For many crypto traders, understanding tax obligations feels like navigating a minefield. Rules vary wildly between countries, deadlines shift, and the consequences of getting it wrong range from penalties to criminal prosecution. Whether you are trading spot markets, running bots, or holding long-term positions, tax compliance is not optional. It is part of the game.

Swing Traders who actively move in and out of positions across multiple exchanges face an even more complex picture. Every trade, swap, and withdrawal can potentially trigger a taxable event, and keeping track of it all manually is a serious challenge. This guide breaks down how crypto is taxed around the world in 2026, which countries offer zero or minimal crypto tax, and what practical steps you can take to stay on the right side of the law.

How Crypto Is Taxed in Most Countries

The majority of countries treat cryptocurrency as property or a financial asset rather than currency. This means that every time you sell, swap, or spend crypto at a profit, you may owe capital gains tax. The specific rates and rules depend on where you live, but the underlying principle is remarkably consistent across jurisdictions.

In practice, taxable events in crypto trading typically include selling crypto for fiat currency, exchanging one cryptocurrency for another, using crypto to pay for goods or services, and receiving crypto as income through mining, staking, or airdrops. Simply buying crypto with fiat and holding it usually does not trigger a tax obligation. The taxable moment comes when you dispose of it.

Short-Term vs. Long-Term Capital Gains

Many countries differentiate between short-term and long-term capital gains. Assets held for less than a year before selling are often taxed at a higher rate, while those held for over a year may qualify for reduced rates or even exemptions.

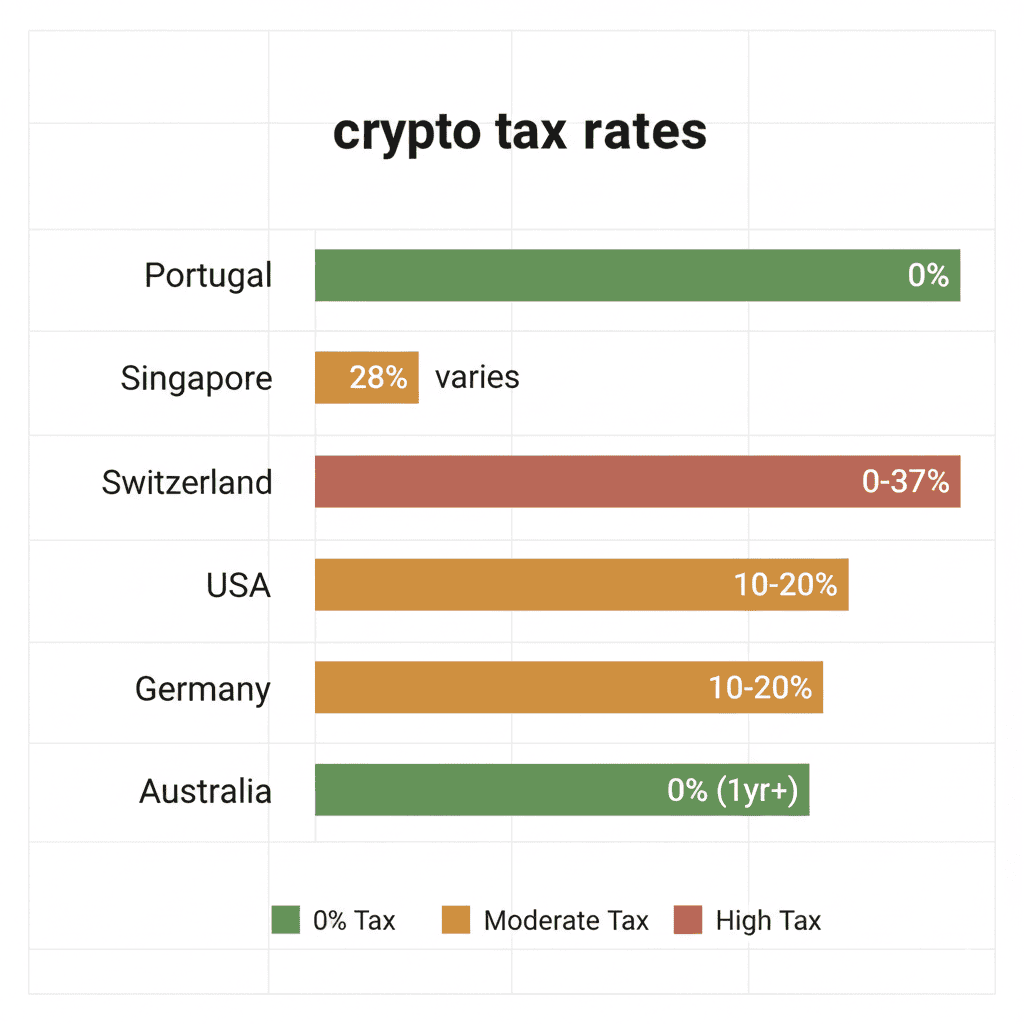

For example, in the United States, short-term crypto gains are taxed as ordinary income, which can reach up to 37% depending on your bracket. Long-term gains, on the other hand, are taxed at 0%, 15%, or 20%. Germany takes a different approach entirely. If you hold crypto for more than one year, your gains are completely tax-free regardless of the amount.

Understanding this distinction matters for active traders. Swing Traders who hold positions for days or weeks will almost always fall into the short-term category, which means higher tax rates in most jurisdictions. Planning your holding periods around tax thresholds can make a meaningful difference to your bottom line.

Countries with Zero Crypto Tax in 2026

Not every country taxes crypto gains. A growing number of jurisdictions have adopted crypto-friendly tax policies, either exempting digital assets entirely or offering extremely favorable conditions. Here are the most notable ones as of 2026.

United Arab Emirates (UAE)

The UAE remains one of the most attractive destinations for crypto traders. There is no personal income tax, no capital gains tax, and no VAT on crypto transactions. Dubai and Abu Dhabi have both established robust regulatory frameworks through their free zones, making it straightforward for traders and crypto businesses to operate legally.

The UAE's appeal goes beyond zero tax. Its strategic location, modern infrastructure, and active crypto community make it a practical choice for traders who want to relocate. However, establishing genuine residency is important. Simply setting up a shell company without physical presence may not be sufficient to claim tax benefits.

Portugal

Portugal has historically been one of Europe's most crypto-friendly nations, and while its policies have evolved, it still offers significant advantages. As of 2026, crypto held for more than 365 days is exempt from capital gains tax. Short-term gains are taxed at a flat 28% rate, which is still competitive compared to many European countries.

Portugal's Non-Habitual Resident (NHR) program, though reformed, continues to attract international traders. The country's quality of life, affordable cost of living, and growing tech scene add to its appeal beyond pure tax considerations.

Singapore

Singapore does not impose capital gains tax on individuals, which means crypto trading profits are generally tax-free for personal traders. However, if trading is your primary business activity, profits may be classified as income and taxed at the prevailing corporate or personal income tax rates.

The key distinction in Singapore is whether you are trading as an individual investor or operating as a business. Occasional traders and long-term holders benefit the most from Singapore's favorable tax treatment. The Monetary Authority of Singapore (MAS) provides clear regulatory guidance, which reduces uncertainty.

Switzerland

Switzerland takes a nuanced approach. For individual investors, crypto gains from private asset management are not subject to income tax. However, if the Swiss tax authorities classify you as a professional trader, based on factors like trading frequency, leverage use, and the proportion of your income derived from trading, your gains become taxable as income.

Several Swiss cantons, particularly Zug (known as "Crypto Valley"), offer especially favorable conditions and have built entire ecosystems around blockchain and digital assets. The country's political stability and banking infrastructure make it a strong option for serious traders.

Other Notable Jurisdictions

Several other countries deserve mention for their crypto-friendly tax policies:

- Malaysia does not tax capital gains on crypto for individual investors, though this could change as regulations evolve.

- Malta has built a comprehensive regulatory framework and offers competitive tax rates for crypto businesses, though individual taxation depends on residency status and the nature of the activity.

- El Salvador made Bitcoin legal tender and does not tax Bitcoin gains for either residents or foreigners, making it unique among sovereign nations.

- Georgia does not tax crypto gains for individuals, and its low cost of living makes it increasingly popular among digital nomads and traders.

How Crypto Tax Is Calculated

Understanding how your tax obligation is calculated is essential for accurate reporting. The core formula is straightforward, but the details matter.

Cost Basis Methods

Your tax liability depends on how you calculate your cost basis, the original value of the asset when you acquired it. The most common methods include:

- FIFO (First In, First Out): Assumes the first coins you bought are the first ones you sell. This is the default method in many jurisdictions and can result in higher taxable gains during bull markets if your earliest purchases were at the lowest prices.

- LIFO (Last In, First Out): Assumes the most recently purchased coins are sold first. This can reduce your tax liability in a rising market because your most recent (and typically highest) purchase price is used as the cost basis.

- Specific Identification: Allows you to choose exactly which coins you are selling. This gives you the most control over your tax liability but requires meticulous record-keeping.

Not all countries allow all methods. The United States, for example, permits FIFO and Specific Identification but does not officially recognize LIFO for crypto. Always verify which methods your jurisdiction accepts before filing.

DeFi, Staking, and Airdrops

Decentralized finance activities introduce additional tax complexity. Staking rewards are generally treated as income at their fair market value when received. Liquidity pool earnings, yield farming rewards, and governance token distributions may also be taxable as income.

Airdrops present a particularly tricky situation. In some jurisdictions, the mere receipt of an airdrop triggers an income tax event, even if you did not request it. In others, the tax obligation only arises when you sell or swap the airdropped tokens. Keeping records of the fair market value at the time of receipt is critical in either case.

For Swing Traders using DeFi protocols alongside centralized exchanges, tracking becomes exponentially more difficult. Every interaction with a smart contract, including swaps, deposits, withdrawals, and claims, can potentially be a taxable event that needs documentation.

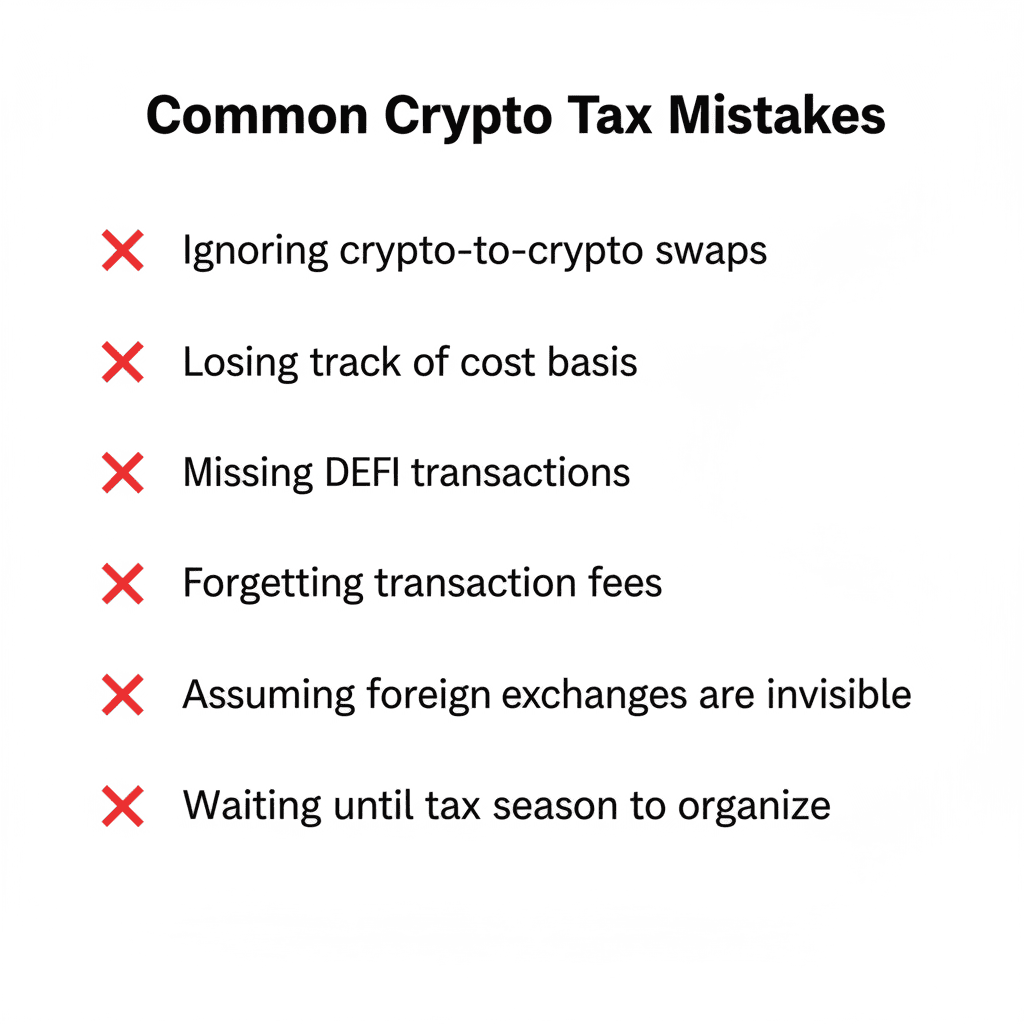

Common Mistakes Crypto Traders Make with Taxes

Even experienced traders make costly tax errors. Here are the most frequent ones to avoid.

Ignoring crypto-to-crypto swaps. Many traders assume that only cashing out to fiat triggers a tax event. In most jurisdictions, swapping BTC for ETH or any other crypto pair is a taxable disposal. Every trade counts.

Failing to track cost basis across exchanges. When you move crypto between exchanges or wallets, the cost basis travels with it. If you lose track of your original purchase price, you may end up overpaying taxes or, worse, underreporting gains.

Missing DeFi transactions. On-chain activities like swaps on decentralized exchanges, claiming staking rewards, or providing liquidity are often taxable but easy to overlook if you are only tracking centralized exchange activity.

Not accounting for transaction fees. Gas fees and trading fees can generally be added to your cost basis or deducted from your proceeds, reducing your taxable gain. Failing to include them means you are likely paying more tax than necessary.

Assuming foreign exchanges are invisible. Tax authorities in major jurisdictions have data-sharing agreements and increasingly use blockchain analytics. Trading on a non-reporting exchange does not make your gains invisible to the tax authorities.

Procrastinating on record-keeping. Trying to reconstruct a full year of trading activity at tax time is a nightmare. The best approach is to track every transaction in real time or use automated tools that pull data from your exchanges and wallets continuously.

Practical Steps to Stay Compliant

Tax compliance does not have to be overwhelming if you approach it systematically. Here are actionable steps every crypto trader should follow.

Keep Detailed Records from Day One

Record every transaction: date, amount, price at the time, fees paid, and the purpose of the transaction. Whether you use a spreadsheet, a dedicated crypto tax tool, or your exchange's built-in export feature, consistency is what matters most. The longer you wait to start tracking, the harder it becomes to reconstruct your history.

Use Crypto Tax Software

Tools like Koinly, CoinTracker, and TokenTax can connect to your exchanges and wallets, automatically categorize transactions, and generate tax reports for your jurisdiction. They handle the complex calculations: cost basis, gains and losses, income from staking, so you do not have to do it manually.

Most crypto tax tools support direct integration with popular exchanges. If you trade on multiple platforms, look for software that can aggregate all your activity into a single, unified report.

Understand Your Local Rules

Tax regulations change frequently, especially in the crypto space. What was true last year may not apply this year. Make it a habit to review your country's latest guidance at least once per tax season. If your situation is complex, for example if you trade across multiple jurisdictions, use DeFi protocols heavily, or have significant unrealized gains, consulting a tax professional who specializes in crypto is a worthwhile investment.

Harvest Your Losses

Tax-loss harvesting is the practice of selling losing positions to offset gains elsewhere in your portfolio. Many jurisdictions allow you to deduct crypto losses against crypto gains, and some even let you carry forward unused losses to future tax years. This is a legitimate and widely used strategy to reduce your tax bill.

Be aware of wash sale rules, though. Some countries prohibit you from claiming a loss if you repurchase the same asset within a short window (typically 30 days). While not all jurisdictions apply wash sale rules to crypto yet, this is an evolving area of regulation.

Separate Trading and Personal Wallets

Keeping your trading activity in dedicated wallets and exchange accounts, separate from personal holdings, makes record-keeping significantly easier. It also simplifies audits if your tax authority ever requests documentation.

Crypto Tax Checklist for 2026

- Have you recorded every trade, swap, and transfer for the tax year?

- Have you included income from staking, airdrops, and mining?

- Have you calculated cost basis using a method accepted in your jurisdiction?

- Have you accounted for transaction fees and gas costs?

- Have you identified any losses eligible for tax-loss harvesting?

- Have you checked whether your jurisdiction requires reporting foreign exchange accounts?

- Have you verified the current tax rates and thresholds for your country?

FAQ

Do I need to pay tax on crypto I have not sold?

In most countries, simply holding cryptocurrency does not trigger a tax obligation. Taxes typically apply only when you dispose of the asset by selling, swapping, spending, or gifting it. However, there are exceptions. Some jurisdictions may tax unrealized gains under specific wealth tax rules, and receiving crypto as income (from mining, staking, or employment) is generally taxable at the time of receipt regardless of whether you sell it. The safest approach is to check your local tax authority's guidance on what constitutes a taxable event.

Can I move to a tax-free country to avoid crypto taxes?

Relocating to a country with zero crypto tax is legal, but it requires genuine residency. Simply setting up a mailing address or bank account in a crypto-friendly country while continuing to live elsewhere will not satisfy most tax authorities. You typically need to establish real physical presence, sever tax residency ties with your previous country, and comply with your former country's exit tax rules if applicable. It is a legitimate strategy, but one that requires careful planning and usually professional advice.

How do tax authorities track crypto transactions?

Tax authorities have become increasingly sophisticated in tracking crypto activity. Major exchanges in regulated countries are required to report user transaction data to tax authorities under frameworks like the OECD's Crypto-Asset Reporting Framework (CARF). Blockchain analytics firms like Chainalysis and Elliptic work directly with government agencies to trace on-chain transactions. Additionally, many countries participate in international data-sharing agreements. Assuming your crypto activity is invisible because you use decentralized exchanges or non-KYC platforms is risky. The technology for tracking continues to advance rapidly.

Trading is risky. Losses can happen quickly in volatile markets, and tax optimization is not a guarantee of profit. Swing Traders, use proper position sizing, predefined stops, and responsible tax planning before allocating meaningful capital. Start a free trial on Altrady to manage your trades across multiple exchanges from a single dashboard, with built-in tracking tools that make portfolio management and record-keeping simpler.