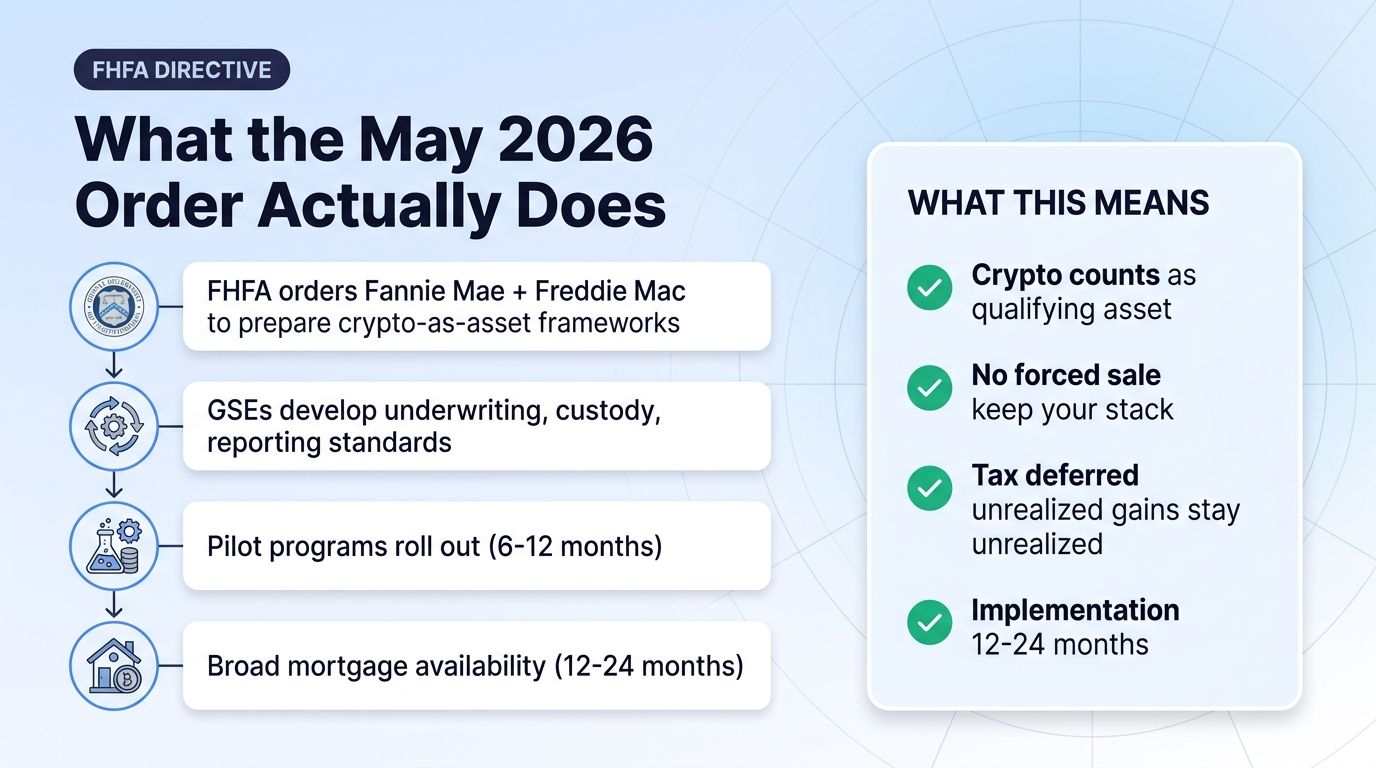

In May 2026, the Director of the Federal Housing Finance Agency (FHFA) ordered Fannie Mae and Freddie Mac to "prepare their businesses to count cryptocurrency as an asset for a mortgage." For crypto holders who want to buy a home, the announcement changed what had been a structural obstacle into a clearer path.

The directive does not make crypto-backed mortgages instantly available at every lender. It signals a multi-year process during which the two government-sponsored enterprises (GSEs) develop the underwriting, custody, and reporting frameworks for crypto-as-asset. But the policy shift is structural and creates a major opportunity for crypto holders who had previously been forced to convert their holdings to dollars to qualify for a home loan.

This guide explains what the FHFA directive does, how crypto-backed mortgages will work in practice, who benefits, the open questions still to be resolved, and the practical steps crypto holders should take if they plan to buy a home in 2026-2028.

What the FHFA Directive Says

The directive applies to Fannie Mae and Freddie Mac, the two GSEs that back the majority of US conforming mortgages. Together they purchase or guarantee roughly half of all US home loans.

The directive orders the GSEs to: - Develop frameworks for counting crypto holdings as qualifying assets for mortgage underwriting - Coordinate with custodians and reporting infrastructure - Provide implementation timelines and pilot programs - Report progress to the FHFA on a regular cadence

The directive does not specify exact rules. Implementation details are delegated to the GSEs, which will work with the Treasury, banking regulators, and mortgage industry stakeholders to design the operational framework.

For mortgage borrowers, the practical effect is gradual. Most lenders cannot immediately accept crypto as a qualifying asset for a Fannie Mae or Freddie Mac mortgage. But the policy direction is set, and within 12-18 months, pilot programs and then broader availability are expected.

Why the Directive Matters in 2026

Three forces converged to make the change politically and economically necessary.

First, crypto adoption reached scale. With 67 million Americans now holding digital assets according to the National Cryptocurrency Association, the population of mortgage applicants holding crypto is no longer marginal. Excluding crypto from mortgage underwriting denied a growing share of qualified borrowers access to home loans.

Second, the institutional infrastructure for custody and reporting matured. Custody platforms (Coinbase Custody, Anchorage, BitGo, Fidelity Digital Assets) provide auditable holding records. Tax reporting infrastructure (Form 8949, exchange reporting) provides verifiable transaction histories. The operational infrastructure that the GSEs need to verify crypto assets now exists.

Third, the broader regulatory environment shifted. The CLARITY Act, expected to be signed in July 2026, provides legal clarity for crypto custody, reporting, and asset classification. The FHFA directive aligns with the broader policy direction.

For traders and crypto holders, the change is significant. Mortgage qualification typically requires demonstrating sufficient assets, income, and reserves. Crypto holdings that were previously invisible to lenders now count toward qualification.

How Crypto-Backed Mortgages Will Work

The framework is still being developed, but the operational pieces are visible.

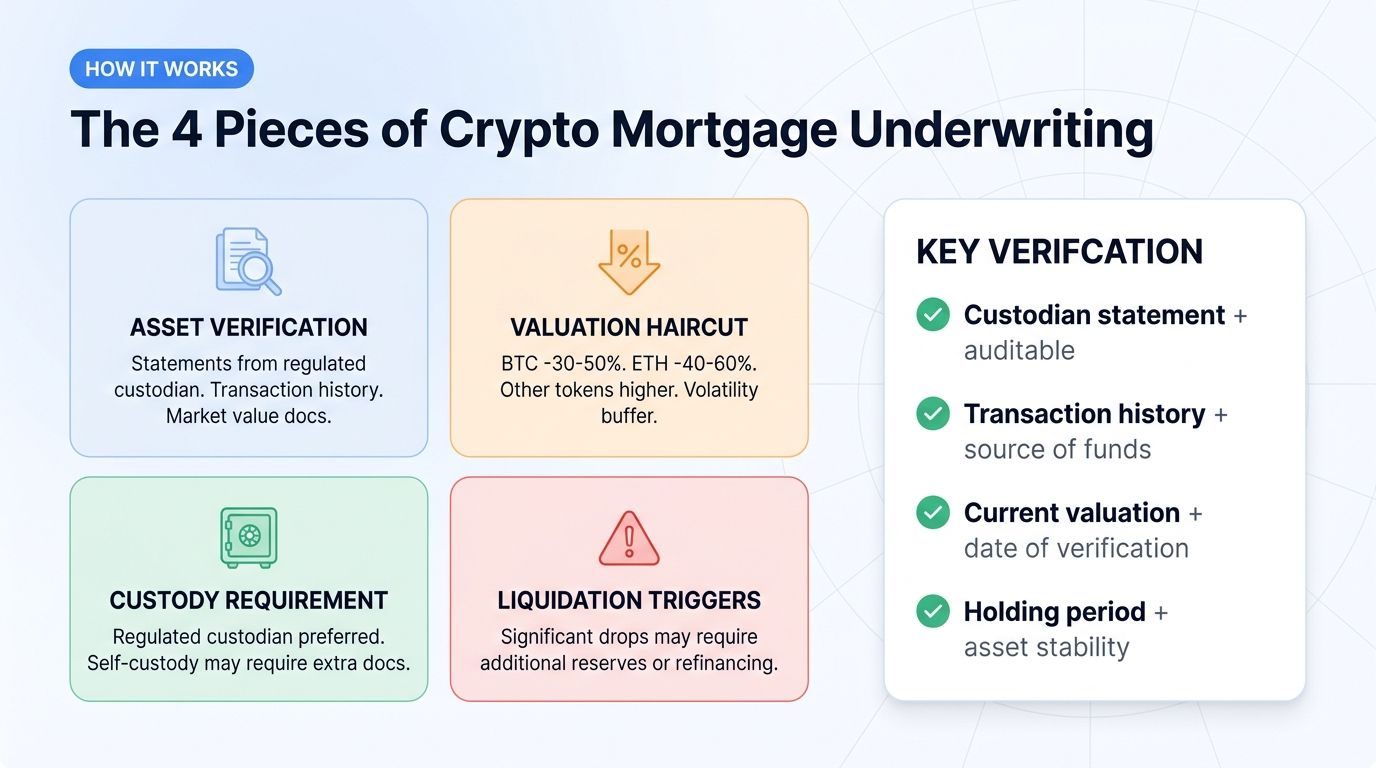

Asset Verification

Lenders need to verify that the borrower holds the claimed crypto assets. This typically requires: - Account statements from a regulated custodian (exchange, custodian platform, or qualified wallet) - Transaction history showing the source of funds - Current market value documentation, typically using exchange-published prices on the verification date

The verification process is similar to verifying brokerage holdings for stocks, with crypto-specific adjustments for the volatility and custody mechanics.

Valuation Haircuts

Crypto assets are volatile. Lenders are expected to apply discount factors (haircuts) when counting crypto toward mortgage qualification. Industry expectation is that bitcoin may be discounted 30-50% from current market value, ethereum 40-60%, and other tokens at higher discount rates. The exact haircuts will depend on GSE-published guidelines.

Custody Requirements

Many lenders will likely require that crypto used as qualifying assets be held with a regulated custodian rather than in self-custody. This provides verification and reduces dispute risk. Self-custody crypto may face stricter documentation requirements or higher haircuts.

Liquidation Triggers

If crypto used to qualify for a mortgage falls significantly in value during the underwriting process or shortly after closing, lenders may require additional reserves or refinancing. The specific triggers will be defined in the GSE rules.

Who Benefits Most

Three groups gain the most from the FHFA directive.

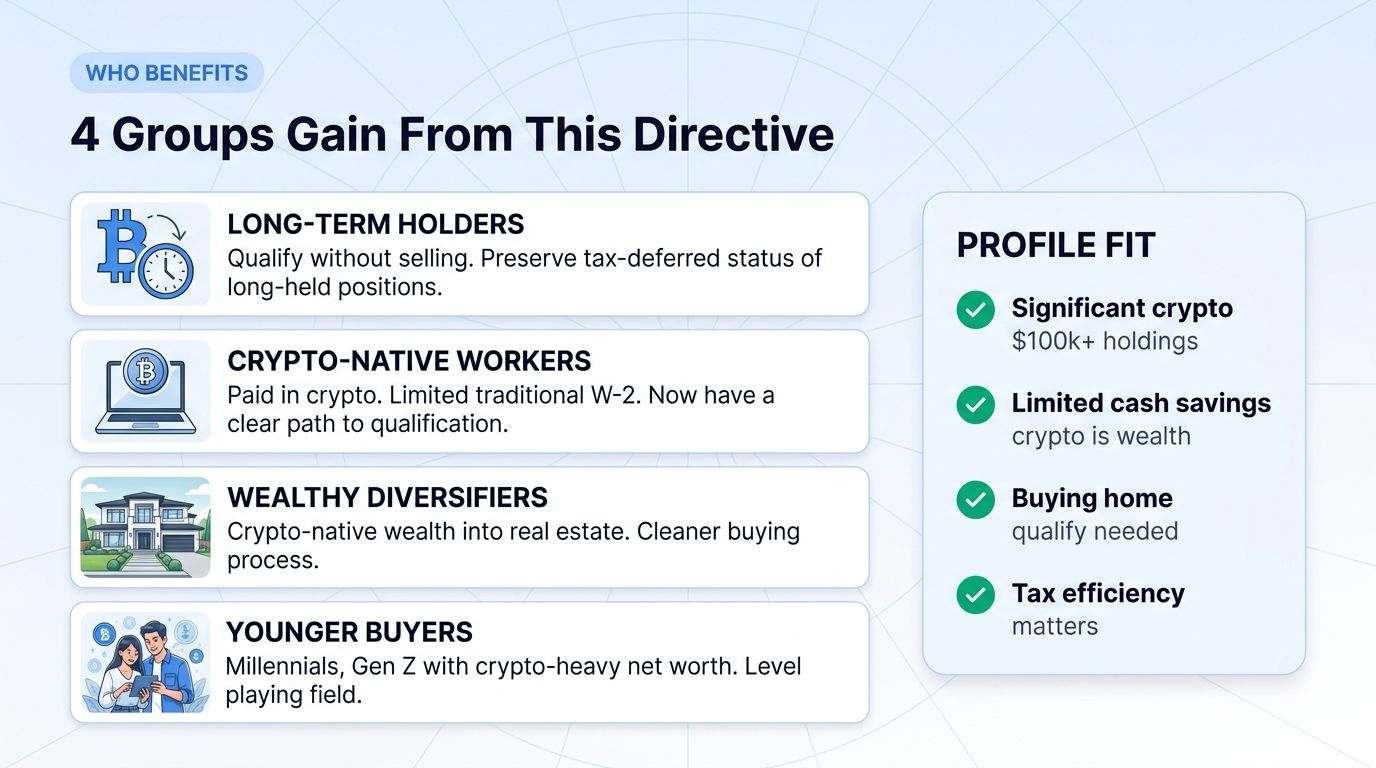

Long-Term Bitcoin Holders

Crypto holders who have held bitcoin for several years and have substantial unrealized gains face a tax dilemma: selling to qualify for a mortgage triggers capital gains tax. The new framework allows them to qualify without selling, preserving the tax-deferred status of long-held positions.

A holder with $500,000 in bitcoin acquired at $200,000 cost basis previously had to sell some portion (incurring $30,000-$50,000+ in capital gains tax) to qualify for a $1 million mortgage. The new framework may allow qualification while keeping the bitcoin in custody.

Crypto-Native Workers

Workers paid in crypto (developers, marketers, founders in the crypto industry) often have substantial crypto holdings but limited traditional W-2 income or banking history. The new framework provides a path to mortgage qualification that matches their actual financial situation.

Wealthy Crypto Holders Diversifying Real Estate

Crypto-native wealth has been one of the major buyer categories in luxury real estate markets (Miami, Austin, parts of California). The new framework makes the buying process cleaner by reducing the need to convert and explain large dollar transfers.

Younger Buyers with Crypto-Heavy Net Worth

Millennials and Gen Z buyers who concentrated wealth in crypto rather than traditional assets had been disadvantaged in mortgage underwriting. The new framework levels this playing field.

The Practical Steps for Crypto Holders Planning to Buy

Three concrete actions.

Step 1: Custody with a regulated provider. Move crypto intended for mortgage qualification from self-custody or smaller exchanges to a major regulated custodian. The exact list of qualifying custodians will be defined by the GSEs, but Coinbase, Kraken, Gemini, Fidelity Digital Assets, BitGo, and Anchorage are likely to be included.

Step 2: Maintain clean transaction records. Source of funds documentation is critical. Save records of every purchase, including exchange records, bank transfers, and tax forms. This documentation will be required during mortgage application.

Step 3: Avoid major rebalancing right before applying. Lenders look at asset stability. Major sales or transfers in the 60-90 days before mortgage application can complicate underwriting. If you plan to apply for a mortgage in 2026-2027, consider stabilizing your crypto allocation 6+ months in advance.

For active traders managing positions across exchanges, a unified portfolio platform like Altrady (connecting to 19+ exchanges) helps maintain visibility into total holdings across platforms during the period leading up to a mortgage application.

The Open Questions

Several issues remain unresolved.

Self-Custody Treatment

The framework's treatment of self-custody crypto (private wallets, hardware wallets) is not yet defined. Self-custody offers maximum security but creates verification challenges for lenders. Industry expectation is that self-custody will be permitted with additional documentation requirements (signed messages, transaction history attestations), but with potentially higher haircuts than custodian-held crypto.

Defi Holdings

Crypto held in DeFi protocols (lending platforms, liquidity pools, staking contracts) creates additional verification complexity. Whether and how these holdings count toward mortgage qualification is an open question. Initial frameworks are likely to count only spot holdings, with DeFi positions added in later phases.

Volatility-Driven Margin Calls

If a borrower's crypto holdings drop significantly after mortgage approval but before closing, what happens? The current expectation is that material drops (e.g., 30%+) may require additional reserves or could disqualify the application. Specific thresholds are not yet defined.

State-Level Variation

Different states have different mortgage and consumer protection rules. Some states may add additional requirements to crypto-backed mortgages. The federal framework provides the baseline, but state-level layering is likely.

How Crypto Mortgages Fit Into a Broader Strategy

A practical framework:

- Maintain liquid reserves separately: Even with crypto-as-asset accepted, lenders typically require liquid reserves (cash, money market funds) equal to 2-6 months of mortgage payments. Do not use crypto as your sole reserve.

- Plan the tax implications: Mortgage payments are typically made in dollars. If you intend to sell crypto periodically to fund mortgage payments, plan for the tax implications of those sales.

- Avoid over-leveraging: The new framework lets you keep crypto holdings while taking on mortgage debt. This is effectively leveraged exposure to both crypto and real estate. Size the mortgage to a level where worst-case crypto decline does not jeopardize the home.

- Consider tax-loss harvesting opportunities: If you have lower-cost-basis positions and higher-cost-basis positions, strategic selling of the higher-cost-basis positions for mortgage application proceeds can produce tax benefits.

The Broader Trend

The FHFA directive is part of a larger pattern. Major US institutions are increasingly accommodating crypto as a legitimate asset class: - Banks offer custody services to wealth-management clients - Brokerages list bitcoin and ethereum ETFs - Retirement platforms permit crypto allocations in 401(k) and IRA accounts - Now mortgage qualification accepts crypto as an asset

For long-term crypto holders, the cumulative effect is that crypto is becoming usable in traditional financial planning, not just held as a speculative position. This integration may take 2-5 years to fully materialize, but the direction is set.

The Risks of Crypto-Backed Mortgages

Volatility risk. Crypto values change daily. A mortgage qualified based on $500,000 of bitcoin may face complications if bitcoin drops 40% before closing. Borrowers should build buffer into their applications and avoid stretching to maximum qualification levels.

Tax complexity. Using crypto to qualify for a mortgage without selling preserves tax deferral. But future sales of that crypto (to fund mortgage payments, for example) trigger tax events. Plan with a CPA familiar with crypto taxation.

Custody risk. Holding crypto with a custodian during mortgage underwriting requires confidence in that custodian. Custodian failures (like FTX in 2022) can be catastrophic. Diversify across custodians for significant holdings.

Regulatory change risk. The framework is being developed under one administration and one FHFA director. Future administrations could revise or rescind the directive. Borrowers planning to use crypto for future home purchases should not assume the framework remains static.

Documentation burden. Source-of-funds documentation for crypto can be onerous, particularly for holders who acquired crypto across many transactions over many years. Engage with a tax professional who can help organize the records.

FAQ

When can I actually apply for a Fannie Mae or Freddie Mac mortgage using my crypto?

The FHFA directive was issued in May 2026. Pilot programs are expected within 6-12 months, with broader availability in 12-24 months. Specific timelines depend on the GSEs' implementation work and lender adoption.

Do I have to sell my crypto to qualify for a mortgage?

No, that's the central change. The new framework allows your crypto holdings to count as qualifying assets without requiring a sale. You can keep your crypto position while qualifying for a mortgage.

What discount factor will lenders apply to my crypto?

Specific haircuts are not yet published. Industry expectation is 30-50% discount for bitcoin, 40-60% for ethereum, higher for less-liquid tokens. The exact factors will be set by GSE guidelines and individual lenders.

Will this work for jumbo loans or only conforming mortgages?

The FHFA directive applies to Fannie Mae and Freddie Mac, which back conforming loans (currently up to $766,550 in most areas, higher in expensive markets). Jumbo lenders may follow with their own frameworks, but the FHFA directive itself does not cover jumbo loans.

Can I trade crypto on Altrady while qualifying for a mortgage?

Yes. Altrady connects to 19+ exchanges and provides unified portfolio tracking. Lenders typically want to see asset stability rather than zero activity, so continued trading is generally acceptable. Major liquidations or rebalancing right before application may complicate underwriting, but normal trading activity is not a barrier.

Conclusion

The FHFA's May 2026 directive is a structural milestone for crypto integration into traditional finance. For the millions of Americans who hold significant crypto wealth, the ability to qualify for a home mortgage without liquidating positions removes one of the most-painful tax and financial frictions in crypto ownership.

The framework is not instant. Implementation will take 12-24 months to reach broad availability. But the policy direction is set, and crypto holders planning home purchases in 2026-2028 should start positioning their holdings, custody arrangements, and documentation accordingly.

The takeaway for traders is this: crypto-as-asset is no longer a marginal classification. Real estate, the largest single asset for most American households, now joins retirement accounts, brokerage accounts, and savings as a category where crypto can serve as qualifying wealth. This unlocks a meaningful financial planning opportunity that did not exist a year ago.

The broader pattern continues. Each year, crypto integrates more deeply into the regulated financial system. Each integration unlocks new use cases, new buyer pools, and new institutional capital. The FHFA directive is one significant step in that ongoing process.