket of assets. It serves as the main trading and liquidity asset for DeFi protocols on the network.

The success of HONEY depends on adoption by DeFi protocols and trust in its backing mechanism. Stablecoin adoption is notoriously difficult to establish.

What Went Wrong Post-Launch

Three primary factors.

Factor 1: Aggressive Token Unlocks

BERA's vesting schedule front-loaded significant unlocks in the first year. As the unlocks released to the market, sustained selling pressure overwhelmed organic buying.

Factor 2: DeFi Activity Slower Than Expected

Despite the PoL mechanism designed to incentivize liquidity, total DeFi activity on Berachain was slower to develop than the team and investors had projected. Without strong DeFi growth, the PoL flywheel could not generate the rewards needed to offset selling pressure.

Factor 3: L1 Category Headwinds

The broader L1 category faced headwinds in 2025. As Ethereum L2s captured significant scaling demand, sovereign L1s competing for similar use cases struggled. Berachain was caught in the broader category downdraft.

The combination produced sustained price decline. By mid-2026, BERA had fallen approximately 97% from peak.

The Bera Builds Businesses (BBB) Pivot

In May 2026, the Berachain Foundation announced the BBB strategic pivot. The new approach focuses on three pillars.

Pillar 1: Incubation

The Foundation incubates new applications building on Berachain. Selected projects receive funding, technical support, and ecosystem grants. The incubation focuses on applications with clear paths to generating revenue and cash flow.

Pillar 2: Acquisition

The Foundation acquires or invests in existing applications that can benefit from Berachain integration. This brings established teams and products to the ecosystem rather than relying on greenfield development.

Pillar 3: Partnership

The Foundation partners with applications that maintain their own platforms but commit to integration with Berachain. This expands the network's reach without requiring full ecosystem migration.

The BBB approach is a significant departure from typical L1 incentive programs that rely on token grants and developer subsidies. By focusing on actual cash flow and operational businesses, the pivot attempts to create durable economic activity that supports BERA's value.

The risks of the BBB pivot include execution challenges (running a venture capital operation requires different skills than running a protocol), capital allocation discipline (the Foundation must avoid funding non-viable projects), and timing (results may take 1-2 years to materialize).

How Traders Can Get Berachain Exposure

Three practical paths.

Path 1: Hold BERA on a centralized exchange. BERA trades on major CEXs including Binance, Coinbase, Bybit, KuCoin, OKX. This provides direct exposure to the broader Berachain thesis. A platform like Altrady connects to 19+ exchanges, useful for managing BERA positions across venues.

Path 2: Provide liquidity in Berachain DEXs. For sophisticated investors, providing liquidity in Berachain DEXs earns trading fees plus BGT rewards. The yields can be attractive but require active management and exposure to impermanent loss.

Path 3: Hold tokens of Berachain ecosystem projects. Various DeFi protocols, DEX tokens, and ecosystem projects on Berachain have their own tokens. Concentrated positions in specific ecosystem winners can outperform broad BERA exposure if you select well.

The Risks of Berachain Investing

Continued decline risk. Despite the 97% drawdown, further decline is possible if the BBB pivot fails to execute or if broader crypto conditions worsen. The "bottom" is not guaranteed.

Execution risk on BBB pivot. Running a venture investment strategy alongside an L1 protocol requires different organizational capabilities than the original team built. The pivot could underperform if execution falters.

Competitive pressure. Monad, other EVM-compatible L1s, and Ethereum L2s all compete for the same developer ecosystem. Berachain faces sustained competitive pressure.

Tokenomics complexity. The tri-token system is more complex than typical L1s. Complexity creates more failure modes and harder analytical work for investors.

Vesting overhang. Continued token unlocks through 2026-2027 create ongoing supply pressure that can suppress price recovery.

Community fatigue. The committed community is an asset, but sustained underperformance can erode commitment. Watching community engagement metrics is important.

How Berachain Fits Into a Crypto Portfolio

A practical framework for higher-risk allocation:

- Core large-cap holdings (BTC, ETH): 50-65% of crypto allocation

- Large alt-L1 exposure (SOL primarily): 10-20%

- Emerging high-performance L1 basket (MON, BERA, others): 5-15%. Diversify across multiple emerging L1s.

- Higher-risk speculative bucket (BERA + similar comeback stories): 2-5%. Sized for total loss tolerance.

- Cash reserves: 5-15%.

BERA specifically rarely exceeds 2-3% of total crypto portfolio for most disciplined investors due to the elevated risk profile. The position should be sized to a level where worst-case outcomes (continued decline, project failure) do not damage broader portfolio health.

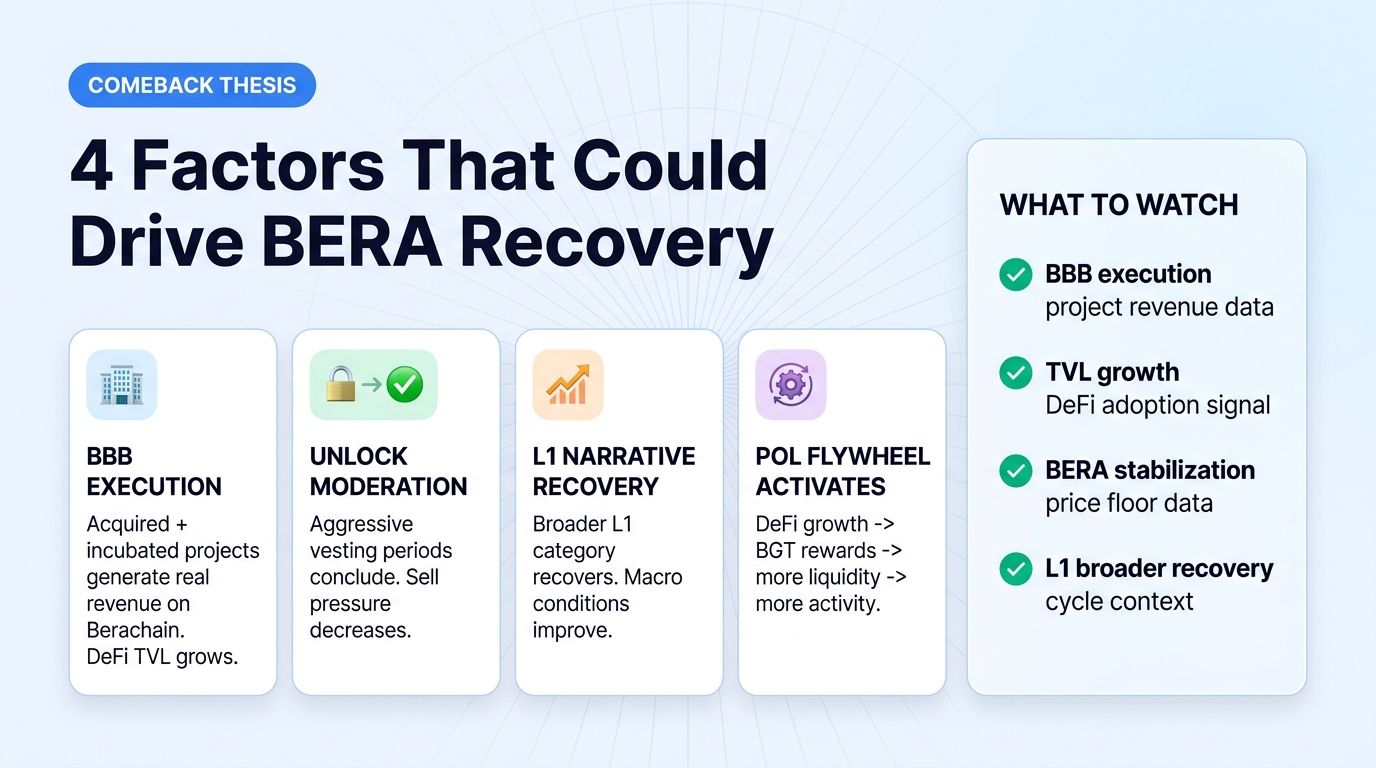

The Comeback Thesis

If the comeback thesis plays out, several factors would converge.

Factor 1: BBB execution succeeds. Acquired and incubated projects generate real revenue on Berachain. DeFi TVL grows. Network activity compounds.

Factor 2: Token unlocks moderate. As the most aggressive vesting periods conclude, selling pressure decreases. Organic buying can absorb remaining unlocks.

Factor 3: Broader L1 narrative recovers. Improving macro conditions, continued institutional adoption, and broader crypto cycles can lift the L1 category overall.

Factor 4: PoL flywheel activates. If DeFi activity grows, BGT rewards become meaningful, attracting more liquidity, which generates more activity. The flywheel that did not activate in 2025 could activate in 2026-2027.

If two or three of these factors play out, BERA can recover significantly from current levels. If none play out, the decline continues. The asymmetric upside is what makes Berachain interesting as a small-allocation comeback position.

FAQ

Should I buy BERA at current prices?

This depends on your conviction in the comeback thesis and your risk tolerance. BERA is significantly below its peak, but "down a lot" does not guarantee "up from here." If you believe in the BBB pivot and have appetite for higher-risk allocation, a small position can produce meaningful returns if the thesis plays out.

What is proof-of-liquidity in simple terms?

Proof-of-liquidity ties consensus security to real economic activity in the network's DEXs. Instead of just bonding tokens for security (proof-of-stake), validators and the broader ecosystem coordinate to provide liquidity in DEX pools. The mechanism aligns security with actual network usage.

How is Berachain different from other EVM-compatible L1s?

Berachain's main differentiation is the proof-of-liquidity consensus and tri-token system. Other EVM L1s (Monad, Avalanche, BSC, etc.) use proof-of-stake variants. The novel consensus creates different economic dynamics that may produce different outcomes over time.

Can I stake BERA?

BERA can be bonded for validator operations or delegated to validators. The exact mechanics involve the BGT system (BGT holders direct rewards). Most retail investors would delegate to a validator rather than running one directly. Yields depend on validator performance.

Can I trade BERA on Altrady?

Yes. BERA is listed on Binance, Coinbase, Bybit, KuCoin, OKX, and other major exchanges. Altrady connects to 19+ exchanges, so you can manage BERA positions alongside other crypto holdings, run automated strategies via the signal bot, grid bot, or DCA bot, and use unified portfolio tracking.

Conclusion

Berachain is one of the most interesting comeback stories in crypto in 2026. After a brutal 97% drawdown from launch peaks, the project has technical credibility, committed community, and a fresh strategic direction through the BBB pivot.

For traders, the practical takeaway is this: BERA is a higher-risk position with asymmetric payoff potential. Sized appropriately, it can produce meaningful returns if the comeback thesis plays out, while limited downside exposure if it does not.

The next 12-18 months will produce decisive information. BBB execution, BERA price stabilization, DeFi growth on Berachain, and broader L1 category performance will all matter. The comeback is not guaranteed, but the asymmetric setup makes Berachain worth attention as part of a diversified crypto portfolio.

The longer-term question is whether the proof-of-liquidity mechanism can demonstrate sustained value. The mechanism is novel and theoretically sound, but theoretical soundness does not guarantee economic success. Watching whether the PoL flywheel actually activates in 2026 will be one of the most informative data points for the entire alternative L1 thesis.