Crypto arbitrage is the practice of profiting from price differences for the same asset across different markets, trading pairs, or venues. Because crypto markets are fragmented across dozens of exchanges that each run their own order books, the same asset can trade at slightly different prices in different places at the same moment. Arbitrage captures that gap.

The appeal is straightforward: arbitrage is one of the few crypto strategies that does not depend on predicting direction. You are not anticipating whether Bitcoin goes up or down. You are exploiting a structural inefficiency that exists right now. The challenge is that these inefficiencies are small, short-lived, and competitive, which means execution speed, low fees, and multi-exchange access determine whether arbitrage is actually profitable after costs.

This guide explains the three core arbitrage methods in depth (triangular, statistical, and cross-exchange), the mechanics and worked logic behind each, the costs and risks that erode arbitrage profit, and how to execute these strategies practically using a multi-exchange setup like Altrady, which connects to 19+ exchanges from a single interface.

What Is Crypto Arbitrage?

Arbitrage exploits the fact that an asset's price is not perfectly synchronized everywhere. In an idealized efficient market, the same asset would have one price everywhere at once. Real crypto markets are not efficient in this way. Liquidity is fragmented, order books are independent, and price discovery happens at different speeds on different venues.

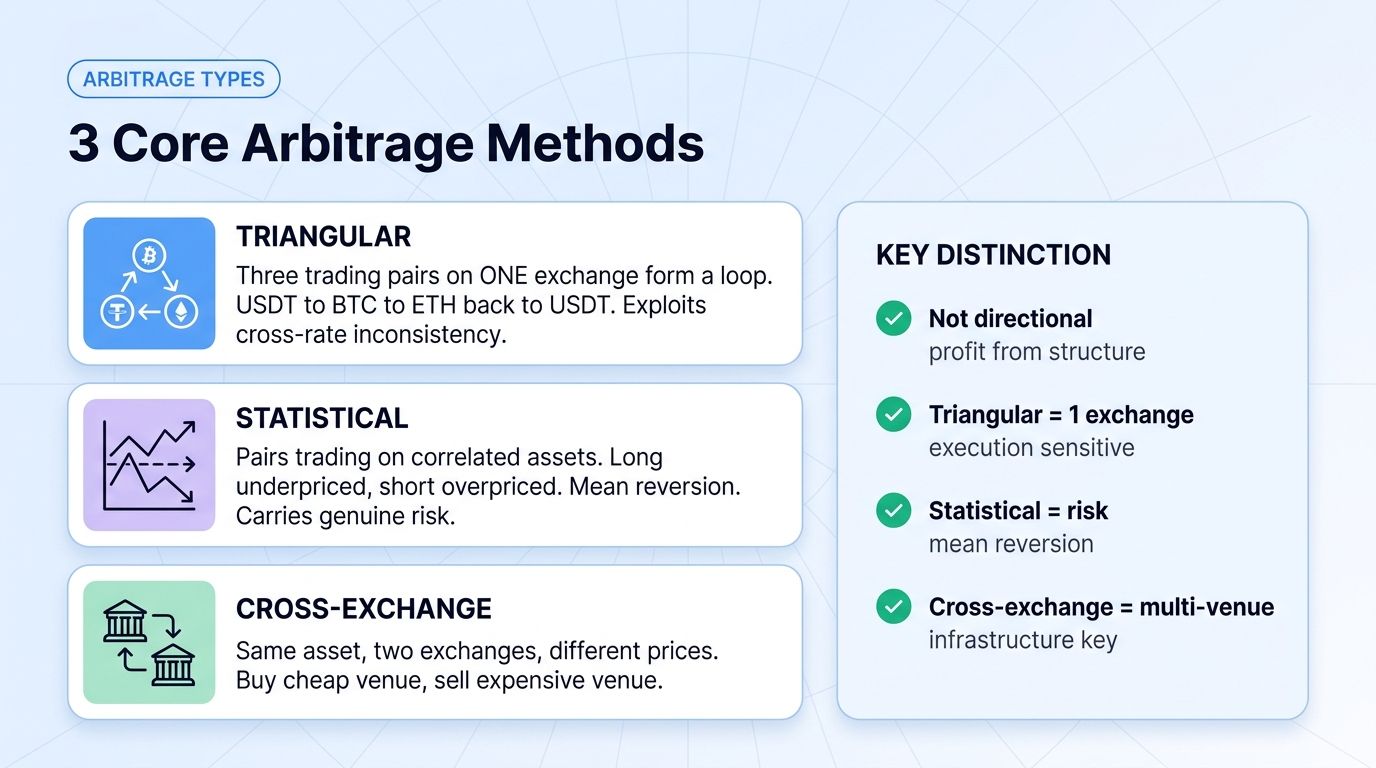

This fragmentation creates three distinct categories of price discrepancy that traders can exploit.

First, discrepancies between trading pairs on a single exchange (the basis for triangular arbitrage).

Second, statistical mispricings between historically correlated assets (the basis for statistical arbitrage).

Third, price differences for the same asset between two different exchanges (the basis for cross-exchange arbitrage).

Each method has a different risk profile, capital requirement, and execution challenge. Understanding all three lets a trader choose the approach that matches their infrastructure and risk tolerance.

Triangular Arbitrage

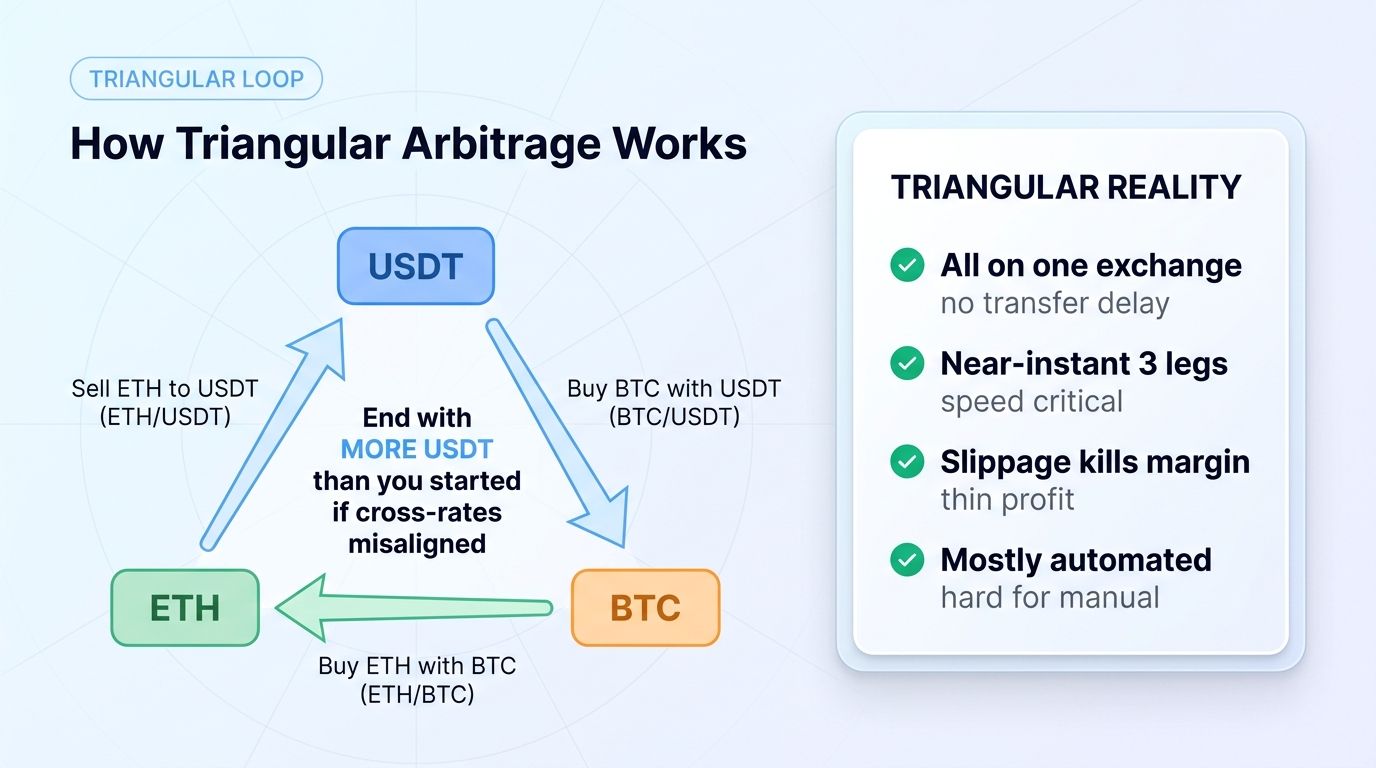

Triangular arbitrage exploits price inconsistencies between three trading pairs on the same exchange. Because it happens entirely within one venue, it avoids the transfer delays and withdrawal risks of moving assets between exchanges.

How Triangular Arbitrage Works

The strategy involves three currencies and three trades that form a loop, starting and ending with the same asset. If the cross-rates between the three pairs are temporarily inconsistent, completing the loop returns more of the starting asset than you began with.

Consider a loop using USDT, BTC, and ETH on a single exchange:

- Start with USDT. Buy BTC with USDT (using the BTC/USDT pair).

- Buy ETH with that BTC (using the ETH/BTC pair).

- Sell that ETH back to USDT (using the ETH/USDT pair).

If the implied cross-rate between the three pairs is misaligned, you end the loop with more USDT than you started with. The profit comes from the inconsistency between the direct ETH/USDT price and the synthetic ETH price implied by routing through BTC.

Why Triangular Opportunities Appear and Disappear

These inconsistencies appear when one of the three pairs updates its price slightly before the others, creating a momentary gap. They disappear quickly because they exist entirely within one exchange's order books, where automated systems constantly scan for and close them.

The practical implications are significant. Triangular arbitrage requires fast detection and near-instant execution of all three legs. Because all three trades happen on the same exchange, there are no withdrawal delays, but slippage on any of the three legs can erase the thin profit margin. This is generally the most execution-sensitive of the three arbitrage types.

Statistical Arbitrage

Statistical arbitrage (often called stat arb) is a quantitative approach that exploits temporary mispricings between assets that have a historical statistical relationship. Unlike triangular and cross-exchange arbitrage, which target near-risk-free price gaps, statistical arbitrage accepts a degree of risk in exchange for opportunities that are more frequent and larger.

How Statistical Arbitrage Works

The classic form is pairs trading. A trader identifies two assets that have historically moved together (for example, two Layer 1 tokens that tend to be correlated). When the price relationship between them diverges beyond its normal range, the trader takes opposing positions: long the relatively underpriced asset and short the relatively overpriced one. The position profits if the relationship reverts to its historical norm.

The key concept is mean reversion. Statistical arbitrage assumes that temporary divergences from a historical relationship tend to correct over time. The trader is not taking a view on market direction; they are anticipating that the spread between two correlated assets returns to its average.

Why Statistical Arbitrage Is Different

Statistical arbitrage carries genuine risk that triangular and cross-exchange arbitrage do not. The historical relationship can break down permanently. Two assets that were correlated for months can decouple due to a fundamental change in one of them. This means statistical arbitrage requires careful position sizing, stop-loss discipline, and ongoing monitoring of whether the statistical relationship still holds.

The advantage is that statistical mispricings are more frequent and can be larger than the tiny gaps targeted by pure arbitrage. The strategy is more like a systematic, market-neutral trading approach than a risk-free profit capture. It rewards quantitative analysis, backtesting, and disciplined risk management.

Cross-Exchange Arbitrage

Cross-exchange arbitrage exploits price differences for the same asset between two different exchanges. If Bitcoin trades slightly cheaper on one exchange than another at the same moment, a trader can buy on the cheaper venue and sell on the more expensive one.

How Cross-Exchange Arbitrage Works

The basic mechanic is simple. Suppose BTC trades at one price on Exchange A and a slightly higher price on Exchange B. The trader buys BTC on Exchange A and sells BTC on Exchange B, capturing the difference.

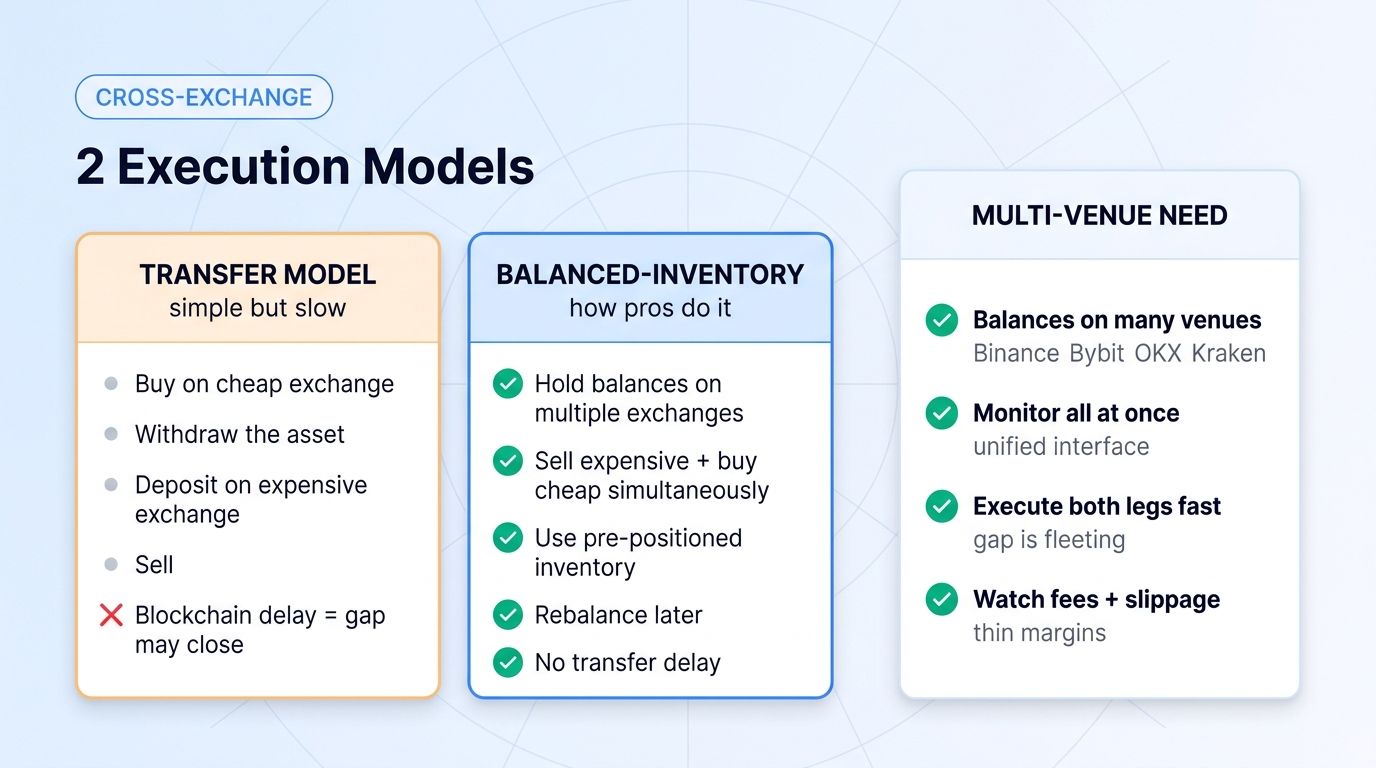

There are two main execution models.

The first is the transfer model. Buy on the cheaper exchange, withdraw the asset, deposit it on the more expensive exchange, and sell. This is conceptually simple but slow, because blockchain withdrawal and deposit times introduce delay during which the price gap can close or reverse.

The second is the balanced-inventory model. Maintain balances of both the asset and a quote currency (like USDT) on multiple exchanges simultaneously. When a gap appears, sell on the expensive exchange and buy on the cheap exchange at the same time, using your pre-positioned balances. Later, rebalance inventory as needed. This avoids the transfer delay entirely and is how most serious cross-exchange arbitrage is executed.

The Realities of Cross-Exchange Arbitrage

Cross-exchange arbitrage requires accounts and balances on multiple exchanges. A trader running this strategy might hold inventory across exchanges like Binance, Bybit, OKX, Kraken, and others to capture gaps wherever they appear. The more venues you can monitor and execute on simultaneously, the more opportunities you can capture.

The main constraints are withdrawal fees and times (for the transfer model), exchange trading fees on both legs, the capital required to maintain balances across multiple venues, and the risk that a gap closes before both legs complete. Price differences between major exchanges are usually small and fleeting, so execution efficiency is decisive.

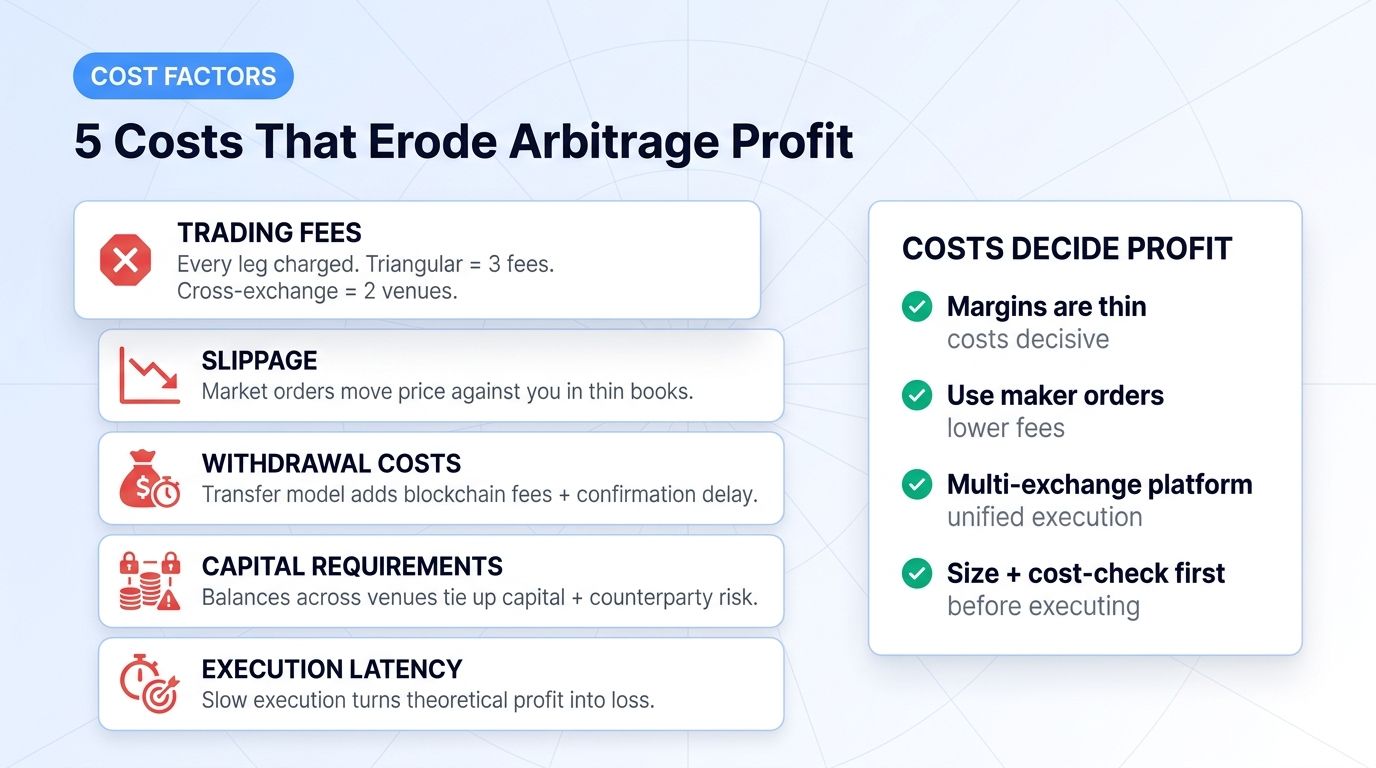

The Costs That Erode Arbitrage Profit

Arbitrage profits are thin, which makes costs the deciding factor between profit and loss. Several costs must be accounted for.

Trading fees. Every arbitrage involves multiple trades, each charged a fee. Triangular arbitrage has three legs, each with a fee. Cross-exchange has two legs on two venues. Fees can easily exceed the price gap if not carefully managed. Using maker orders where possible and fee discounts can be the difference between profit and loss.

Slippage. Arbitrage profit assumes you execute at the prices you see. In practice, executing a market order moves the price against you, especially in thin order books. Slippage on any leg can erase the margin.

Withdrawal and transfer costs. For transfer-model cross-exchange arbitrage, blockchain withdrawal fees and confirmation times add cost and risk.

Capital requirements. Maintaining balances across multiple exchanges ties up capital and introduces exchange counterparty risk (the risk that an exchange freezes withdrawals or fails).

Execution latency. The time between detecting an opportunity and completing all legs determines whether the gap is still there when you execute. Slow execution turns theoretical profit into realized loss.

How to Execute Arbitrage With Altrady's Multi-Exchange Setup

Cross-exchange arbitrage in particular depends on managing positions across many venues simultaneously, which is exactly the problem a multi-exchange platform solves. Altrady connects to 19+ exchanges from a single interface, which provides several practical advantages for arbitrage traders.

Unified multi-exchange access. Altrady connects to 19+ exchanges including Binance, Bybit, OKX, Kraken, KuCoin, Coinbase, and others. Rather than logging into each exchange separately, a trader monitors and trades across all connected venues from one terminal. This is foundational for cross-exchange arbitrage, where you need to see prices and execute on multiple venues at once.

Unified portfolio tracking. Maintaining inventory across multiple exchanges for the balanced-inventory model requires knowing your balances everywhere at a glance. Altrady aggregates holdings across all connected exchanges into a single portfolio view, so you always know how much of each asset and quote currency you have on each venue.

Fast order execution with Smart Trading. Arbitrage is execution-sensitive. Altrady's Smart Trading features let you place and manage orders quickly with predefined parameters, which matters when capturing fleeting price gaps.

Risk management tools. For statistical arbitrage, which carries genuine risk, the Risk Reward Calculator helps size positions appropriately and define exit levels before entering. Disciplined risk management is what separates sustainable statistical arbitrage from gradual capital erosion.

Automated strategies. While Altrady offers a signal bot, grid bot, and DCA bot for systematic trading, traders interested in automated arbitrage execution often combine multi-exchange monitoring with dedicated arbitrage bots. For a deeper look at automated approaches, see resources on arbitrage bots and how they operate across exchanges like Bybit and others.

The practical workflow for cross-exchange arbitrage with a multi-exchange setup is: maintain quote-currency and asset balances on several connected exchanges, monitor for price gaps across venues from the unified interface, execute both legs simultaneously when a gap exceeds your cost threshold, and periodically rebalance inventory across exchanges.

The Risks of Arbitrage Trading

Execution risk. The gap can close before you complete all legs, leaving you with an unhedged position or a loss.

Fee and slippage risk. Costs can exceed the price gap, turning a theoretical profit into a realized loss.

Counterparty risk. Holding balances across multiple exchanges exposes you to the risk of an exchange freezing withdrawals or failing. Diversifying across reputable exchanges and not over-concentrating funds on any single venue mitigates this.

Statistical breakdown risk (for stat arb). Historical relationships can break down permanently, turning a mean-reversion trade into a sustained loss.

Capital efficiency risk. Capital tied up across multiple exchanges to enable arbitrage is capital not deployed elsewhere. The opportunity cost matters.

Competition risk. Arbitrage is competitive. Professional firms and bots scan for the same opportunities with faster infrastructure. Retail arbitrage is most viable in less-monitored pairs and venues, and in statistical approaches where speed is less decisive than analysis.

How Arbitrage Fits Into a Trading Approach

Arbitrage is best understood as one tool among several rather than a complete strategy. For most traders, the practical framing is:

- Cross-exchange arbitrage: Viable for traders with multi-exchange infrastructure and the capital to maintain balances across venues. Most efficient with a unified multi-exchange platform.

- Triangular arbitrage: Highly execution-sensitive and typically dominated by fast automated systems. Difficult for manual retail traders but useful to understand.

- Statistical arbitrage: The most accessible to analytically inclined retail traders, since it rewards research and discipline over raw speed. Carries genuine risk and requires proper position sizing.

Arbitrage works best as a complement to other strategies rather than a sole approach, particularly given the capital requirements and the competitive, costs-sensitive nature of the opportunities.

UK angle: crypto arbitrage checks before you start

For UK-based traders, crypto arbitrage starts with the same core question as anywhere else: can the price gap survive fees, transfer time, execution delay, and slippage? The local angle is mostly operational. Check which exchanges are available to you, which account funding routes you actually use, and how quickly you can move or rebalance capital between venues.

Cross-exchange arbitrage can look simple on a screen but become much harder once withdrawal limits, network fees, settlement delays, and liquidity depth are included. UK traders should calculate the full round trip cost before treating any spread as actionable.

Triangular arbitrage is usually even more execution-sensitive because all legs happen inside one exchange. A manual trader is often too slow for the cleanest gaps, which is why dashboards, alerts, and automation matter. Even then, the setup should be tested with small size first.

Altrady can help UK traders monitor multiple supported exchanges, compare execution conditions, and manage orders from a single workspace. It does not remove exchange fees or market risk, so the edge still has to come from disciplined calculation, position sizing, and fast risk control.

FAQ

What is the easiest type of crypto arbitrage for beginners?

Statistical arbitrage (pairs trading) is often the most accessible for analytically inclined beginners because it rewards research and discipline rather than raw execution speed. However, it carries genuine risk since historical relationships can break down. Cross-exchange arbitrage is conceptually simple but requires accounts and balances on multiple exchanges. Triangular arbitrage is the hardest for manual traders because it is extremely execution-sensitive and dominated by automated systems.

Is crypto arbitrage risk-free?

No. While triangular and cross-exchange arbitrage target structural price gaps that are lower-risk than directional trading, they are not risk-free. Execution risk, fees, slippage, withdrawal delays, and counterparty risk can all turn a theoretical profit into a loss. Statistical arbitrage carries even more risk because historical relationships can break down permanently. No form of arbitrage is genuinely risk-free in practice.

How much capital do I need for crypto arbitrage?

It depends on the method. Cross-exchange arbitrage typically requires meaningful capital because you maintain balances across multiple exchanges to capture gaps without transfer delays. Triangular arbitrage requires capital on a single exchange. Statistical arbitrage capital requirements scale with position size. Because arbitrage profits are percentage-thin, larger capital is generally needed to produce meaningful absolute returns after costs.

Why do crypto arbitrage opportunities exist?

Crypto markets are fragmented across dozens of independent exchanges, each with its own order book and liquidity. Prices are not perfectly synchronized everywhere, and price discovery happens at different speeds on different venues. These structural inefficiencies create temporary price gaps that arbitrage captures. The gaps are small and short-lived because automated systems constantly work to close them.

How does Altrady help with crypto arbitrage?

Altrady connects to 19+ exchanges (including Binance, Bybit, OKX, Kraken, and others) from a single interface, which is foundational for cross-exchange arbitrage. It provides unified portfolio tracking across all connected exchanges, fast order execution through Smart Trading, and risk management tools like the Risk Reward Calculator for sizing statistical arbitrage positions. Managing multiple exchanges from one terminal removes the friction of logging into each venue separately.

Conclusion

Crypto arbitrage offers something rare in trading: a way to profit from market structure rather than market direction. The three core methods (triangular, statistical, and cross-exchange) each exploit a different kind of inefficiency in fragmented crypto markets.

For traders, the practical takeaways are these. Triangular arbitrage is execution-sensitive and largely automated. Statistical arbitrage is the most accessible to analytically inclined traders but carries genuine mean-reversion risk that demands disciplined position sizing. Cross-exchange arbitrage is the classic multi-venue play, and its viability depends heavily on having efficient multi-exchange infrastructure to monitor and execute across venues simultaneously.

In every case, costs are decisive. Trading fees, slippage, withdrawal delays, and capital requirements all erode the thin margins that arbitrage targets. Success depends on minimizing these costs and executing efficiently.

A multi-exchange platform like Altrady, connecting to 19+ exchanges with unified portfolio tracking and fast execution, addresses the core infrastructure challenge of cross-exchange arbitrage. For traders serious about arbitrage, the combination of broad exchange access, unified monitoring, and disciplined risk management is what turns theoretical price gaps into realized, after-cost profit. Sizing positions appropriately and accounting for all costs before executing remains the standard discipline for any arbitrage approach.

What should UK traders check before attempting crypto arbitrage?

UK traders should check exchange availability, funding costs, withdrawal limits, network fees, liquidity depth, tax record needs, and whether the price gap remains after the full round trip cost. Altrady can help monitor multiple supported exchanges, but the trader still needs to control execution risk and position size.