What Is the Kelly Criterion?

In the world of trading and probability theory, few mathematical frameworks have stood the test of time like the Kelly Criterion. Developed in 1956 by John L. Kelly Jr., a researcher at Bell Labs, this formula was originally designed to solve a problem in information theory: how much signal to send over a noisy telephone line. Kelly recognized that the same math could be applied to any scenario where someone repeatedly allocates capital to uncertain outcomes with known probabilities.

The concept quickly caught the attention of traders and investors alike. In the decades that followed, legendary figures such as Edward Thorp, the mathematician who cracked blackjack and wrote "Beat the Dealer," applied Kelly's formula to card counting and later to financial markets. Warren Buffett and Charlie Munger have also referenced Kelly-style thinking in their capital allocation decisions, though they typically apply it qualitatively rather than as a strict formula.

For crypto traders, the Kelly Criterion offers something genuinely valuable: a mathematically grounded answer to the question "how much of my account should I risk on this trade?" In a market notorious for volatility, overleveraging, and emotional decision-making, having a principled framework for position sizing can be the difference between long-term profitability and blowing up an account.

The Kelly Formula Explained

The Kelly Criterion is expressed as a deceptively simple formula:

f\* = (bp - q) / b

Breaking down each component:

- f\* is the fraction of your capital to allocate to the trade

- b is the odds received on the trade, meaning the ratio of potential profit to potential loss (also called the reward-to-risk ratio)

- p is the probability of winning (your win rate as a decimal)

- q is the probability of losing, which equals 1 - p

So if a trade has a 55% win rate and a 1.5:1 reward-to-risk ratio, the calculation looks like this:

f\ = (1.5 x 0.55 - 0.45) / 1.5 f\ = (0.825 - 0.45) / 1.5 f\ = 0.375 / 1.5 f\ = 0.25, or 25% of capital

This result tells you that, given those exact inputs, the mathematically optimal position size is 25% of your available capital. Anything less leaves potential growth on the table. Anything more increases the risk of ruin beyond what the math supports.

The formula is grounded in expected logarithmic utility, meaning it maximizes the geometric growth rate of your capital over many repeated trades. It does not maximize the arithmetic average return, which is what most traders intuitively think about. This distinction matters enormously in practice.

Applying Kelly to Crypto Trading

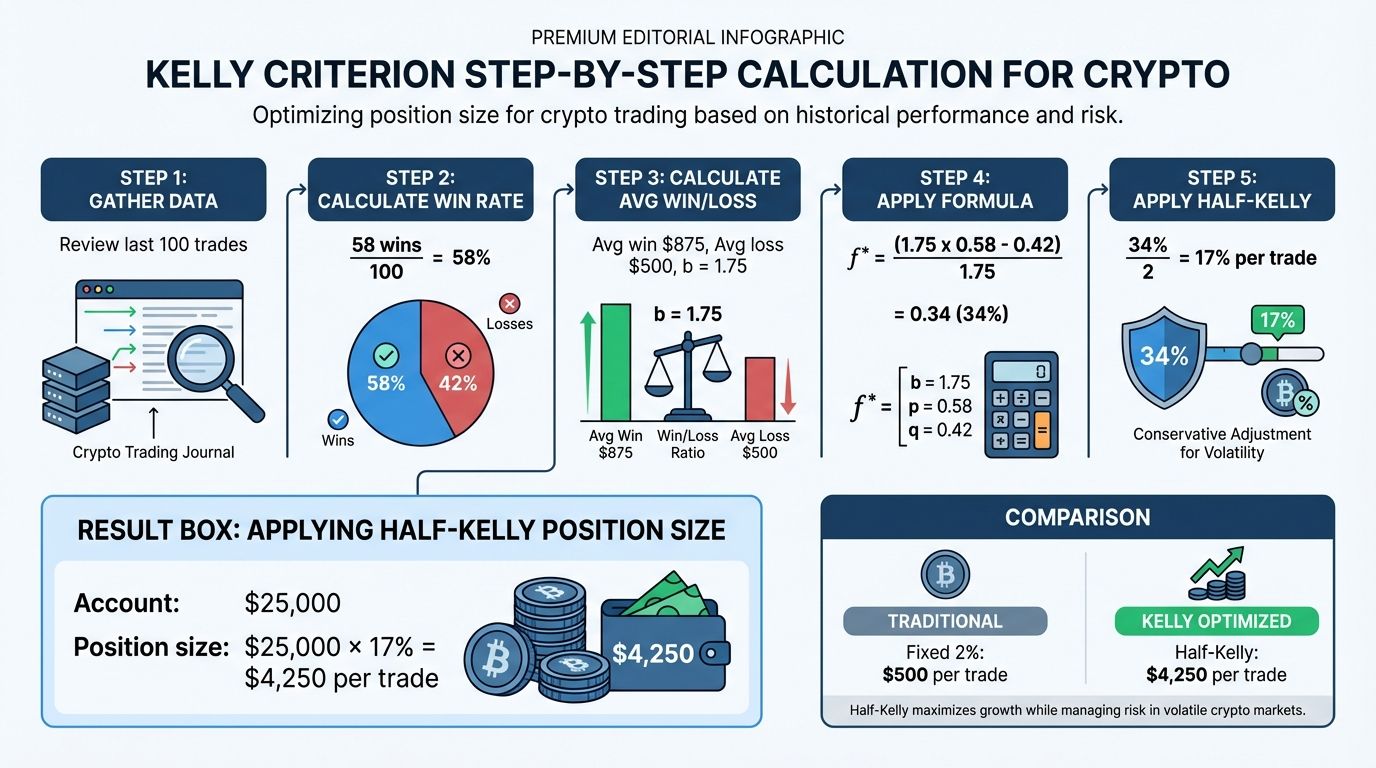

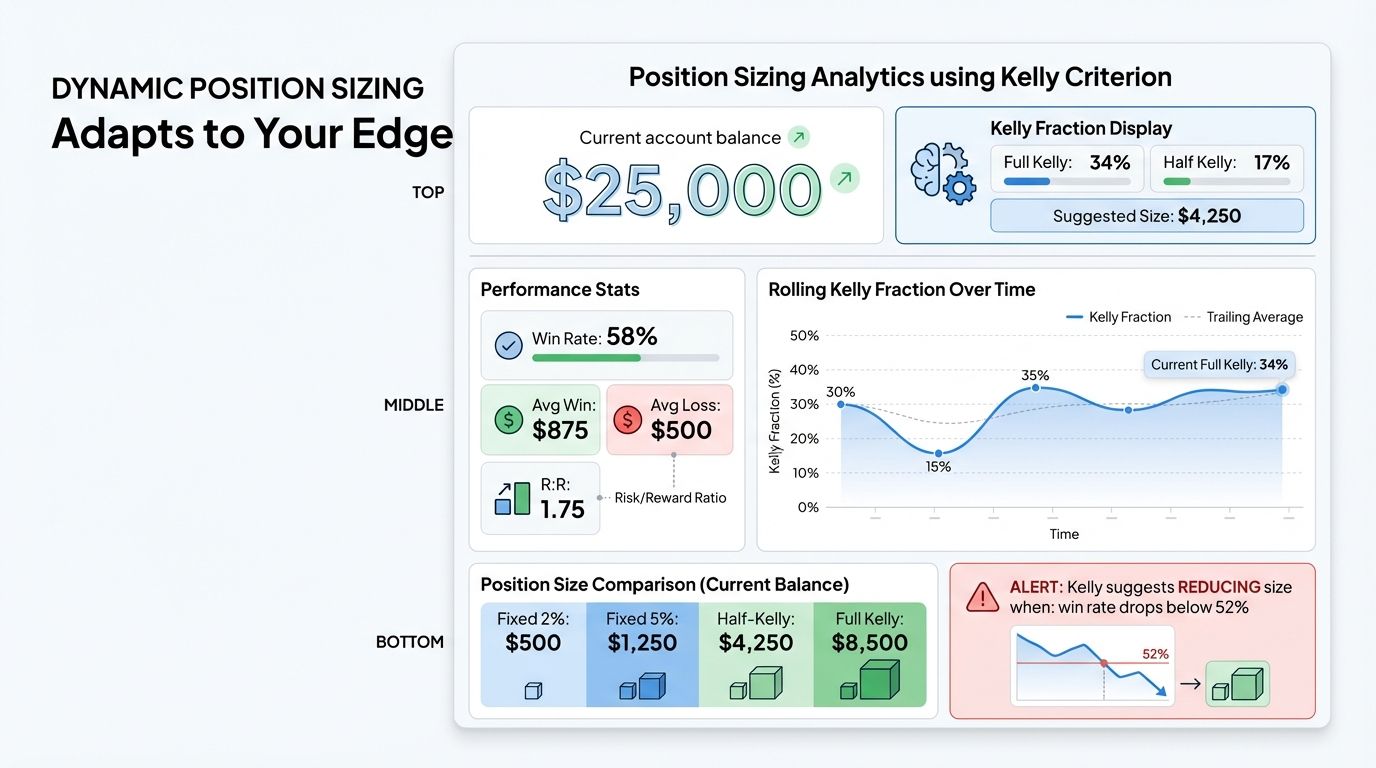

Applying the Kelly Criterion to crypto trading requires you to have a reliable estimate of two inputs: your historical win rate and your average reward-to-risk ratio. Both figures should come from a sufficiently large sample of real trades, typically at least 50 to 100 closed positions.

Here is a concrete example. Suppose you have been trading Bitcoin breakouts for six months and your trading journal shows the following:

- Win rate: 55% (55 winning trades out of 100)

- Average winning trade: +$150 per $100 risked, so a 1.5:1 reward-to-risk ratio

- Average losing trade: $100 loss per trade

Plugging these numbers into the Kelly formula:

f\* = (1.5 x 0.55 - 0.45) / 1.5 = 0.25

The Kelly Criterion says to risk 25% of your account on each trade. For most crypto traders, this figure will feel alarming, and for good reason. It assumes your inputs are perfectly accurate, that each trade is statistically independent, and that you can handle the emotional and practical reality of occasionally losing 25% of your account on a single position. In practice, most professionals use a scaled-down version of this number.

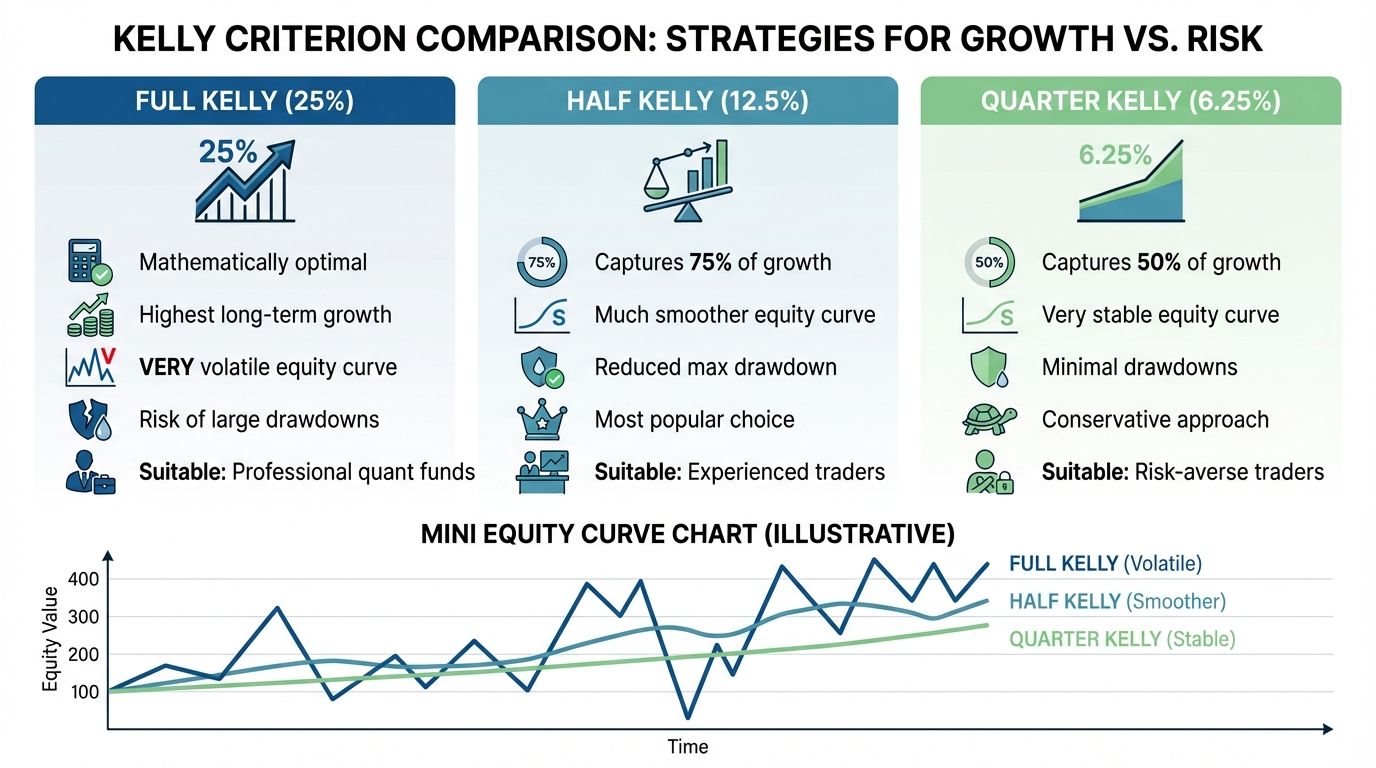

Full Kelly vs Fractional Kelly

The output of the Kelly formula is often called the Full Kelly. While it is mathematically optimal under ideal conditions, it comes with serious practical drawbacks for active traders.

Full Kelly produces the maximum long-term geometric growth but also generates the maximum drawdowns along the way. A sequence of losing trades can wipe out a substantial portion of your account even when you are trading with a genuine edge. For crypto, where market regimes can shift rapidly and historical statistics can become temporarily unreliable, Full Kelly is considered dangerously aggressive by most professional traders.

Half-Kelly is simply half the Full Kelly output. If Full Kelly says 25%, you trade 12.5%. Research and practical experience consistently show that Half-Kelly captures roughly 75% of the optimal growth rate while dramatically reducing drawdowns and variance. For most traders, this is the preferred approach.

Quarter-Kelly is 25% of the Full Kelly output. At 6.25% for the example above, this feels much more conservative but remains mathematically justified as a way to account for estimation error in your win rate and reward-to-risk inputs.

The core insight is this: the Kelly formula assumes your probability estimates are precise. In reality, they are not. Fractional Kelly is a practical way to build in a margin of safety for estimation error.

Step-by-Step Kelly Calculation for Crypto

Let's walk through a complete example using a $25,000 trading account.

Step 1: Gather your trading statistics

Pull at least the last 100 trades from your journal or trading platform. Calculate:

- Total winning trades: 58 out of 100

- Win rate (p): 0.58

- Loss rate (q): 0.42

- Average profit per winning trade: $375

- Average loss per losing trade: $250

- Reward-to-risk ratio (b): 375 / 250 = 1.5

Step 2: Apply the Kelly formula

f\ = (1.5 x 0.58 - 0.42) / 1.5 f\ = (0.87 - 0.42) / 1.5 f\ = 0.45 / 1.5 f\ = 0.30 (Full Kelly = 30%)

Step 3: Choose your Kelly fraction

- Full Kelly: 30% = $7,500 per trade

- Half-Kelly: 15% = $3,750 per trade

- Quarter-Kelly: 7.5% = $1,875 per trade

Step 4: Set your stop loss and calculate position size

If you use Half-Kelly and plan to risk $3,750 on a BTC trade with a stop loss set 2% below entry, your position size is:

Position size = Risk amount / Stop loss percentage Position size = $3,750 / 0.02 = $187,500 worth of BTC

This is the notional value of the position, not the amount of capital used. On a leveraged exchange, this determines your leverage ratio. On a spot account, this tells you how many dollars worth of BTC to purchase.

Step 5: Reassess periodically

Recalculate your Kelly fraction after every 50 trades or whenever your strategy undergoes a significant change. Win rates and reward-to-risk ratios drift over time as market conditions evolve.

Comparison: Fixed 2% vs Half-Kelly vs Full Kelly

The table below illustrates how three different position sizing approaches might perform across 100 trades using the statistics from the example above (58% win rate, 1.5:1 reward-to-risk, starting with $25,000).

| Metric | Fixed 2% | Half-Kelly (15%) | Full Kelly (30%) |

|---|---|---|---|

| Risk per trade | $500 | $3,750 | $7,500 |

| Total gain after 100 trades | ~$12,180 | ~$89,400 | ~$142,000 |

| Worst simulated drawdown | ~12% | ~38% | ~61% |

| Account value at end | ~$37,180 | ~$114,400 | ~$167,000 |

| Probability of ruin (50% loss) | Near 0% | ~4% | ~18% |

The numbers illustrate the trade-off clearly. Fixed 2% is safe but leaves a massive amount of growth unrealized. Full Kelly maximizes returns but exposes the account to gut-wrenching drawdowns and a real chance of catastrophic loss. Half-Kelly sits in the middle, capturing most of the upside at a fraction of the psychological and financial cost.

Note: The figures above are illustrative approximations based on Monte Carlo-style reasoning. Actual results will vary depending on the sequence of wins and losses.

Advantages of Kelly Criterion Over Fixed Percentage

The standard approach most new traders learn is fixed fractional sizing: risk 1% or 2% of your account on every trade regardless of the setup's quality. While simple and consistent, this method ignores the actual statistical properties of your trading strategy.

Mathematical optimality. The Kelly Criterion maximizes the long-term geometric growth rate of your capital. No other sizing strategy has been proven to grow capital faster over a large number of independent trials with known probabilities. Fixed percentages, by contrast, are arbitrary and make no use of your edge size.

Scales with edge. When your win rate and reward-to-risk ratio improve, Kelly automatically recommends a larger position. When your statistics deteriorate, it recommends a smaller one. This creates a natural feedback loop that aligns position size with demonstrated performance.

Adapts to opportunity quality. If you trade multiple strategies with different statistical profiles, Kelly allows you to size each strategy proportionally to its edge. A high-win-rate scalping strategy would receive a different Kelly fraction than a lower-win-rate trend-following system, reflecting their true differences in edge size.

Prevents oversizing. Perhaps counterintuitively, Kelly also puts an upper limit on position size. If your edge is small, the formula prescribes a small position. Traders who blow accounts typically overbet, often because they have no systematic framework for sizing. Kelly prevents this by grounding every decision in data.

Risks and Limitations

The Kelly Criterion is a powerful tool, but it comes with important caveats that every crypto trader should understand before applying it.

Garbage in, garbage out. The formula is only as accurate as the inputs. If your sample size is small (fewer than 50 trades), your win rate and reward-to-risk estimates will have high variance. A win rate estimated from 20 trades could easily be off by 10 percentage points in either direction, which would produce a Kelly fraction that is wildly incorrect.

Assumes independent trades. The mathematical foundation of Kelly assumes that each trade is statistically independent from the previous one. In practice, trades are not always independent. A volatile market event can produce multiple consecutive losses across different positions simultaneously. Correlation between trades means Full Kelly is even riskier than the formula suggests.

Assumes accurate probability estimates. In probability scenarios with fixed rules, probabilities are known precisely. In trading, they are estimated from historical data and assumed to remain stable going forward. Crypto markets are prone to regime changes, where the statistical properties of price action shift suddenly and dramatically. A strategy with a 58% win rate in a trending market may perform very differently in a choppy, low-volatility environment.

Psychological challenges. Even Half-Kelly can produce drawdowns that are emotionally difficult to endure. A 38% drawdown on a $25,000 account means watching your portfolio fall to $15,500. Most traders will abandon a strategy long before it recovers, locking in losses and destroying the very statistical edge Kelly was designed to exploit.

Oversizing risk. Because Kelly grows positions as the account grows, a streak of bad luck early in a trading period can shrink the account enough that subsequent Kelly-sized positions, though smaller in absolute terms, concentrate risk at a vulnerable time. Some traders address this by using a fixed dollar amount rather than a percentage during drawdowns.

The solution to most of these limitations is the same: use fractional Kelly, maintain a large and well-documented trade journal, and reassess your statistics regularly.

Size Your Positions Smarter with Altrady

Understanding the Kelly Criterion is one thing. Implementing it consistently across every trade you take is another. Altrady's position sizing tools, portfolio analytics, and trade tracking features give you the data infrastructure you need to calculate and apply Kelly-based sizing in real time.

With Altrady, you can track your win rate and average reward-to-risk ratio across all your trades, across all the exchanges you use, from a single dashboard. The platform's built-in performance metrics make it straightforward to gather the statistical inputs the Kelly formula requires, so your position sizing decisions are always grounded in your actual trading history rather than guesswork.

Whether you are trading Bitcoin on Binance, altcoins on Kraken, or perpetuals on Bybit, Altrady connects your accounts and consolidates your performance data so you always know exactly what your edge looks like. Start a free trial today and see how smarter position sizing translates into more disciplined, more profitable trading.

Frequently Asked Questions

What is the Kelly Criterion in simple terms?

The Kelly Criterion is a mathematical formula that tells you what percentage of your capital to risk on a trade based on your historical win rate and the average size of your wins relative to your losses. Its goal is to maximize the long-term growth rate of your account without exposing you to an unnecessary risk of ruin.

Is Full Kelly too aggressive for crypto trading?

For most retail crypto traders, yes. Full Kelly maximizes long-term returns under ideal mathematical conditions, but it produces large drawdowns that are difficult to endure psychologically and can be catastrophic if your statistical inputs are slightly off. Most professionals use Half-Kelly or Quarter-Kelly as a safer approach that still captures the core benefit of the formula.

How many trades do I need before I can use Kelly sizing?

A minimum of 50 closed trades is generally considered necessary to get a statistically meaningful estimate of your win rate and average reward-to-risk ratio. A sample of 100 or more trades is preferable. Using Kelly with fewer than 50 data points is risky because your estimates will have too much variance to be reliable.

Does the Kelly Criterion work for all types of crypto strategies?

The formula applies to any strategy where you can estimate a win rate and a reward-to-risk ratio from historical data. This includes trend following, breakout trading, mean reversion, and even certain algorithmic strategies. However, it works best when trades are reasonably independent and market conditions are relatively stable. Strategies that cluster trades in highly correlated assets or during the same market events may not meet the independence assumption cleanly.

What happens if the Kelly formula gives a negative number?

A negative Kelly fraction means the formula has detected that your strategy has a negative expected value, meaning you are more likely to lose money over time than to make it. A negative result is a clear signal that you should not be trading this strategy at all until you improve your win rate, your reward-to-risk ratio, or both. It is one of the most useful outputs the formula can produce because it prevents you from allocating capital to a losing system.