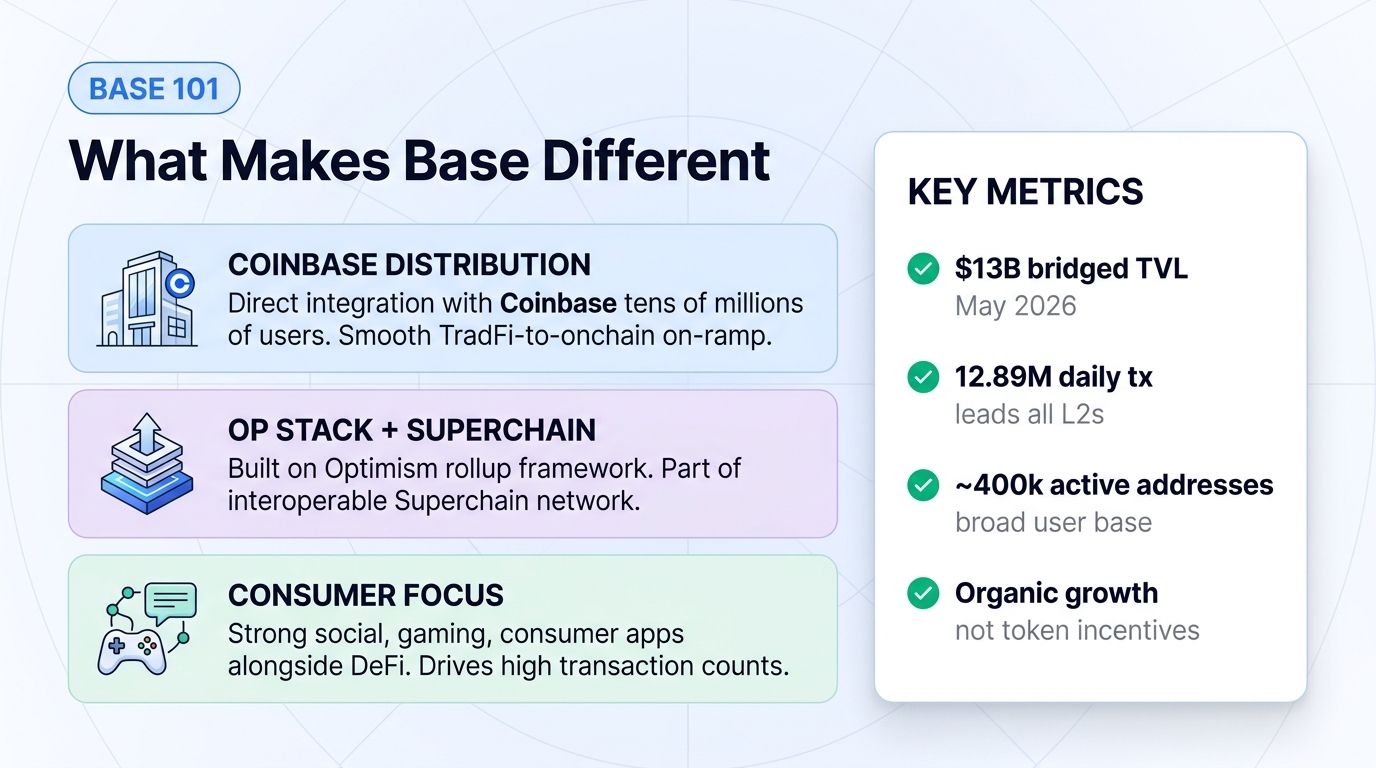

Base, the Ethereum Layer 2 network incubated by Coinbase, has become one of the defining infrastructure stories of the 2024-2026 crypto cycle. As of early May 2026, Base surpassed $13 billion in bridged total value locked, with roughly $4.49 billion in DeFi-specific TVL. The network now leads all Ethereum Layer 2s in daily transaction volume at approximately 12.89 million transactions per day, and records nearly 400,000 active addresses, reflecting one of the broadest user bases in the L2 category.

The growth trajectory is striking. Base expanded from approximately $2.1 billion in TVL in October 2024 to between $10.7 billion and $12.8 billion by May 2026, roughly a five-fold increase in 18 months. Notably, this growth has been largely organic, driven by Coinbase's distribution advantage and ecosystem applications rather than aggressive token incentive programs.

This guide explains what Base is, why it matters in the broader L2 landscape, the ecosystem driving its growth, the no-token question, the competitive position against Arbitrum, and how traders should think about Base exposure.

What Is Base?

Base is an Ethereum Layer 2 network built on the OP Stack, the open-source rollup framework developed by Optimism. It was incubated by Coinbase, the largest US crypto exchange, and launched to the public in 2023. Base operates as an optimistic rollup, batching transactions off-chain and posting compressed data and proofs back to Ethereum mainnet for security.

The network has three core characteristics that distinguish it.

First, Coinbase distribution. Base benefits from direct integration with Coinbase's product ecosystem, which serves tens of millions of users. This provides a uniquely smooth on-ramp from traditional finance into on-chain activity. Coinbase's Smart Wallet and various consumer products route activity to Base.

Second, OP Stack foundation and the Superchain. Base is part of the broader Optimism Superchain, a network of interoperable OP Stack chains. This shared infrastructure provides technical maturity and a path toward cross-chain interoperability with other Superchain members.

Third, consumer and social focus. While many L2s emphasize pure DeFi, Base has cultivated strong consumer, social, and gaming applications alongside its DeFi ecosystem. This broad application mix drives high transaction counts and a diverse user base.

Why Base Matters in the 2026 L2 Landscape

Three structural factors explain Base's prominence.

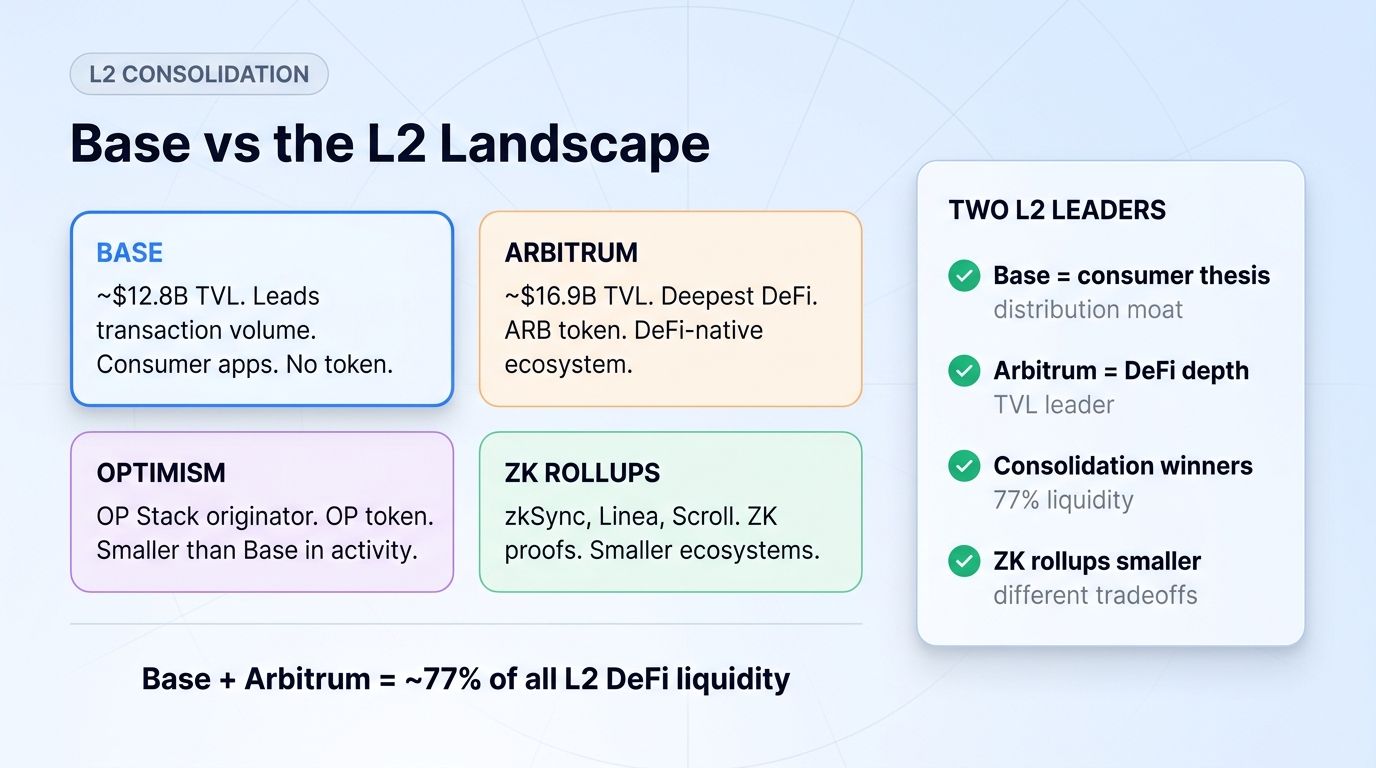

First, the L2 consolidation thesis. By 2026, the Ethereum Layer 2 ecosystem has consolidated around a few dominant players. Arbitrum One holds approximately $16.9 billion in TVL while Base follows at roughly $12.8 billion. Together, these two networks account for approximately 77 percent of all L2 DeFi liquidity. The era of dozens of competing L2s with fragmented liquidity is giving way to a winner-concentration dynamic, and Base is one of the two clear leaders.

Second, organic growth without token incentives. Many L2s bootstrapped TVL through aggressive token airdrops and liquidity mining incentives, which often produced mercenary capital that fled once incentives ended. Base grew primarily through genuine application usage and Coinbase distribution. This organic growth is generally considered more durable than incentive-driven TVL.

Third, the consumer crypto narrative. Base leads in transaction volume largely because of consumer, social, and gaming applications. As crypto adoption broadens beyond pure financial speculation toward consumer use cases, Base's positioning aligns with where new user growth is concentrated.

For traders, Base represents exposure to the L2 consolidation winner with the strongest consumer-distribution moat.

The Base Ecosystem in 2026

Several categories of activity drive Base usage.

DeFi Protocols

Base hosts a comprehensive DeFi ecosystem with $4.49 billion in TVL. Major protocols include decentralized exchanges, lending platforms, yield aggregators, and derivatives venues. The network's 24-hour DEX volume reaches approximately $655 million, with perpetual trading volume near $154 million. Aerodrome (a leading Base-native DEX), along with deployments of major cross-chain protocols, anchor the DeFi activity.

Consumer and Social Applications

Base's distinguishing feature is its consumer and social application layer. Social protocols, content platforms, and creator-economy applications generate significant transaction volume. This consumer activity is what pushes Base to the top of the L2 transaction-count rankings.

Gaming

On-chain gaming applications contribute to Base's high transaction throughput. The combination of low fees and Coinbase distribution makes Base attractive for gaming developers seeking mainstream reach.

Stablecoin Payments

Base has become a significant venue for stablecoin activity, particularly USDC (which Circle, the USDC issuer, supports natively on Base). The combination of low transaction costs and Coinbase integration makes Base attractive for payment use cases.

The No-Token Question

One of the most distinctive aspects of Base is that it has not launched a native token. This stands in contrast to most other major L2s, including Arbitrum (ARB), Optimism (OP), and others, which all have governance and incentive tokens.

Coinbase has repeatedly stated that Base has no plans to issue a token. This has several implications.

For traders, it means there is no direct Base token to hold. Exposure to Base must come indirectly through ecosystem tokens, Coinbase equity (COIN), or ETH (since Base settles to Ethereum and pays fees in ETH).

For the ecosystem, the absence of a token removes the speculative token-incentive dynamic that has both helped and harmed other L2s. Base's growth is not propped up by token emissions, which supports the organic-growth durability thesis but removes a potential catalyst for speculative capital inflows.

The no-token stance could change in the future, and speculation about a potential Base token periodically circulates. However, as of 2026, no token exists, and traders should not position around an unconfirmed token launch.

How Base Compares to Other L2s

The L2 landscape has consolidated around several major players.

Base vs Arbitrum: Arbitrum leads in raw DeFi TVL (~$16.9B vs ~$12.8B) and has a more mature DeFi-native ecosystem. Base leads in transaction volume and consumer applications, and has the Coinbase distribution advantage. Arbitrum has the ARB token; Base has no token.

Base vs Optimism: Both are OP Stack chains in the Superchain. Optimism (OP token) is the originator of the OP Stack. Base has grown larger than the Optimism mainnet chain in most activity metrics, despite being built on Optimism's technology.

Base vs zkSync, Linea, Scroll (ZK rollups): These use zero-knowledge proof technology rather than optimistic rollups. They offer different technical tradeoffs (faster finality, different security models) but have smaller ecosystems than Base.

Base vs Solana (alt-L1): Solana is a separate Layer 1, not an Ethereum L2. It competes with Base for consumer and high-throughput applications but operates on entirely different infrastructure.

For traders, the practical takeaway is that Base and Arbitrum are the two L2 leaders, with Base offering the consumer-distribution thesis and Arbitrum offering the DeFi-depth thesis.

How Traders Can Get Base Exposure

Three practical paths.

Path 1: Hold ETH. Since Base settles to Ethereum and uses ETH for gas, broad Base ecosystem growth indirectly supports ETH demand. ETH is the most direct liquid proxy for L2 ecosystem activity. A platform like Altrady connects to 19+ exchanges for unified ETH position management.

Path 2: Hold Base ecosystem tokens. Tokens of major Base-native protocols (Aerodrome's AERO and others) provide concentrated exposure to Base DeFi activity. Higher risk than ETH but more directly tied to Base-specific growth.

Path 3: Hold Coinbase equity (COIN). For investors comfortable with traditional equities, COIN provides exposure to Coinbase's overall business, including the strategic value of Base. This is an indirect and diversified path rather than pure Base exposure.

The Risks of Base Exposure

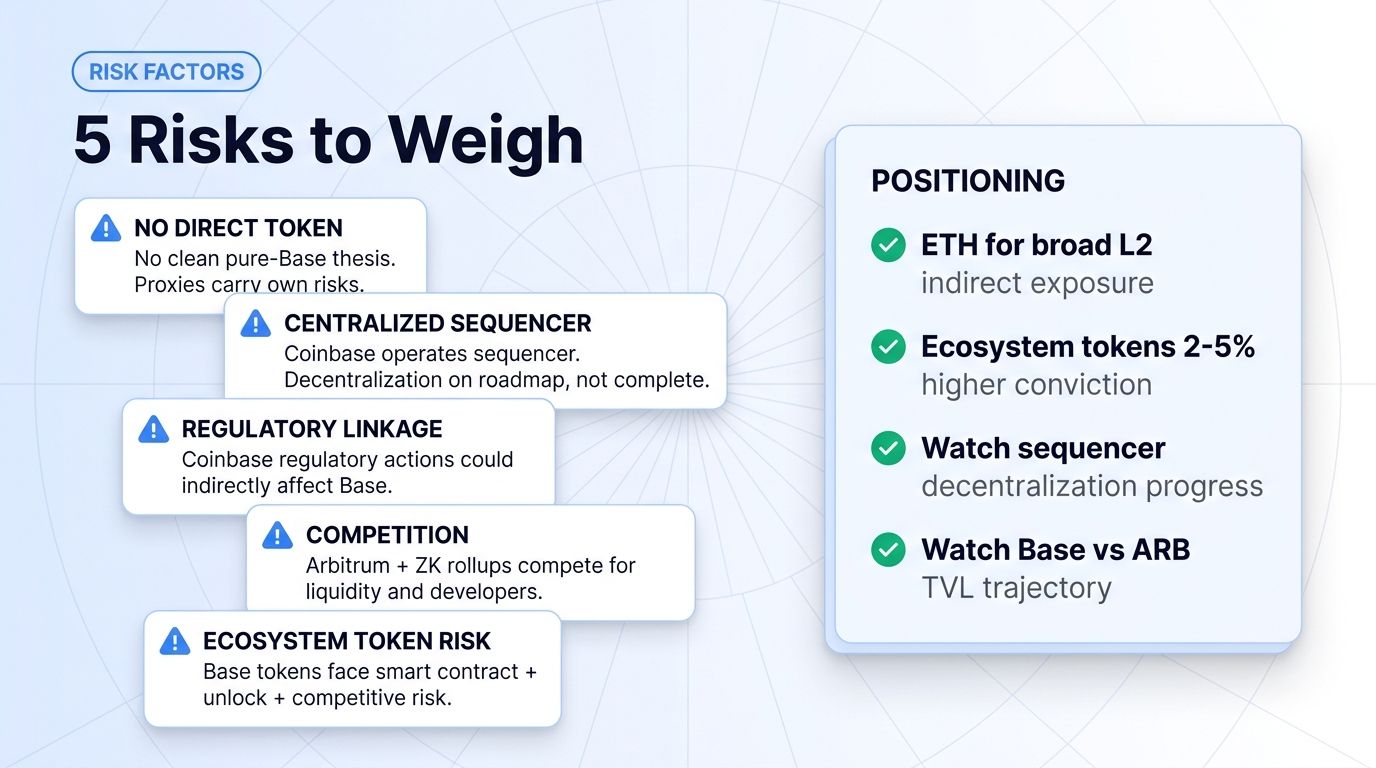

No direct token risk. The absence of a Base token means there is no clean way to express a pure Base thesis. Indirect proxies (ETH, ecosystem tokens, COIN) each carry their own additional risk factors.

Centralization concerns. Base, like most optimistic rollups in 2026, still relies on a centralized sequencer operated by Coinbase. Decentralization of the sequencer is on the roadmap but not yet complete. This creates a degree of operational dependency on Coinbase.

Regulatory risk. Base's tight association with Coinbase means regulatory actions affecting Coinbase could indirectly affect Base. Coinbase's regulatory standing has improved through 2025-2026, but the linkage is a risk factor.

Competitive risk. Arbitrum and emerging ZK rollups compete for liquidity and developers. The L2 landscape could shift if technical or ecosystem advantages emerge elsewhere.

Ecosystem token risk. Base ecosystem tokens are subject to the standard risks of DeFi tokens: smart contract vulnerabilities, token unlocks, and competitive pressure.

How Base Fits Into a Crypto Portfolio

A practical framework:

- Core large-cap holdings (BTC, ETH): 50-65% of crypto allocation. ETH allocation captures indirect L2 growth.

- L2 ecosystem exposure: 5-15%. This can include ARB, OP, and Base ecosystem tokens (AERO, others).

- Base-specific ecosystem tokens: 2-5%. Concentrated positions for higher Base conviction.

- Cash reserves: 5-15%

Since Base has no token, the most direct portfolio expression of a Base thesis is through ETH (broad), Base ecosystem tokens (concentrated), or COIN equity (diversified).

What to Watch in the Next 12 Months

Three indicators.

Indicator 1: TVL trajectory vs Arbitrum. Does Base close the gap with Arbitrum, or does Arbitrum maintain its DeFi TVL lead? The relative trajectory signals which L2 thesis is winning.

Indicator 2: Sequencer decentralization progress. Does Base make progress on decentralizing its sequencer? This is a key milestone for reducing centralization risk.

Indicator 3: Token launch signals. Does Coinbase change its no-token stance? Any movement here would be a major catalyst, though traders should not position around speculation.

If Base continues growing transaction volume and ecosystem depth while making decentralization progress, it consolidates its position as a top-two L2. If competitors gain ground, the consolidation dynamic could shift.

FAQ

Does Base have a token?

No. As of 2026, Base has not launched a native token, and Coinbase has repeatedly stated it has no plans to issue one. This contrasts with most other major L2s like Arbitrum (ARB) and Optimism (OP). Exposure to Base must come indirectly through ETH, Base ecosystem tokens, or Coinbase equity.

Is Base built on Ethereum?

Yes. Base is an Ethereum Layer 2 built on the OP Stack (Optimism's rollup framework). It batches transactions off-chain and posts data back to Ethereum mainnet for security. It uses ETH for gas and settles to Ethereum.

How does Base compare to Arbitrum?

Arbitrum leads in DeFi TVL (~$16.9B vs Base's ~$12.8B), while Base leads in daily transaction volume and consumer applications. Base has the Coinbase distribution advantage but no token; Arbitrum has the ARB token and deeper DeFi ecosystem. They are the two dominant L2s, holding roughly 77 percent of L2 DeFi liquidity combined.

Why is Base growing so fast?

Base's growth is driven primarily by Coinbase's distribution advantage (tens of millions of users with smooth on-ramps) and its consumer, social, and gaming application ecosystem, rather than token incentives. This organic growth is generally considered more durable than incentive-driven TVL.

Can I trade Base ecosystem tokens on Altrady?

Base ecosystem tokens that are listed on major exchanges can be managed through Altrady. Altrady connects to 19+ exchanges, so you can manage positions in ETH and listed Base ecosystem tokens alongside other crypto holdings, run automated strategies via the signal bot, grid bot, or DCA bot, and use unified portfolio tracking.

Conclusion

Base has established itself as one of the two dominant Ethereum Layer 2 networks of the 2024-2026 cycle. With over $13 billion in bridged TVL, category-leading transaction volume, and nearly 400,000 active addresses, Base demonstrates the power of Coinbase's distribution advantage combined with a consumer-focused application ecosystem.

For traders, the practical takeaway is this: Base represents the consumer-distribution thesis in the L2 consolidation, but the absence of a native token means exposure must come indirectly through ETH, ecosystem tokens, or Coinbase equity. The organic, incentive-light growth is a positive durability signal.

The longer-term trajectory depends on whether Base can continue closing the TVL gap with Arbitrum, make progress on sequencer decentralization, and maintain its consumer-application lead. The next 12 months will produce decisive data on the L2 consolidation winners.

For diversified crypto portfolios, the cleanest expression of a Base thesis is through ETH for broad L2 exposure, supplemented by select Base ecosystem tokens for higher conviction. Sizing positions appropriately based on the indirect nature of Base exposure remains the standard discipline.