What Are Options Greeks?

If you have spent any time trading crypto options, you have probably heard traders throw around terms like "delta neutral" or "high vega play." These are references to the Options Greeks, a set of mathematical measures that describe how an option's price responds to changes in market conditions.

Greeks are not just abstract math. They are your real-time dashboard for understanding risk. When you buy a Bitcoin call option, you are not simply taking a directional position. You are taking on exposure to time, volatility, interest rates, and the speed at which all of these factors change. Each Greek quantifies one slice of that exposure.

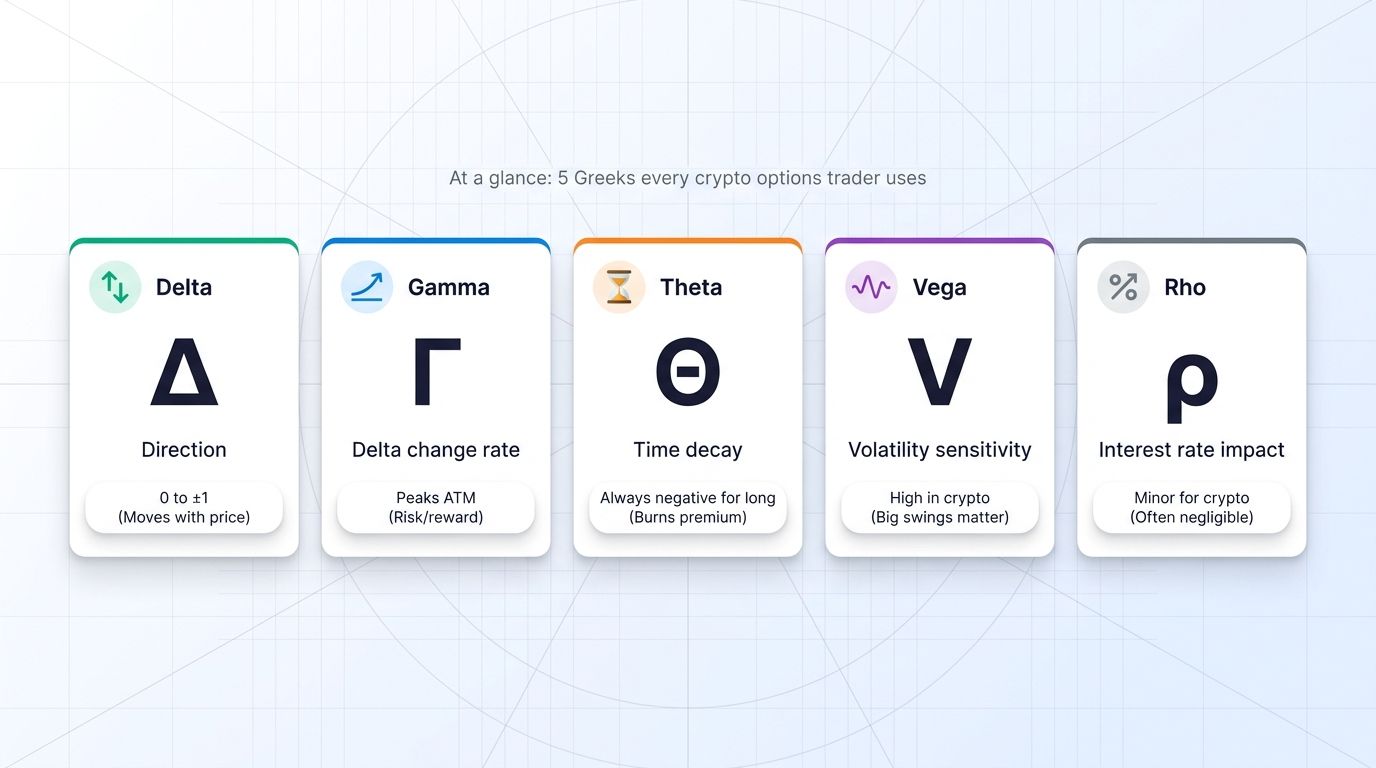

There are five primary Greeks that every serious crypto options trader should understand: Delta, Gamma, Theta, Vega, and Rho. Together they tell you how your position behaves under different scenarios, from a sudden 10% BTC pump to a quiet weekend where implied volatility collapses.

Understanding these metrics becomes especially important in crypto because the asset class is structurally different from equities. Bitcoin and Ethereum regularly see annualized implied volatility of 60 to 100 percent or higher. That compares to 15 to 20 percent for most stock indices. In an environment this volatile, ignoring Greeks is how traders get blindsided.

Delta: Directional Exposure

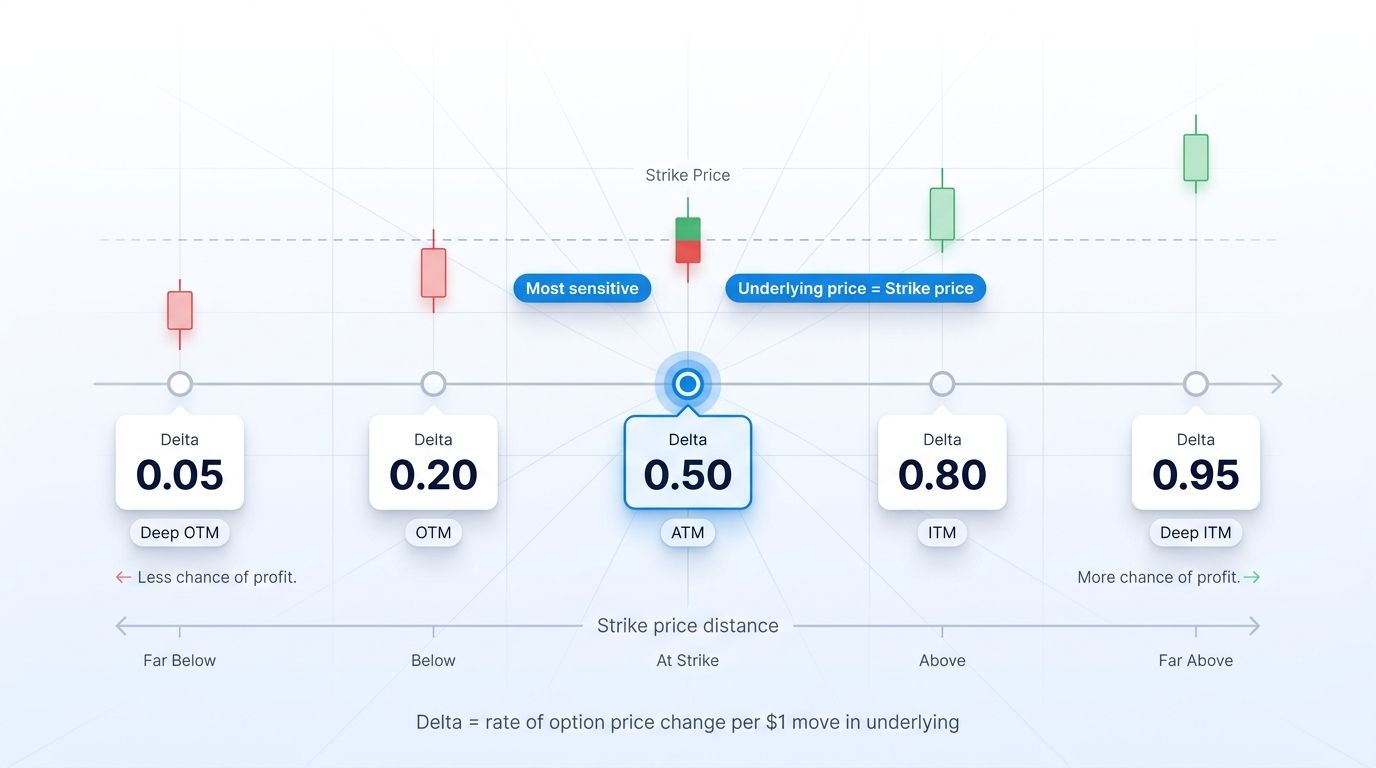

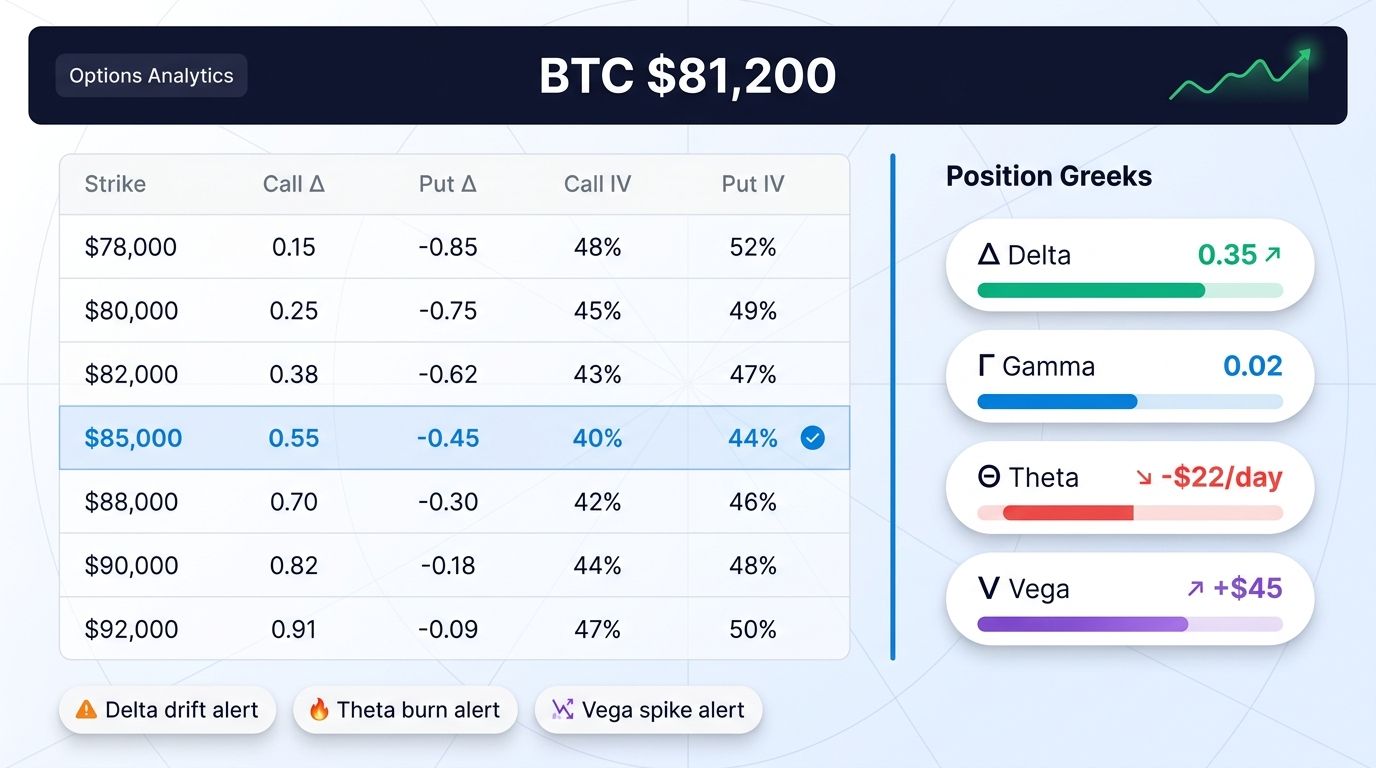

Delta is the most fundamental Greek. It measures how much an option's price changes for every $1 move in the underlying asset.

For call options, Delta ranges from 0 to 1. If a BTC call option has a Delta of 0.60, a $1 rise in BTC causes the option to gain approximately $0.60 in value. For put options, Delta ranges from -1 to 0. A BTC put with a Delta of -0.40 gains $0.40 in value for every $1 BTC falls.

Delta by moneyness:

- Deep in-the-money (ITM) calls: Delta approaches 1.0. These behave almost like holding spot BTC.

- At-the-money (ATM) calls: Delta is approximately 0.50.

- Deep out-of-the-money (OTM) calls: Delta approaches 0. The option is mostly premium with low directional sensitivity.

Practical example: Suppose BTC is trading at $85,000 and you buy a call option with a strike of $87,000 expiring in two weeks. This option is out of the money. It might have a Delta of 0.30. If BTC rises $2,000 to $87,000, your option gains approximately $600 in value per BTC contract. If BTC falls $2,000 to $83,000, the option loses roughly $600.

Delta is also widely used as a rough probability estimate. A 0.30 Delta call is roughly a 30% chance of expiring in the money according to the model. Traders use this when screening strikes for covered calls or spreads.

Delta hedging is the practice of offsetting your option's directional exposure by taking a position in the underlying. A delta-neutral book has a combined Delta near zero, meaning short-term price moves in either direction do not dramatically affect your portfolio value.

Gamma: Rate of Delta Change

If Delta tells you how fast your option moves with price, Gamma tells you how fast Delta itself changes. Gamma is the acceleration of your directional exposure.

Gamma is always positive for long options (both calls and puts) and negative for short options. It peaks for at-the-money options and drops off sharply for deep ITM or deep OTM contracts.

Why Gamma matters in crypto:

Because BTC and ETH can move 5 to 15 percent in a single day, Gamma risk is not theoretical. If you are short an ATM option and the market makes a big move, Delta shifts rapidly and your short position can incur losses faster than you can re-hedge.

Example: You sell an ATM BTC call when BTC is at $85,000. The option has Delta 0.50 and Gamma 0.0003. BTC jumps to $88,000, a $3,000 move. Delta has now shifted upward by roughly 0.0003 x 3,000 = 0.90. Your short call has gone from 0.50 Delta to effectively near 1.0, meaning it now moves almost dollar-for-dollar with BTC. Your losses accelerate sharply.

Long Gamma vs. Short Gamma:

- Long Gamma (bought options): You benefit from big moves. Time works against you, but large price swings generate profits.

- Short Gamma (sold options): You collect premium and profit from quiet markets. Large moves hurt you.

The tension between Gamma and Theta (see below) is at the core of most options strategies.

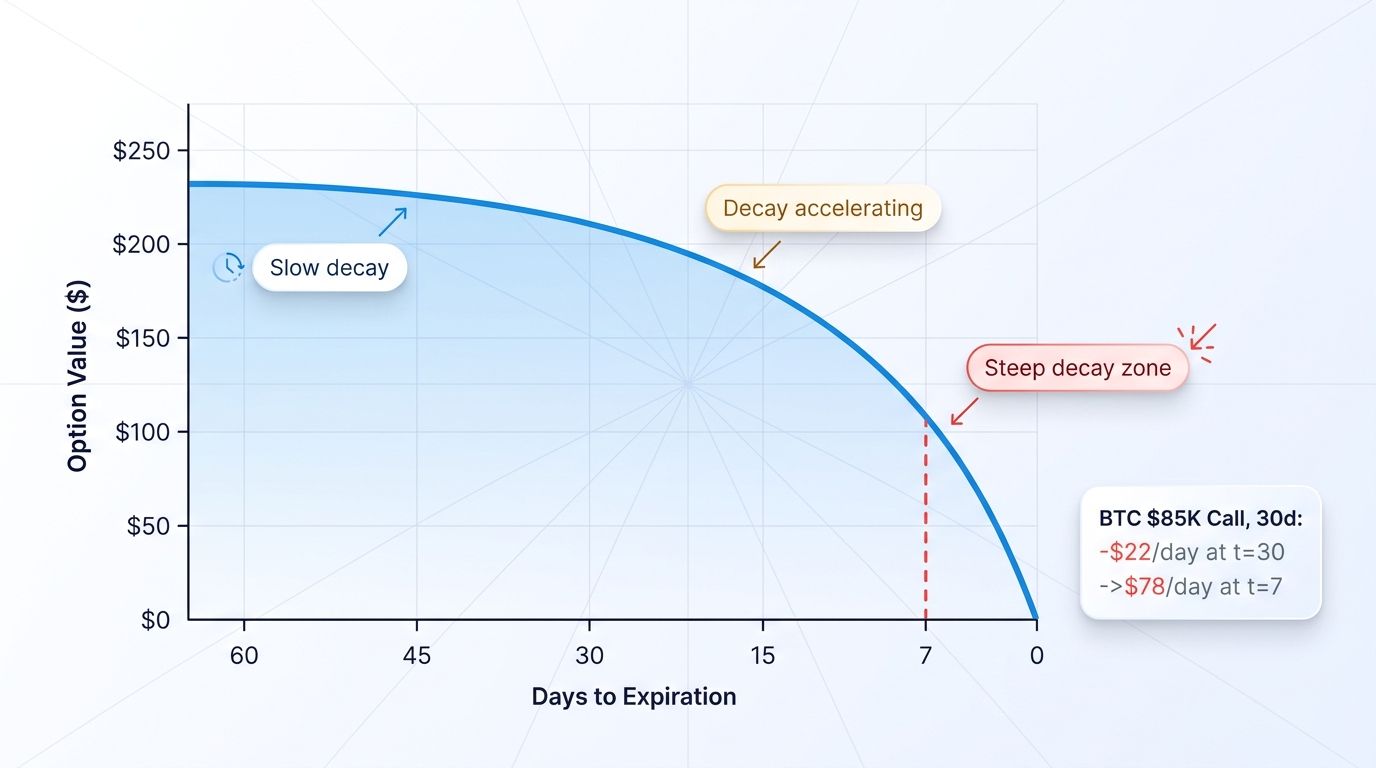

Theta: Time Decay

Theta measures how much value an option loses each day as it approaches expiration, all else being equal. It is expressed as a negative number for long positions because time decay erodes the option's premium.

Options are wasting assets. The "extrinsic value" (or time value) built into the premium bleeds out with each passing day. This bleed accelerates as expiration approaches, following a non-linear curve. An option loses value faster in its final week than in its first week.

BTC Theta example:

Suppose you buy a BTC call option with a $90,000 strike, 14 days to expiry, and BTC trading at $85,000. The option is priced at $1,200. It might carry a Theta of -$90 per day. After one week of flat price action, the option has lost roughly $630 in time value and is now worth approximately $570, even if BTC has not moved.

Theta is most aggressive for ATM options near expiration. Deep ITM and deep OTM options have lower Theta because they carry less extrinsic value.

Seller's advantage: Option sellers (writers) benefit from positive Theta. Each day that passes with no adverse move, the seller pockets a portion of the premium. This is why selling covered calls on BTC or ETH is popular during sideways or mildly bullish markets. The seller earns time decay while holding the underlying.

Buyer's burden: If you buy options, time is working against you from the moment you enter. To profit, the underlying must move enough, fast enough, to offset the daily Theta bleed.

Vega: Volatility Sensitivity

Vega measures how much an option's price changes for every 1 percentage point change in implied volatility (IV). A Vega of $50 means the option gains or loses $50 for each 1% move in implied volatility.

Vega is arguably the most critical Greek for crypto options traders because of how extreme IV can get in this market.

Implied volatility vs. historical volatility:

Historical volatility (HV) measures how much the asset has actually moved over a past period. Implied volatility (IV) is forward-looking, extracted from current option prices. It reflects the market's expectation of future volatility.

In equity markets, index IV typically sits between 15 and 25 percent annually. In crypto, BTC IV regularly runs 60 to 90 percent. During major events such as protocol upgrades, regulatory announcements, or macro shocks, IV can spike well above 100 percent. ETH IV has similar characteristics and can be even more volatile around network events.

Vega in practice:

You buy a 30-day ETH call when IV is at 75%. The option costs $400 and has a Vega of $15. If IV rises to 85% (a 10-point increase), your option gains $150 in value just from the IV expansion, independent of any ETH price move. Conversely, if IV collapses to 60% after the anticipated event passes, you lose $225 in value even if ETH is flat.

This is called "IV crush" and it is one of the most common ways crypto options traders lose money. Buying options ahead of a major catalyst (like a Bitcoin ETF decision or ETH upgrade) often means paying elevated IV. Once the event passes, IV reverts and the option loses value rapidly.

Long Vega vs. Short Vega:

- Long options (calls or puts): Long Vega. You benefit when IV rises.

- Short options: Short Vega. You benefit when IV falls or stays flat.

Traders who anticipate a volatility expansion (but are unsure of direction) use long straddles or strangles, which are long both a call and a put. These positions profit from IV increases or large price moves.

Rho: Interest Rate Sensitivity

Rho measures how much an option's price changes for a 1 percentage point change in the risk-free interest rate. For call options, Rho is positive (higher rates increase call value slightly). For puts, Rho is negative.

In traditional finance, Rho matters most for long-dated equity options during periods of active central bank policy. In crypto, Rho is the least important Greek for several reasons. Crypto options are typically short-dated, expiring within days to weeks. The risk-free rate has a small effect on short-term extrinsic value. Additionally, crypto lending rates are volatile and not directly tied to central bank policy in the same way.

That said, Rho is not entirely irrelevant. During periods of rising interest rates, longer-dated BTC LEAPS (options with months or years to expiry) can see measurable Rho effects. As the crypto derivatives market matures and longer-duration instruments become more common, Rho will grow in importance.

For most active crypto options traders focusing on weekly or monthly expirations, Rho is background noise compared to Delta, Gamma, Theta, and Vega.

Greeks at a Glance: Summary Table

| Greek | Measures | Typical Range | Crypto Relevance |

|---|---|---|---|

| Delta | Price sensitivity per $1 underlying move | -1 to 1 | High, core to hedging |

| Gamma | Rate of Delta change | 0 to infinity | Very high, crypto's big moves amplify Gamma risk |

| Theta | Daily time value decay | Negative (buyers), Positive (sellers) | High, especially near expiry |

| Vega | Sensitivity to 1% IV change | Positive (buyers), Negative (sellers) | Very high, crypto IV is extreme |

| Rho | Sensitivity to 1% interest rate change | Small positive/negative | Low for short-dated, moderate for LEAPS |

How Greeks Work Together in Practice

Greeks do not operate in isolation. Understanding how they interact is what separates novice options traders from professionals.

Example 1: Selling a covered call on BTC

You hold 1 BTC at $85,000 and sell a 30-day call with a $90,000 strike. The call has:

- Delta: 0.30 (short, so -0.30 for your position)

- Theta: +$60/day (you collect this as the seller)

- Vega: -$40 per 1% IV (you lose if IV rises)

- Gamma: -0.0002 (short Gamma means big moves hurt you)

In a sideways market, you collect $60 per day in Theta. BTC stays flat for two weeks and you pocket $840 in time decay. But if BTC surges to $93,000, your short call goes deep ITM, Gamma accelerates your losses, and you are capped at $90,000 on your BTC position. The trade-off is explicit: Theta income in exchange for limited upside and short Gamma risk.

Example 2: Delta hedging a long options portfolio

You buy an ETH call spread going into a major network event, expecting volatility to spike. Your position is long 5 ETH calls with a combined Delta of +2.5. To neutralize short-term direction risk (you want Vega, not Delta), you short 2.5 ETH in the spot or perpetual market. Your net Delta is now near zero. You profit if IV rises regardless of price direction, but lose Theta daily while waiting.

Gamma scalping is an advanced extension of this: as price moves, Delta shifts, and you re-hedge the Delta by trading spot. In a volatile market, this dynamic re-hedging can generate profit from the price swings themselves, funded by your short-Gamma position in premium.

Using Greeks for Crypto Options Strategies

Different strategies have different Greek profiles. Knowing what you own helps you manage positions under changing conditions.

Strategies and their Greek signatures:

- Long call/put (directional position): Positive Delta (call) or negative Delta (put), positive Gamma, negative Theta, positive Vega. Best when you expect a big move and rising IV.

- Covered call: Reduced positive Delta, positive Theta, negative Vega. Best in sideways to mildly bullish markets.

- Long straddle (ATM call + put): Near-zero Delta, positive Gamma, negative Theta, positive Vega. Best when you expect a large move but are unsure of direction, and IV is currently low.

- Iron condor (short OTM call spread + short OTM put spread): Near-zero Delta, negative Gamma, positive Theta, negative Vega. Best in low-volatility, range-bound markets.

- Calendar spread (short near-term, long far-term ATM): Near-zero Delta, positive Vega, positive Theta (net). Best when IV is low and you expect it to rise.

In crypto, the most popular retail strategies tend to be long calls (directional speculation), covered calls (yield generation on BTC or ETH holdings), and long straddles ahead of high-impact events. Each of these has a distinct Greek profile that dictates when and why it performs.

Monitoring Greeks in real time:

As market conditions change, your Greeks change. A position that starts Delta-neutral can become significantly directional after a 5% BTC move. Active traders review their portfolio Greeks at least daily and re-hedge when thresholds are breached. Platforms that display aggregate Greeks across a multi-exchange portfolio make this significantly easier.

Trade Options Smarter with Altrady

Managing a crypto options portfolio across multiple exchanges is complex. Prices move fast, Greeks shift constantly, and missing a re-hedge window can turn a well-planned position into a significant loss.

Altrady is a professional crypto trading platform built for traders who take risk management seriously. With multi-exchange connectivity, you can view and manage BTC, ETH, and altcoin options positions across all your accounts in one dashboard, without jumping between tabs and spreadsheets.

Key features relevant to options traders:

- Portfolio tracking across exchanges: Consolidate all your open positions, including options and spot holdings, into a single view so you always know your total exposure.

- Risk management tools: Set alerts and stop conditions to protect your positions when the market moves against you. In a high-Gamma environment, speed matters.

- Real-time market data: Accurate, low-latency price feeds are essential when you are delta-hedging or monitoring Theta decay on short-dated positions.

- Customizable alerts: Get notified when BTC or ETH moves past a threshold that triggers a re-hedge, or when IV crosses a level that affects your Vega exposure.

Whether you are selling covered calls on your BTC stack, running a long straddle into a protocol event, or managing a complex multi-leg spread, having all the data in one place reduces errors and improves execution.

Start a free trial with Altrady today and see how a purpose-built trading platform changes the way you manage crypto options risk.

Frequently Asked Questions

What is the most important Greek for crypto options traders?

For most traders, Vega is the most critical Greek to understand in crypto. Because Bitcoin and Ethereum implied volatility is structurally much higher than in equity markets (60 to 100 percent versus 15 to 20 percent for stock indices), volatility swings can dramatically affect an option's value even when price barely moves. IV crush after a major event is one of the most common reasons options buyers lose money in crypto. Delta is equally important for directional traders, but Vega tends to catch newcomers off guard.

What does Delta neutral mean and why would a trader want it?

A Delta-neutral position has a combined Delta near zero, meaning short-term price moves in the underlying do not significantly affect your profit or loss. Traders set up Delta-neutral positions when they want to isolate a different Greek, typically Vega or Theta. For example, if you expect volatility to rise ahead of a Bitcoin halving but are unsure of price direction, you might buy an ATM straddle and hedge the small residual Delta. You profit from IV expansion without being exposed to whether BTC goes up or down.

How does Theta decay accelerate near expiry?

Theta decay is non-linear. An option does not lose the same dollar amount every day. In the early weeks of an option's life, time decay is relatively slow. As expiration approaches, the rate of decay accelerates sharply. This is because extrinsic value (the portion of premium beyond intrinsic value) diminishes rapidly in the final days. A BTC option with 30 days to expiry might lose $80 per day in Theta, while the same option with 5 days to expiry might lose $300 per day. This is why option sellers often prefer to write contracts with 2 to 6 weeks until expiry, capturing the steepest part of the decay curve.

Can I use Greeks to manage risk on a covered call position?

Yes, Greeks are ideal for covered call management. When you sell a call against your BTC holdings, you take on short Delta (partially offsetting your spot long), short Gamma (big BTC moves hurt you), positive Theta (you earn daily decay), and short Vega (you lose if IV spikes). Monitoring Delta tells you how much of your BTC upside is capped at the current strike. Watching Theta shows you how much premium you are earning per day. If IV rises significantly (say from 70% to 90%), the short Vega exposure means your short call has become more expensive to close. Greeks help you decide whether to roll the position, take profits early, or hold to expiry.

How is Gamma risk different in crypto compared to traditional markets?

In equity markets, large single-day moves of 5 to 10 percent are rare outside of individual stock events. In crypto, BTC and ETH regularly see moves of this magnitude within a single trading session. This amplifies Gamma risk significantly. When you are short Gamma (which happens any time you sell options), a large adverse move causes Delta to shift rapidly against you, accelerating your losses. Crypto traders need to size their short-Gamma exposure more conservatively than equity traders, and they need faster re-hedging capabilities. The combination of high IV and high realized volatility makes Gamma one of the most dangerous Greeks to ignore in crypto options trading.