ETH stakers face a recurring question. The base staking yield sits around 3-4% APY. EigenLayer and the liquid restaking protocols built on top offer 8-15% APY by stacking additional rewards from services that pay for shared security. The math looks obvious. The risk picture is not.

In April 2026, Kelp DAO, one of the largest liquid restaking protocols, suffered a $280-293 million exploit when an attacker drained rsETH via a LayerZero cross-chain bridge vulnerability. It was the largest single DeFi exploit of 2026 to that point. Anyone who had not understood the layered risks of restaking learned them in 24 hours.

This guide explains the difference between staking, restaking, and liquid restaking, walks through the major protocols, and covers what you actually accept in exchange for the higher yield. By the end, you should be able to decide whether the extra return justifies the extra risk for your portfolio.

Staking, Restaking, and Liquid Restaking

The three terms describe a chain of decisions, each one layering on top of the previous.

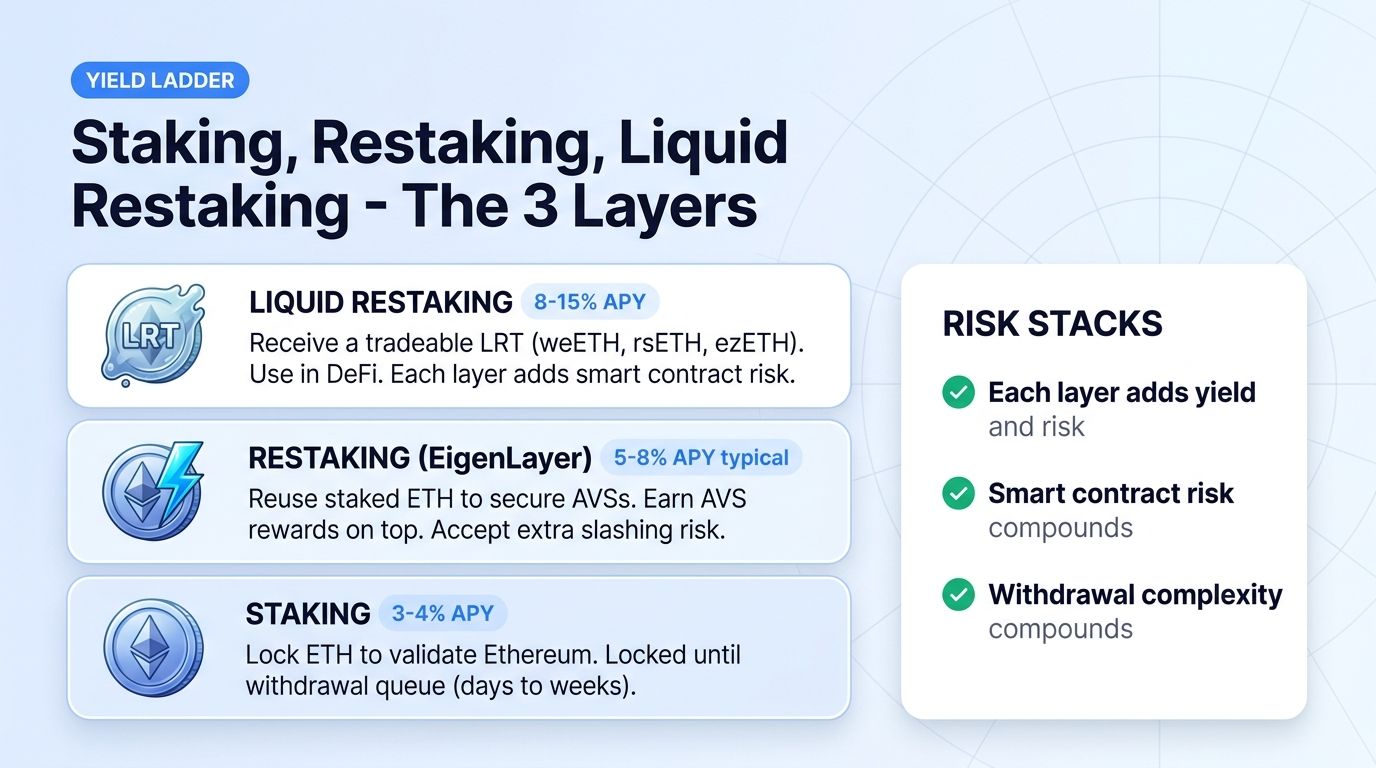

Staking means locking ETH into Ethereum's proof-of-stake system to help validate blocks. You earn rewards in ETH. The base rate has been roughly 3-4% APY in 2025-2026 depending on network conditions. Your ETH is locked until you withdraw, with an exit queue that can take days to weeks.

Restaking means taking your already-staked ETH and using it to also secure additional services on top of Ethereum. EigenLayer is the protocol that introduced this. Services that build on EigenLayer (called Actively Validated Services, or AVSs) pay restakers in their own tokens or fees in exchange for the borrowed security guarantee. You earn the base staking yield plus AVS rewards. You also accept additional slashing risk if you fail to validate the AVS correctly.

Liquid restaking means using a liquid restaking token (LRT) protocol like ether.fi, Kelp DAO, or Renzo. You deposit ETH or stETH, the protocol restakes on your behalf, and you receive a tradable LRT (weETH, rsETH, ezETH) representing your position. You can use the LRT in DeFi, sell it, or hold it for yield. You delegate operational decisions to the LRT protocol.

Each layer adds yield and adds risk. Each layer also adds smart contract dependencies.

Why Liquid Restaking Took Off

EigenLayer launched the restaking primitive in 2023. Until then, ETH security could only secure Ethereum. EigenLayer let AVS developers borrow that security by paying restakers. New AVSs (data availability layers, oracle networks, cross-chain bridges) launched with day-one security backed by billions in restaked ETH.

The base experience was operationally complex. You had to delegate to specific operators, choose which AVSs to validate, and manage withdrawal queues. Most retail users would not bother.

Liquid restaking protocols solved that. ether.fi launched in early 2024 and became the dominant LRT by TVL. Kelp DAO and Renzo followed with different operational profiles. By 2026, LRTs collectively held tens of billions in TVL. Yield stacking reached 10-15% APY for users willing to accept the layered risk.

The result: a yield product positioned between low-risk staking (3-4%) and higher-risk DeFi (15%+). For ETH holders who wanted more than base staking but less than memecoin volatility, liquid restaking filled an obvious gap.

The Major Liquid Restaking Protocols

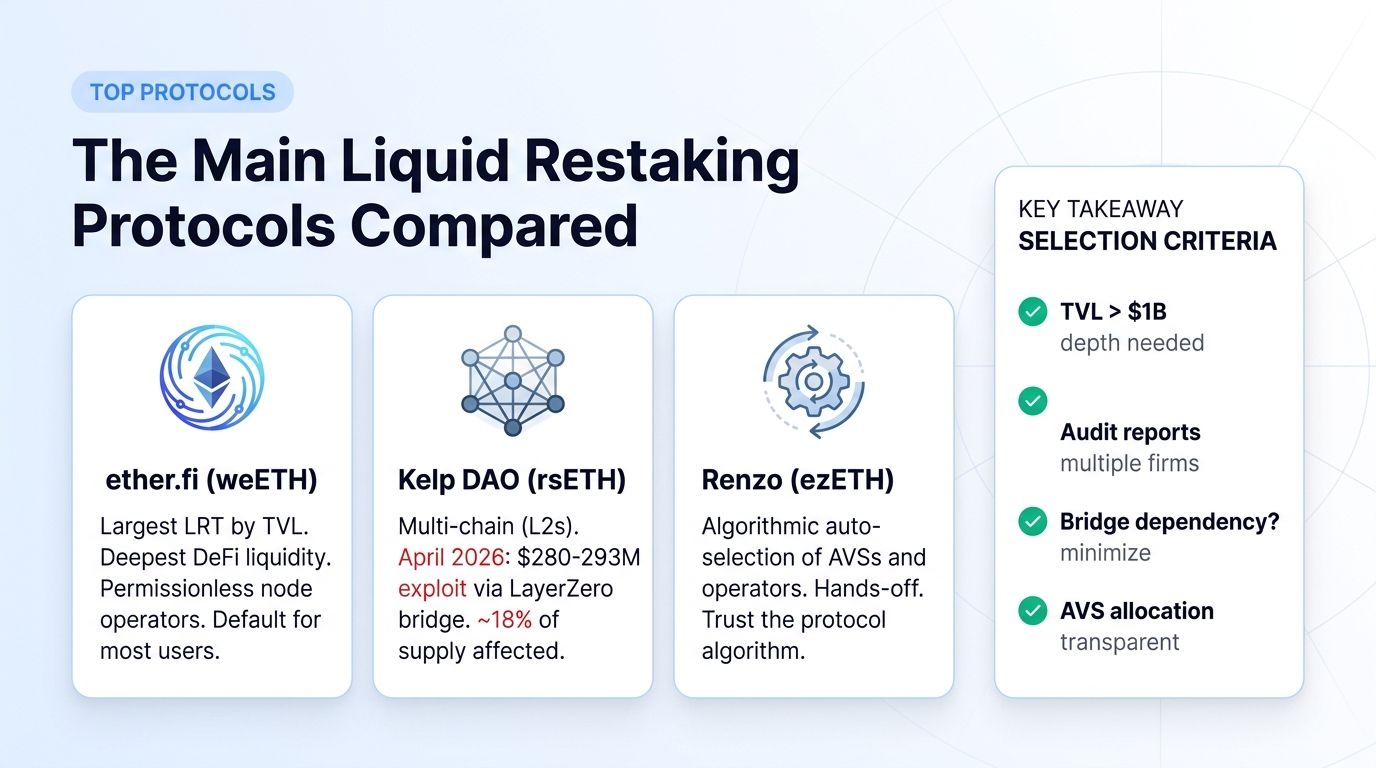

ether.fi (weETH)

ether.fi is the largest LRT by TVL and the deepest liquidity in DeFi. weETH is accepted as collateral on more lending platforms than any other LRT. The protocol uses a permissionless node operator model where anyone can run a node and earn rewards. weETH is the default LRT for most users in 2026 because of its DeFi composability.

Kelp DAO (rsETH)

Kelp focuses on multi-chain availability. rsETH is bridged to Ethereum Layer 2 networks including Arbitrum and Optimism, with lower gas fees for active DeFi users. Kelp's appeal was the L2 availability and integration with Polygon, BNB Chain, and others.

The April 2026 exploit changed Kelp's trust profile significantly. The vulnerability was in the LayerZero cross-chain adapter, not in the Kelp contract itself, but $280-293 million of rsETH was drained or made unbacked on multiple chains. Roughly 18% of the rsETH supply (116,500 tokens) was affected. Kelp continues operating and has been working on remediation, but the incident is a reminder that bridge dependencies are real attack surface.

Renzo (ezETH)

Renzo runs an algorithmic, hands-off restaking model. The protocol automatically selects AVSs and operators based on yield and risk parameters set by the protocol team. ezETH is suitable for users who want exposure without managing AVS decisions themselves. Renzo's design has been operationally smooth but the algorithmic selection introduces protocol-decision risk separate from individual user discretion.

Other Options

Puffer, Eigenpie, and several smaller LRTs compete on niche features (DVT integration, MEV redistribution, specific AVS partnerships). For most retail users in 2026, ether.fi, Kelp, and Renzo cover the practical options.

How to Access Liquid Restaking

Three paths.

Path 1: Deposit on the LRT protocol directly. Connect a wallet to ether.fi, Kelp, or Renzo. Deposit ETH or stETH. Receive the LRT. This is the cleanest path and gives you the protocol's full yield. Use Arbitrum or Optimism deployments if available to keep gas low.

Path 2: Buy the LRT on a DEX. weETH, rsETH, and ezETH trade on Uniswap, Curve, and similar venues. You can buy directly with USDC or other stables. This skips the deposit step but you pay slippage and may trade at a small discount or premium to NAV.

Path 3: Use the LRT as collateral in DeFi. Once you hold weETH or another major LRT, you can use it on lending markets like Aave to borrow stables or other assets. This is where the additional capital efficiency comes in, but it adds liquidation risk on top of all the restaking risks.

The Risks You Need to Understand

Smart contract risk, layered. When you hold an LRT, your capital depends on the LRT contract, the underlying EigenLayer contract, and the contracts of every AVS your restaking is delegated to. A bug at any layer can cause losses. Kelp's April 2026 exploit was at the bridge layer, which most users had not even considered.

Slashing risk. EigenLayer's AVSs can slash restaked ETH if the operator fails to validate correctly or acts maliciously. Slashing risk is inherited by every restaker who delegates to that operator. Read which AVSs the LRT delegates to and what their slashing conditions are.

LRT depegging. LRT prices can drift from the underlying ETH-equivalent value during market stress. A 5-10% depeg is not unusual when liquidations cascade through DeFi. If you use the LRT as leverage collateral, even a small depeg can trigger liquidations.

Withdrawal queue risk. Restaking withdrawals go through EigenLayer's escrow period (typically 7-14 days) plus the LRT protocol's internal queue. In a stressed market, exits can be slow or temporarily unavailable. The LRT trades on a secondary market in the meantime, often at a discount.

Centralization risk in AVS selection. Many LRT protocols make decisions about which AVSs to delegate to. You inherit those decisions. If the protocol chooses a poorly designed AVS, your position carries that AVS's risk profile without your individual approval.

Regulatory risk. Liquid restaking yields may be classified as securities-like products in some jurisdictions. The Kelp exploit and similar incidents have drawn regulatory attention to LRT structures.

How Liquid Restaking Fits Into a Crypto Portfolio

A practical framework for ETH holders:

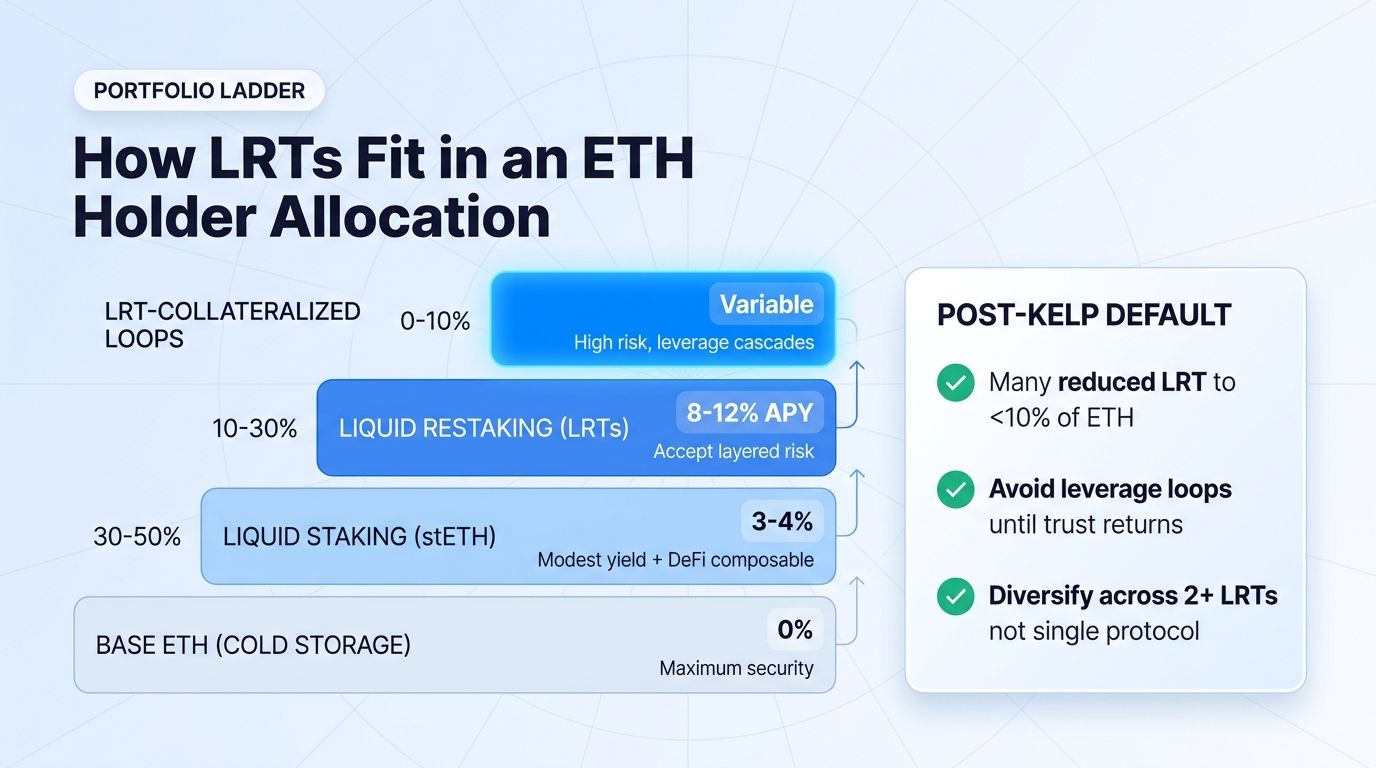

- Base ETH (cold storage or self-custody): 30-50% of ETH allocation. Maximum security, no yield. The foundation.

- Standard liquid staking (stETH from Lido or similar): 30-50%. Modest yield (3-4% APY), strong DeFi composability, lower risk than restaking.

- Liquid restaking (weETH, rsETH, ezETH): 10-30%. Higher yield (8-12% APY typical), accept the layered risks for the additional return.

- Aggressive DeFi (LRT-collateralized loops): 0-10%. Only if you understand liquidation cascades and accept the possibility of total loss on that portion.

The right allocation depends on your time horizon, your other portfolio holdings, and how much active risk management you can do. After the Kelp exploit, many traders reduced LRT exposure to single-digit percentages of total ETH.

FAQ

What is the difference between staking and restaking?

Staking secures Ethereum and earns ETH rewards (3-4% APY). Restaking takes your already-staked ETH and uses it to also secure additional services (AVSs) on top of Ethereum via EigenLayer, earning AVS rewards on top. Restaking adds yield and adds slashing risk.

Are LRTs the same as stETH?

No. stETH is a liquid staking token from Lido, representing staked ETH. LRTs (weETH, rsETH, ezETH) represent restaked ETH. LRTs have higher yield potential but more layered smart contract dependencies and additional slashing exposure.

Is liquid restaking safe after the Kelp exploit?

Liquid restaking continues to operate. The Kelp incident exposed a specific vulnerability in cross-chain bridge integration, not a flaw in EigenLayer or the broader restaking model. Most LRTs still hold billions in TVL. But the incident is a fair warning that bridge dependencies and layered smart contract risks are not theoretical.

Can I use Altrady to manage LRT positions?

Altrady's crypto trading platform focuses on centralized exchange integration across 19+ exchanges. LRTs are typically held in self-custody wallets and used on DeFi protocols. If you trade the wrapped versions on a CEX (where they are listed), you can view those positions in Altrady alongside other crypto. For on-chain DeFi management of LRTs, you need a wallet and DeFi interfaces directly.

What yield should I realistically expect from liquid restaking?

In 2026, typical liquid restaking yields run 8-12% APY, with some periods spiking to 15%+ during high AVS demand. Compare this to standard liquid staking at 3-4% APY and base ETH at 0%. Your effective yield depends on which AVSs the LRT delegates to and how those AVS reward structures perform.

Conclusion

Liquid restaking turned EigenLayer's complex restaking primitive into a one-click yield product for ETH holders. The promise is real: 8-15% APY on capital that previously earned 3-4% or nothing. The risks are also real, and the Kelp exploit in April 2026 demonstrated exactly how those risks materialize when bridge or contract vulnerabilities meet large TVL.

For traders, the practical takeaway is this: liquid restaking is a yield strategy with layered dependencies. The extra 4-10% APY over base staking is real, but you accept smart contract risk at multiple layers, slashing exposure, depeg risk, and withdrawal-queue risk for the privilege. Size the position to a level where a worst-case loss does not damage your overall portfolio.

The category will continue to mature. New LRTs will launch. Security models will improve. But the lesson from 2026's largest DeFi exploit is permanent: yield comes with risk, and risk is rarely visible until it shows up.