What Is Crypto Lending and Borrowing?

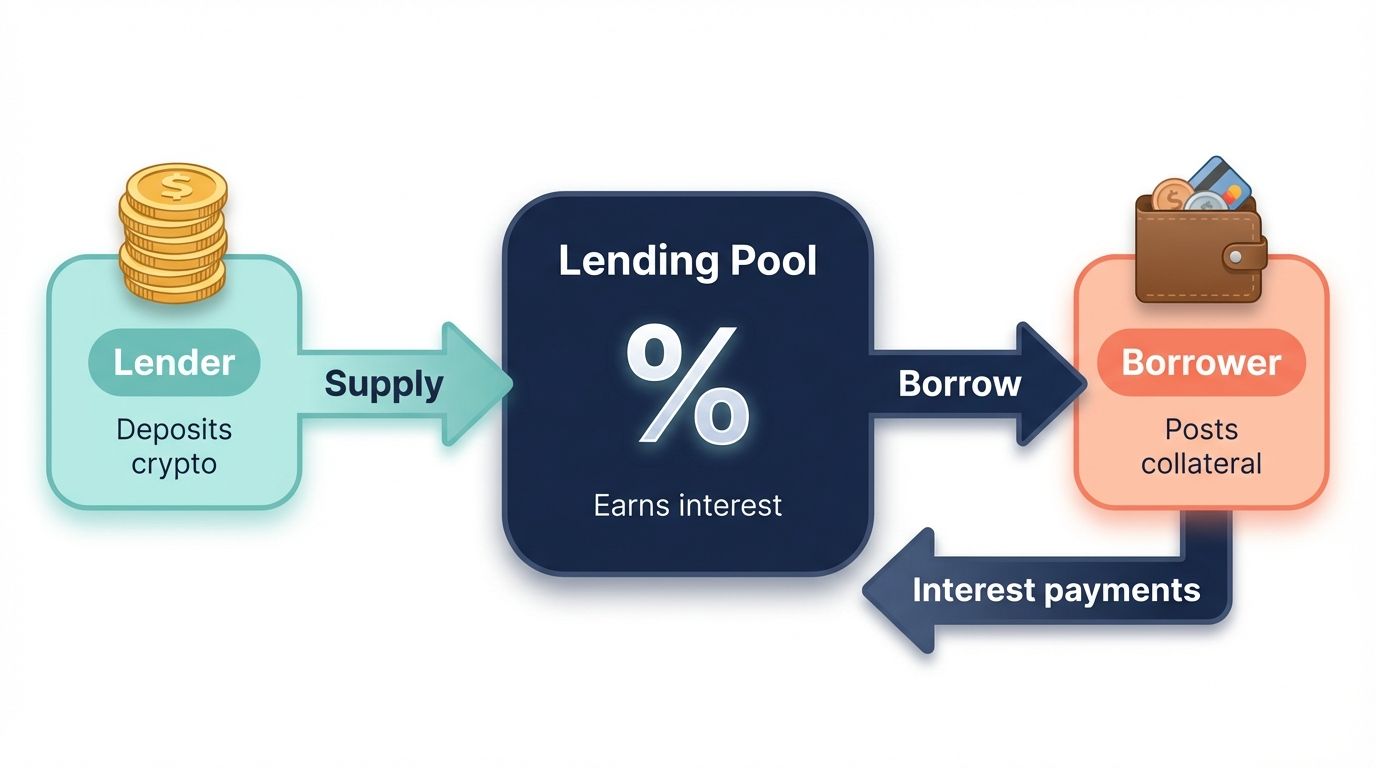

Crypto lending and borrowing is a financial mechanism that allows individuals to earn interest on idle digital assets or access liquidity without selling their holdings. At its core, the model is structurally similar to traditional banking: one party deposits assets and earns a yield, while another party borrows those assets and pays interest. The key difference is that the entire process can be automated through smart contracts, eliminating the need for a central authority like a bank.

In traditional finance, you might deposit money into a savings account earning 2% to 4% annually, while borrowers on the other end pay 8% to 20% for personal loans. The bank captures the spread. In crypto, that spread either goes to the protocol's treasury or is distributed differently, depending on the governance model. More importantly, rates in crypto can be dramatically higher or lower depending on market demand, token incentives, and liquidity conditions.

Crypto lending and borrowing exists in two primary environments: centralized finance (CeFi) and decentralized finance (DeFi). In CeFi, a company like Nexo or Ledn acts as the intermediary, taking custody of your assets and managing the lending process through its internal systems. In DeFi, smart contracts on blockchains like Ethereum, Avalanche, or Solana automate every step, from collateral management to interest accrual and liquidation, without any human intermediary.

Why does crypto lending exist at all? Several strong incentives drive it. Institutional traders need to borrow assets for short-selling or hedging. Long-term holders want liquidity without triggering a taxable sale. DeFi protocols need deep liquidity to function. Yield-seekers want their idle stablecoins or ETH to work harder than a traditional savings account offers. Each group has a clear reason to participate, and together they create a robust two-sided market that has grown to tens of billions of dollars in total value locked (TVL) across both CeFi and DeFi platforms.

By March 2026, crypto lending and borrowing has matured significantly. After the regulatory upheaval of 2022 through 2024, which saw several CeFi platforms collapse and DeFi protocols face security audits, the market has rebuilt on stronger foundations, with better risk models, clearer regulations in several jurisdictions, and more sophisticated tooling for participants on both sides of the market.

How Crypto Lending Works

Before you deposit a single token, it helps to understand exactly what happens to your assets once they enter a lending protocol or platform. The mechanics differ between CeFi and DeFi, but the core flow follows a consistent pattern: you supply assets, those assets are made available to borrowers, and you earn interest in return.

Depositing Assets as a Lender

On a DeFi platform like Aave or Compound, depositing assets is straightforward. You connect a non-custodial wallet, approve the protocol to interact with your tokens, and deposit your chosen asset into a liquidity pool. In return, you receive receipt tokens, known as aTokens on Aave or cTokens on Compound, which represent your share of the pool and automatically accrue interest in real time.

On a CeFi platform, the process resembles opening a savings account. You create an account, complete identity verification, and transfer your assets to the platform's custodial wallet. Interest accrues daily or weekly and is paid in the same asset or in the platform's native token, depending on the product you choose.

In both cases, your assets join a shared pool used to fund borrowing. You do not lend to a specific borrower. Instead, the protocol manages the pool collectively, setting rates based on overall utilization. The key risk for lenders in DeFi is smart contract vulnerability. In CeFi, the key risk is platform solvency and counterparty risk. Both are real and are discussed in more detail in the risk section of this guide.

Most platforms support a wide range of assets for lending, including major cryptocurrencies like Bitcoin (wrapped as WBTC), Ether (ETH), and Solana (SOL), as well as stablecoins like USDC, USDT, and DAI. Stablecoins typically attract the highest borrow demand and therefore offer the most competitive lending rates, often ranging from 3% to 15% APY depending on conditions.

How Interest Rates Are Set

Interest rates in crypto lending are almost never fixed in the same way a 5-year CD might be. Most DeFi protocols use an algorithmic interest rate model that adjusts rates based on pool utilization, which is the percentage of deposited assets that are currently being borrowed.

At low utilization (say 20%), the borrow rate might be just 1% to 3% annually. As utilization rises toward an optimal target, often set around 80%, the rate increases gradually to attract more deposits and moderate borrowing demand. Above that optimal threshold, rates can spike sharply to 20%, 40%, or even higher to discourage further borrowing and incentivize repayment. This creates a self-regulating system that keeps the protocol liquid.

Aave V3, for example, uses a two-slope rate model: a gradual slope from 0% to the optimal utilization point, and a much steeper slope beyond it. Compound uses a similar approach with its Jump Rate Model. These parameters can be updated through governance votes, giving token holders some control over the protocol's risk posture.

On CeFi platforms, rates are set by the company based on internal demand, competition, and yield opportunities. They are typically less volatile than DeFi rates but also less transparent in how they are derived.

Compound Interest and APY vs APR

When evaluating a lending opportunity, you will encounter two different rate figures: APR (Annual Percentage Rate) and APY (Annual Percentage Yield). Understanding the difference matters more than most people realize.

APR is the simple interest rate without factoring in compounding. APY accounts for the effect of compounding, which means your earned interest itself begins generating interest. On most DeFi protocols, interest compounds continuously or every block, which can significantly increase the effective yield over a year compared to the stated APR.

For example, a 10% APR compounded daily becomes roughly 10.52% APY. At higher rates, the difference is more pronounced: a 30% APR compounded daily becomes approximately 34.97% APY. Always compare APY to APY when evaluating platforms, and look for whether the rate advertised is the base lending rate or includes additional token rewards, as those two components can behave very differently over time.

Some protocols also offer boosted rates through liquidity mining, distributing governance tokens on top of base interest. These additional rewards can dramatically inflate the headline APY but may decrease in value rapidly if the token price falls. Experienced lenders always separate the base yield from token incentives when assessing sustainability.

How Crypto Borrowing Works

Borrowing in crypto is structurally different from a traditional personal loan in one critical way: it is almost always over-collateralized. You must lock up more value than you receive. This sounds counterintuitive at first, but it serves a clear purpose: since crypto prices are volatile and since blockchain transactions cannot rely on credit checks or legal recourse, the collateral model protects lenders and keeps the system solvent.

Collateral Requirements

To borrow on a platform like Aave or MakerDAO, you first deposit an asset as collateral. This collateral is locked in the smart contract for the duration of your loan. You cannot spend it while it is locked, but you retain exposure to its price movements, both the upside and the downside.

Different assets are accepted as collateral at different risk parameters. Blue-chip assets like ETH and WBTC typically have more favorable collateral factors because they are more liquid and less volatile than smaller-cap tokens. On Aave V3, ETH carries a collateral factor of around 80%, meaning you can borrow up to 80 cents for every dollar of ETH you deposit. A more volatile asset like LINK might have a collateral factor of 65% to 70%.

On CeFi platforms, the collateral requirements are set by the company and can change based on market conditions or internal risk models. In some cases, CeFi platforms may also accept a broader range of assets as collateral, including NFTs or real-world assets in more experimental products.

Once your collateral is deposited, you can borrow any supported asset up to your borrowing limit. Most borrowers choose stablecoins, since they can then use the stablecoins freely without worrying about the borrowed asset appreciating and increasing their debt.

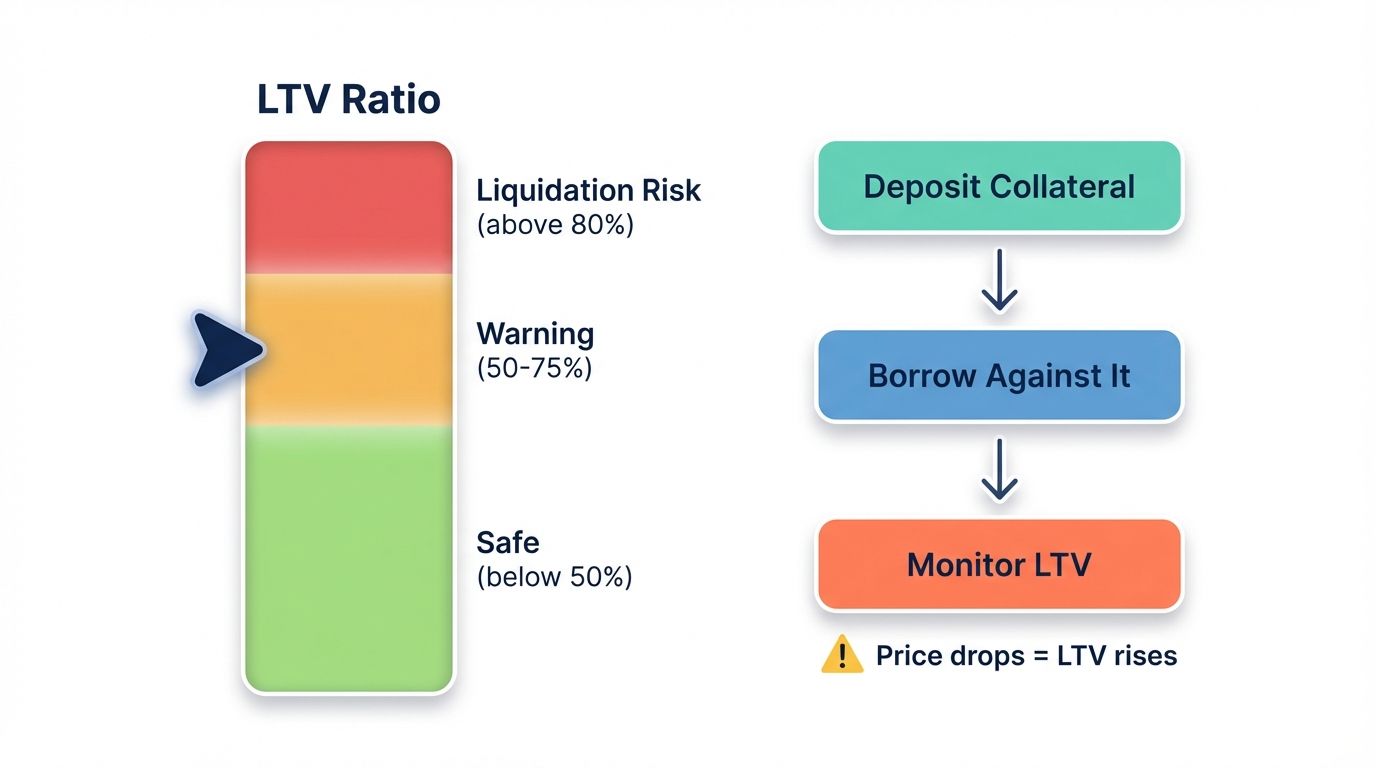

Loan-to-Value (LTV) Ratios Explained

The Loan-to-Value (LTV) ratio is the percentage of your collateral's value that you are currently borrowing. If you deposit 1 ETH worth $3,000 and borrow $1,500 in USDC, your LTV is 50%.

Protocols define two important LTV thresholds. The maximum LTV is the highest ratio at which you can open a new borrow position, typically 65% to 80% for major assets. The liquidation threshold is slightly higher, typically 5% to 10% above the maximum LTV, and represents the point at which your position becomes eligible for liquidation if your collateral value drops.

For example, on Aave V3 with ETH as collateral, you might have a maximum LTV of 80% and a liquidation threshold of 82.5%. This 2.5 percentage point buffer gives you a small cushion but not much in a fast-moving market. Experienced borrowers keep their effective LTV well below the maximum, often at 40% to 60%, to maintain a comfortable safety margin.

Monitoring your LTV in real time is one of the most important habits for any crypto borrower. Most platforms display a health factor, which is a single number summarizing your position's safety. On Aave, a health factor above 1.0 means you are safe; below 1.0, you are eligible for liquidation. Some platforms email or text alerts when your health factor drops below a threshold you set.

Liquidation Risk and How to Avoid It

Liquidation is the process by which a protocol automatically sells part of your collateral to repay your debt when your LTV exceeds the liquidation threshold. It is the most significant risk for borrowers and has caught many participants off guard during sharp market drops.

When liquidation occurs, a third-party liquidator, often a bot, repays part of your debt and receives a portion of your collateral as a bonus, known as the liquidation penalty. On Aave, this penalty is typically 5% to 10% of the liquidated amount. This means you not only lose collateral to repay the debt; you also lose extra collateral as the penalty. In a severe market event, cascading liquidations can cause significant losses beyond what a simple price drop would suggest.

To avoid liquidation, borrow conservatively at well below the maximum LTV. Maintain a buffer of at least 30% to 40% below the liquidation threshold. If the market drops sharply, you have three options: repay part of your loan to reduce LTV, add more collateral to improve your health factor, or accept partial liquidation. Having stablecoins ready to inject as collateral or to repay debt quickly is a practical safety strategy. Some advanced users set automated alerts through on-chain monitoring tools or portfolio trackers to act before the protocol does.

CeFi vs DeFi Lending Platforms

The choice between CeFi and DeFi lending is not just technical; it reflects a fundamental philosophy about trust, custody, transparency, and control. Each approach has distinct advantages and meaningful trade-offs that suit different types of users.

Centralized Lending (CeFi)

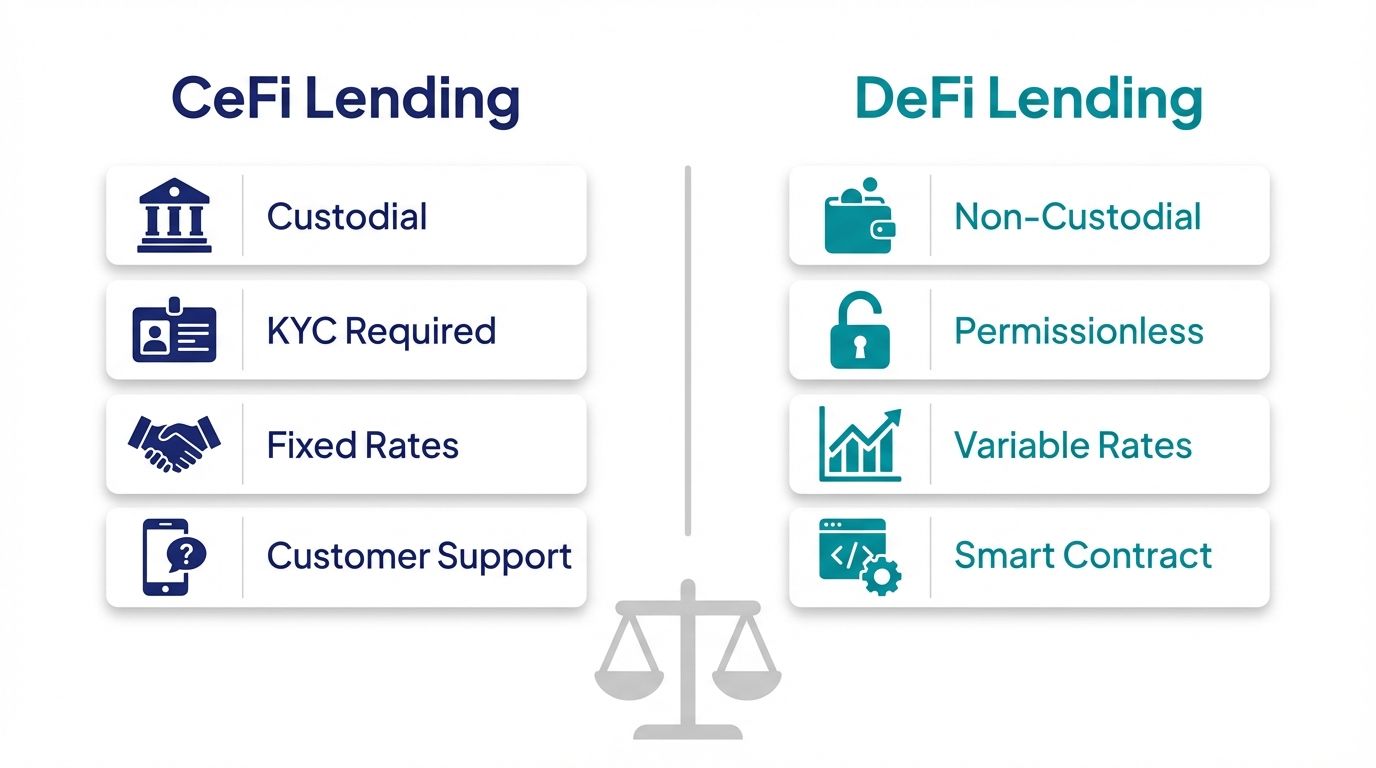

CeFi platforms operate like crypto-native banks or fintech lenders. Companies like Nexo and Ledn (the major survivors post-2022) hold custody of user assets, manage lending operations through internal credit desks, and offer user-friendly interfaces that require no blockchain knowledge.

The main advantages of CeFi are ease of use, customer support, and in some cases, insurance or reserve backing. You can typically access fiat loan disbursements, which is not easily done in pure DeFi. Interest rates are often predictable over short periods. For borrowers, CeFi may offer more flexible terms and manual margin call processes rather than automatic on-chain liquidations.

The main disadvantages became painfully clear during the collapses of Celsius, BlockFi, and Voyager in 2022. When a CeFi platform fails, user funds can become trapped in bankruptcy proceedings. Counterparty risk is real and severe. Regulatory compliance requirements mean CeFi platforms are jurisdictionally restricted and require full KYC, which may be a dealbreaker for privacy-conscious users.

In 2026, the CeFi platforms that survived did so largely by maintaining transparent reserves, passing independent audits, and operating under clearer regulatory frameworks. EU's MiCA regulation and the US SEC's updated digital asset framework have both clarified the compliance requirements for lending platforms, creating a more stable operating environment.

Decentralized Lending (DeFi)

DeFi lending protocols operate entirely through smart contracts on public blockchains. There is no company holding your assets; instead, the protocol holds them, and the code governing the protocol is publicly auditable. Platforms like Aave, Compound, MakerDAO, and Morpho are the leading examples.

The main advantages of DeFi are transparency, self-custody, permissionless access, and composability. You can verify the protocol's rules on-chain at any time. No one can freeze your assets unilaterally (assuming no admin keys). You can stack DeFi protocols together in ways that CeFi simply cannot match. There is no KYC, which means global access regardless of nationality.

The trade-offs are significant: smart contract bugs can lead to catastrophic losses that are not recoverable. Gas fees on Ethereum can make small positions economically unviable. Interfaces are more complex and error-prone for new users. Liquidations are instant and automated, leaving no room for negotiation.

The DeFi lending market in 2026 has also grown more sophisticated. Multi-chain deployments, cross-chain collateral, and real-world asset (RWA) integrations have expanded what is possible, while formal verification of smart contracts and specialized audit firms have improved security track records significantly.

Which Is Right for You?

For beginners and users who prioritize simplicity, regulatory clarity, and the ability to access fiat loans, CeFi remains the more accessible starting point. If you hold significant assets and are not comfortable managing a wallet and monitoring on-chain positions, CeFi platforms offer a familiar product.

For users who value transparency, permissionless access, and the ability to optimize across multiple protocols, DeFi is the more powerful environment. Advanced users running yield strategies or leveraged positions almost universally operate in DeFi because of its composability and the greater control it affords.

Many participants use both. They might keep a portion of their stablecoin holdings on a CeFi platform for simplicity and use DeFi for more complex strategies. The two ecosystems are not mutually exclusive, and a diversified approach across platforms reduces concentration risk.

Top Crypto Lending and Borrowing Platforms in 2026

The lending landscape has consolidated significantly since 2022. The platforms that remain are generally more battle-tested, better audited, and operating with clearer risk parameters than those that came before them. Here is a breakdown of the leading platforms as of March 2026.

Aave (DeFi) remains the largest DeFi lending protocol by TVL, with over $15 billion across its V3 deployments on Ethereum, Arbitrum, Optimism, Polygon, Avalanche, and Base. Aave V3 introduced efficiency mode (E-mode) for correlated assets, isolation mode for newer tokens, and cross-chain portals for liquidity. It supports 30 or more assets across its markets. Lending APY for USDC typically ranges from 3% to 12% depending on utilization. ETH borrowing rates range from 1% to 8%. Aave is widely considered the gold standard for DeFi lending security, having undergone over 20 independent security audits.

Compound V3 (DeFi) has restructured its architecture around single-base-asset markets, with each market having one borrowable asset and multiple accepted collaterals. The redesign simplified the risk model and improved capital efficiency. Compound V3 is live on Ethereum, Arbitrum, Polygon, and Base. USDC is the primary borrowable asset in its largest markets. APY for supplying USDC typically ranges from 2% to 10%. Compound's governance token, COMP, continues to provide additional rewards on certain markets.

MakerDAO / Sky Protocol (DeFi) pioneered the collateralized debt position (CDP) model, allowing users to lock collateral and mint DAI (a decentralized stablecoin) directly, rather than borrowing from a pool. The protocol, which rebranded to Sky in 2024, supports ETH, WBTC, staked ETH variants, and various RWAs as collateral. The stability fee (interest rate) on ETH vaults has historically ranged from 0.5% to 8%. MakerDAO's DAI retains its place as one of the most widely used decentralized stablecoins, and its integration into other protocols gives it unique composability.

Morpho (DeFi) is one of the most significant newer entrants, having grown from a peer-to-peer optimizer layered on Aave and Compound to a standalone modular lending protocol with Morpho Blue. Its architecture allows anyone to create permissionless lending markets with custom parameters, while MetaMorpho vaults allow passive depositors to earn optimized yields without managing positions manually. TVL surpassed $3 billion in late 2025. Morpho's rates are often more competitive than Aave and Compound for certain assets because of its more efficient matching mechanism.

Nexo (CeFi) is one of the few major CeFi lending platforms to have navigated the 2022 collapse without halting withdrawals. It offers crypto-backed loans with LTV ratios from 20% to 50%, flexible or fixed terms, and the ability to receive loan proceeds in fiat or stablecoins. Nexo supports over 65 assets as collateral. Interest rates for borrowing range from 6.9% to 13.9% annually depending on NEXO token holdings and the selected tier. It operates under MiCA licensing in the EU and has received SOC 2 Type II certification for security practices.

Ledn (CeFi) is a Canada-based platform focusing specifically on Bitcoin-backed loans and Bitcoin savings accounts. Its Open Book attestation model provides monthly proof-of-reserves, which differentiates it from less transparent CeFi competitors. BTC-backed loan rates typically sit around 10% to 14% annually with 50% LTV. Ledn is a strong option for Bitcoin maximalists who want liquidity against their BTC without selling and prefer a CeFi wrapper for simplicity.

Crypto Lending Strategies for Passive Income

Lending your crypto assets is one of the most accessible ways to generate passive income in the digital asset space. Unlike trading, lending does not require active market monitoring. However, choosing the right strategy for your risk tolerance and asset mix matters significantly.

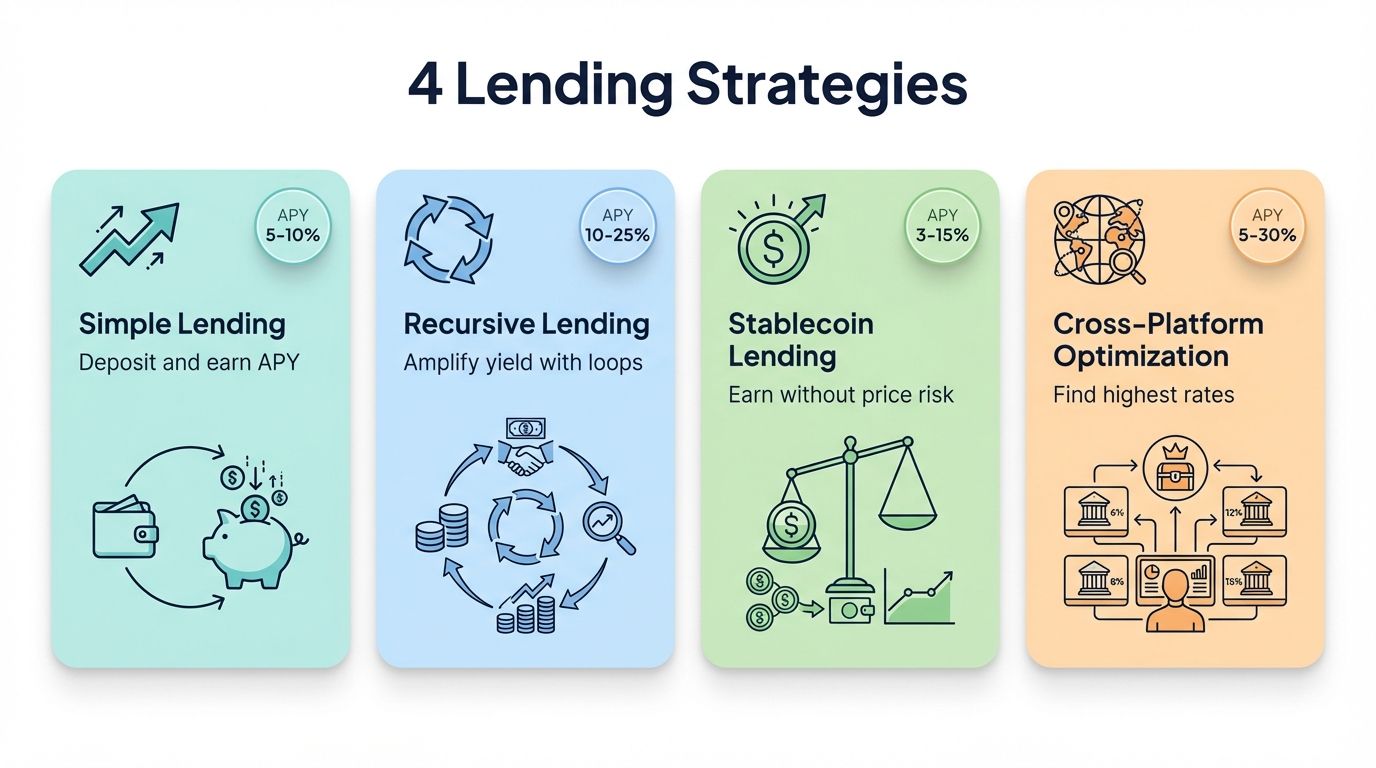

Simple Lending for Yield

The most straightforward strategy is depositing assets directly into a lending protocol and collecting interest. This is suitable for long-term holders who already intend to keep their assets regardless of price movements. The opportunity cost of holding idle assets is zero yield; depositing them into a lending pool converts that dead weight into ongoing income.

For conservative lenders, stablecoins and ETH on established protocols like Aave or Compound are the safest starting points. ETH lending rates on Aave currently range from 2% to 5% APY in base interest, with additional AAVE token rewards available on some markets. This modest yield may seem unremarkable, but it compounds meaningfully over a multi-year holding period.

The key principle for simple lending is protocol selection: stick to protocols with long track records, multiple independent audits, and high TVL that signals market confidence. Chasing the highest APY on newly launched protocols carries substantially more risk than a slightly lower yield on a battle-tested platform.

Recursive Lending (Looping)

Recursive lending, also known as looping or leveraged yield, involves depositing an asset, borrowing against it, depositing the borrowed asset again, and repeating this cycle several times. The result is amplified exposure to the lending rate and any token rewards, but also amplified liquidation risk.

For example, you deposit 1 ETH, borrow 0.7 ETH worth of stETH (liquid staked ETH), deposit that stETH, borrow again, and continue. Each loop amplifies your staking yield but increases your LTV and shrinks your liquidation buffer. This strategy is most commonly executed with correlated assets (ETH and stETH, for instance) to minimize the risk that the borrowed and deposited assets move dramatically against each other.

Aave's E-mode feature was specifically designed to make recursive lending with correlated assets more capital-efficient, allowing higher LTV ratios (up to 90%) between assets in the same category. Tools like DeFi Saver can automate the loop creation and monitor health factors to prevent liquidation.

Recursive lending is an intermediate-to-advanced strategy. It is not recommended without a solid understanding of health factors, liquidation mechanics, and the specific behavior of the assets involved.

Stablecoin Lending for Stable Returns

For risk-averse participants, lending stablecoins offers yield without exposure to crypto price volatility. Since the lent asset maintains a roughly constant value, the only risks are smart contract risk and the stablecoin's own peg stability.

USDC lending on Aave V3 (Ethereum) has offered between 4% and 14% APY over the past 12 months, with peaks during periods of high DeFi activity and borrow demand. On Morpho's curated vaults, USDC yields have consistently been 1% to 3% higher than Aave base rates due to more efficient capital deployment.

Stablecoin lenders benefit from a relatively predictable income stream and are not subject to the emotional volatility of holding directional crypto assets. Many DeFi-native investors maintain a portion of their portfolio in stablecoin lending positions as a low-correlation yield component alongside their spot holdings.

Cross-Platform Yield Optimization

Lending rates across platforms are not uniform and change constantly. An active yield optimizer moves assets between platforms to capture the highest available rate at any given time. This can be done manually or through yield aggregators like Yearn Finance, which automatically reallocates capital to higher-yielding strategies.

The challenge of cross-platform optimization is gas costs and monitoring overhead. Moving assets between protocols on Ethereum mainnet can cost $5 to $50 per transaction, which erodes returns on smaller positions. On Layer 2 networks like Arbitrum or Base, transaction costs are typically under $0.10, making active optimization far more viable for smaller capital amounts.

Using a portfolio tracker that aggregates your positions across multiple protocols allows you to see your effective blended yield at a glance, compare it to available rates elsewhere, and make informed rebalancing decisions without logging into each platform individually.

Crypto Borrowing Strategies

Borrowing against your crypto assets unlocks a range of powerful financial strategies that go far beyond simply accessing liquidity. Understanding why and how to borrow strategically separates sophisticated participants from those who merely use borrowing as a last resort.

Borrowing Against Bitcoin Without Selling

One of the most popular borrowing use cases is using Bitcoin as collateral to access dollars or stablecoins without triggering a taxable sale. Long-term Bitcoin holders who need liquidity for personal expenses, investments, or business purposes can borrow against their BTC and repay the loan when convenient, preserving their BTC position throughout.

On Ledn, for example, a Bitcoin holder can deposit 1 BTC (currently worth approximately $85,000 in March 2026) and receive up to $42,500 in USDC or USD at 50% LTV. The loan carries an interest rate of around 10% to 12% annually. If BTC appreciates over the loan period, the borrower benefits from that appreciation while having had access to capital the entire time. If BTC drops sharply, the borrower risks liquidation unless they add more collateral or repay the loan.

This strategy is particularly compelling for long-term holders with low cost basis who face large capital gains tax on any sale. The tax treatment of crypto loans (as non-taxable events in most jurisdictions) makes this a powerful alternative to selling.

Leveraged Long Positions

Borrowing can be used to amplify exposure to an asset you are already bullish on. The mechanism is simple: deposit ETH as collateral, borrow USDC, use the USDC to buy more ETH, and repeat. This creates a leveraged long position on ETH. Your profits are amplified when ETH rises, but your losses are also amplified when it falls, and you face liquidation risk if it falls enough.

This strategy is sometimes called delta-amplified exposure and is popular during bull markets. The key risk management principle is to maintain enough buffer that even a 30% to 40% price drop does not push your LTV to the liquidation threshold. At 2x leverage, a 30% drop in collateral value translates to a 60% move toward liquidation, depending on your initial LTV.

Sophisticated traders use this strategy in conjunction with stop-loss alerts and automated health factor monitoring to deleverage before liquidation rather than after. The goal is to benefit from the leverage in favorable conditions and exit gracefully in adverse ones.

Tax-Efficient Liquidity Access

In most jurisdictions as of 2026, borrowing against crypto assets is not a taxable event. You receive capital without triggering a capital gains recognition. This makes borrowing an attractive mechanism for accessing liquidity from appreciated positions without incurring an immediate tax liability.

The strategy works best when the cost of borrowing (interest rate) is lower than the expected appreciation of the collateral asset. If you borrow at 8% APR and your collateral appreciates at 20% per year, you are net positive on both the capital gain and the yield side. This is not guaranteed, of course, and assumes you can manage the borrowing cost and liquidation risk effectively.

Tax laws vary by jurisdiction and are evolving rapidly. Users should consult a qualified tax professional familiar with digital asset taxation in their country before relying on borrowing as a tax strategy. The general principle holds in the US, UK, EU, and many Asian markets, but specific rules around loan forgiveness, liquidation events, and collateral disposal can create unexpected tax consequences.

Funding DeFi Opportunities

Borrowers sometimes use their crypto-backed loans to fund participation in other DeFi protocols. For example, a borrower might take a USDC loan against ETH and deploy that USDC into a high-yield liquidity pool, a newly launched protocol with incentives, or a yield aggregator. If the yield from the deployed capital exceeds the borrowing cost, the net result is positive carry.

This strategy, often called carry trading in traditional finance, requires careful management. The risk is that the yield opportunity underperforms expectations, token rewards lose value, or the underlying protocol suffers a security exploit. The safest version of this strategy deploys borrowed stablecoins into other established stablecoin yield opportunities where the rate differential is predictable and the underlying smart contracts are well-audited.

Key Risks of Crypto Lending and Borrowing

Crypto lending and borrowing carries meaningful risks that differ substantially from traditional savings and lending products. Understanding these risks in depth is a prerequisite for participating responsibly. No yield in crypto comes without corresponding risk, and the history of the sector is filled with painful lessons for those who ignored this principle.

Smart Contract Risk

In DeFi, your assets are held by code. Smart contracts can contain bugs, logical errors, or vulnerabilities that allow attackers to drain funds in minutes. This is not a theoretical risk: the DeFi space has suffered hundreds of exploits since 2020, with losses totaling several billion dollars. Even audited protocols have been exploited, sometimes through complex multi-step attack vectors that auditors missed.

Mitigation strategies include using protocols with multiple independent audits and a track record of operating without exploits for several years, diversifying across protocols so no single exploit can wipe out your entire position, and using protocols that have bug bounty programs and proven incident response mechanisms.

Liquidation Risk

As detailed earlier, borrowers face automatic liquidation when their collateral value falls below the required threshold. Liquidations happen instantly on-chain and cannot be appealed. In volatile markets, flash crashes can trigger liquidations even for positions that were well within safe parameters hours before.

The practical mitigation is to borrow conservatively, maintain a 30% to 40% buffer below the liquidation threshold, monitor your health factor actively, and have capital ready to inject as collateral or repay debt on short notice. Using a platform with real-time alerts is important for anyone running leveraged positions.

Platform and Counterparty Risk

CeFi platforms carry the risk of insolvency, mismanagement, fraud, or regulatory shutdown. The 2022 collapses demonstrated that even large, seemingly well-capitalized platforms could become insolvent rapidly due to poor risk management and opaque operations. CeFi users should check proof-of-reserves reports, avoid concentrating large amounts in a single platform, and stay informed about the platform's financial health and regulatory standing.

Even in DeFi, governance risk is real. Protocol upgrades, parameter changes, or rogue governance proposals can alter the terms of your position. Governance exploits, where an attacker acquires enough voting power to pass malicious proposals, have occurred in smaller protocols. Favoring protocols with robust governance safeguards reduces this exposure.

Interest Rate Volatility

DeFi interest rates are not fixed. A stablecoin position earning 8% today might earn 2% tomorrow if borrowing demand drops. More significantly, a borrower locked into a variable rate might see their borrowing cost spike from 5% to 40% during periods of high demand, substantially increasing the cost of carrying a loan and potentially making it economically unviable.

Borrowers should account for interest rate volatility when planning a borrowing strategy. Some protocols, including Aave's new rate switch feature introduced in V3.1, allow borrowers to toggle between variable and stable rates, providing some protection against rate spikes in exchange for a slight premium. Monitoring rate trends and refinancing between protocols when rates diverge is another management tactic.

Regulatory Risk

The regulatory landscape for crypto lending has shifted dramatically over the past three years. In the US, the SEC and CFTC have both asserted jurisdiction over various types of crypto lending products. Several CeFi platforms have received cease-and-desist orders or enforcement actions for offering unregistered securities. In the EU, MiCA has created a clearer but more restrictive framework for licensed operators.

Participants in crypto lending, especially through CeFi channels, should be aware that platforms operating in their jurisdiction may be required to comply with new rules that affect withdrawals, interest payments, or eligibility. DeFi protocols, being non-custodial and permissionless, present different regulatory risk: they are less likely to be shut down but may become legally gray for users in certain jurisdictions over time.

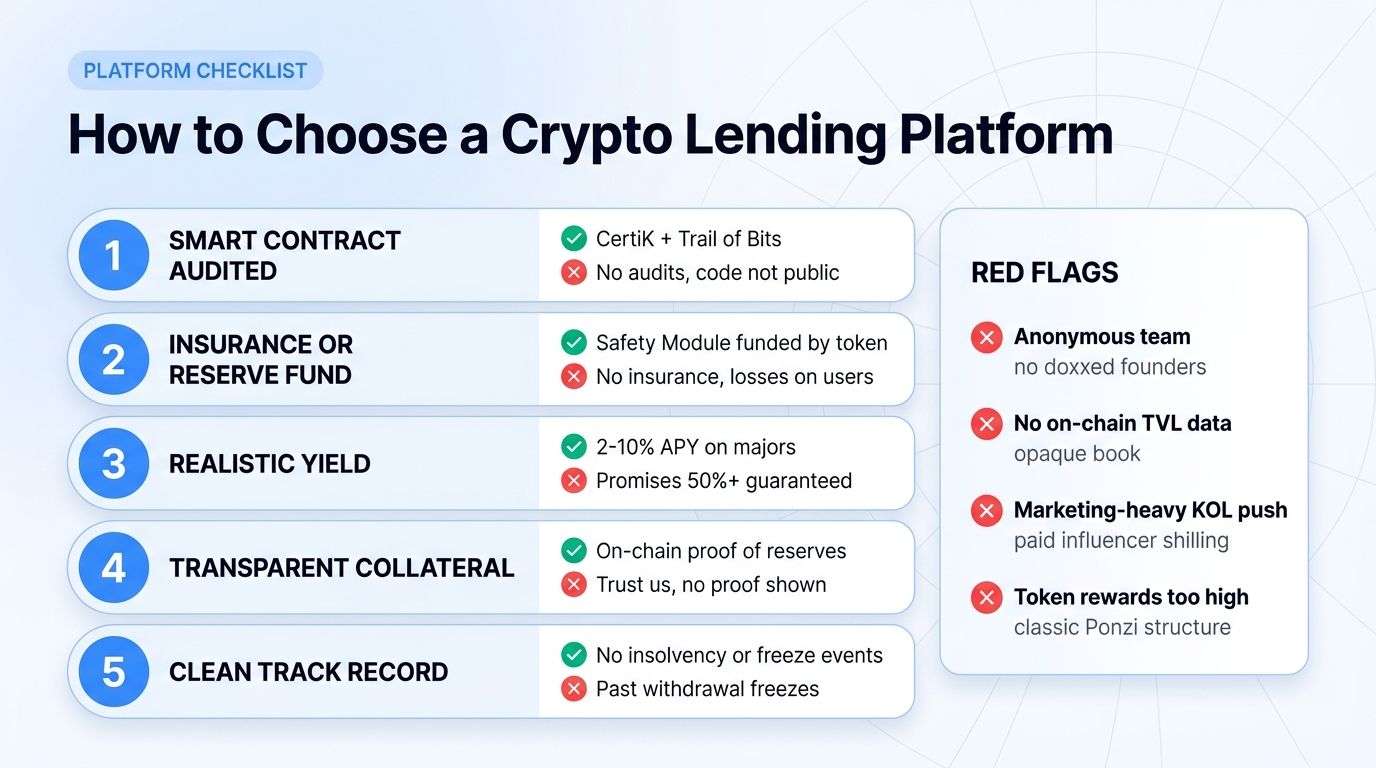

How to Choose the Right Crypto Lending Platform

With dozens of platforms competing for deposits and borrowing activity, making an informed choice requires evaluating several dimensions simultaneously. The right platform depends heavily on your goals, risk tolerance, and technical comfort level.

Security and Audit History: Prioritize platforms with multiple independent security audits from respected firms like Trail of Bits, OpenZeppelin, Certora, or Spearbit. For DeFi protocols, check the number and recency of audits on the protocol's documentation or on platforms like DeFiSafety. For CeFi, look for SOC 2 certification and proof-of-reserves attestations.

Track Record: How long has the platform been operating without a major exploit or insolvency event? A protocol that has managed over $1 billion in TVL for three or more years without incident provides stronger evidence of resilience than a newer, higher-yield alternative.

Supported Assets: Make sure the platform supports the assets you want to lend or the collateral you plan to use for borrowing. Also check whether there are supply caps or borrow caps that might limit your position size or affect the rates you receive.

APY and Rate Transparency: Compare the base lending APY separately from any token incentives. Understand how rates are calculated and how frequently they change. Avoid platforms that advertise suspiciously high fixed rates without clear disclosure of how those rates are funded.

LTV Ratios and Liquidation Mechanics: For borrowers, understand the maximum LTV, the liquidation threshold, and the liquidation penalty. Platforms with lower liquidation penalties and partial liquidation (rather than full position liquidation) are more forgiving in adverse conditions. Aave and Compound both use partial liquidation, closing just enough of the position to restore the health factor, rather than liquidating the entire collateral at once.

User Interface and Monitoring Tools: A clean, intuitive interface reduces the risk of costly errors. Look for platforms that display your health factor prominently, provide clear transaction confirmations, and offer built-in alerts or integrations with monitoring tools. For CeFi, assess the quality of the mobile app, customer support response times, and withdrawal processing speed.

Jurisdiction and Regulatory Compliance: Confirm that the platform is legally accessible in your country. CeFi platforms operating under MiCA in the EU or registered with FinCEN in the US provide a degree of regulatory accountability. Understand what protections (if any) apply to your deposits in the event of platform failure.

Fee Structure: On DeFi platforms, the primary costs are gas fees and any protocol fees on withdrawals or swaps. On CeFi, look for origination fees, early repayment penalties, or withdrawal fees that are not prominently disclosed in the headline rate. The all-in cost of a lending or borrowing position is what matters, not the advertised rate alone.

Managing Your Crypto Lending Portfolio Across Platforms

Once you are active across multiple lending and borrowing platforms, the complexity of managing your positions grows quickly. Each protocol has its own interface, its own health factor metric, its own notification system, and its own rate dynamics. Without a centralized view, it is easy to miss a deteriorating health factor on one platform while you are monitoring another, or to fail to notice that a lending rate you were counting on has dropped significantly.

This is where a unified portfolio dashboard becomes not just convenient but practically essential. You need to see your aggregate collateral value, total borrow exposure, blended effective yield, and overall health factor across all protocols and exchanges from a single interface. Manually logging into Aave, Compound, Morpho, and a CeFi platform separately introduces delays and errors that can be costly in fast-moving market conditions.

Monitoring LTV ratios across all positions in real time is particularly critical for borrowers. A portfolio dashboard that pulls data from multiple protocols and displays a consolidated view of your total collateral versus total debt lets you see at a glance how close any position is to the liquidation threshold, regardless of which platform it is on. Setting alerts at specific health factor thresholds, say a warning at 1.5 and a critical alert at 1.2, gives you time to act before liquidation becomes imminent.

Beyond risk management, a unified dashboard enables yield optimization. Seeing that your USDC is earning 4.2% on Compound while the same asset earns 6.8% on Morpho creates an actionable rebalancing opportunity. Without the side-by-side comparison, that rate differential might go unnoticed for weeks.

Altrady offers exactly this kind of cross-platform monitoring capability. Designed for active crypto participants, Altrady's portfolio tracking tools aggregate your positions across multiple exchanges and DeFi protocols, giving you a consolidated view of your assets, yields, and exposure. For anyone managing a meaningful lending or borrowing portfolio, having that single pane of glass can make the difference between proactive risk management and reactive damage control. You can explore all of these features with a free trial, with no commitment required, and see firsthand how much easier active portfolio management becomes when your data lives in one place.

Frequently Asked Questions

What is the safest crypto lending platform?

Safety in crypto lending depends on the type of platform and how you define risk. For DeFi, Aave is widely considered the safest option based on its long operational history (live since 2020), extensive audit coverage, and high TVL demonstrating market trust. It has never suffered a protocol-level exploit. For CeFi, Nexo and Ledn are among the more transparent and regulated options available as of 2026, both publishing proof-of-reserves and operating under formal regulatory frameworks. No platform is entirely risk-free. Diversifying your lending positions across multiple established protocols is the most practical approach to minimizing the impact of any single point of failure.

Can I lose my crypto through lending?

Yes, it is possible to lose funds through lending, though the mechanisms differ by platform type. In DeFi, the primary risk is a smart contract exploit or bug that drains the lending pool. If such an event occurs, deposited funds may be partially or fully unrecoverable. In CeFi, funds can be lost if the platform becomes insolvent and enters bankruptcy, as happened with Celsius and BlockFi users in 2022. On top of these platform-specific risks, stablecoin lenders face depeg risk if the stablecoin they are holding loses its dollar peg. None of these are likely in normal conditions on established platforms, but they are real possibilities and should inform both your platform selection and your position sizing.

What collateral do I need to borrow crypto?

The accepted collateral types vary by platform. On Aave V3, you can use ETH, WBTC, various liquid staked ETH tokens (wstETH, rETH), USDC, and other supported assets. Each asset has its own collateral factor (how much you can borrow against it) and risk parameters. On MakerDAO, ETH, WBTC, and real-world assets are accepted. On CeFi platforms, accepted collateral typically includes BTC, ETH, and major stablecoins, with some platforms also accepting altcoins at higher haircuts. In all cases, you must deposit more value as collateral than you receive as a loan (over-collateralization). The exact ratio depends on the asset and the platform's risk parameters, but a typical minimum LTV ranges from 50% to 80% of your collateral value.

What happens if my collateral gets liquidated?

If your loan's LTV exceeds the liquidation threshold, your position becomes eligible for liquidation. A liquidator (typically an automated bot) repays part of your debt using your collateral and receives a bonus, the liquidation penalty, which ranges from 5% to 15% depending on the protocol and asset. On most major DeFi protocols like Aave, liquidation is partial: only enough collateral is sold to bring your health factor back above 1.0, not your entire position. After liquidation, you still owe the remaining debt but now have less collateral. If the market continues to fall, you may face further liquidations. The practical consequence is that you lose a portion of your collateral to penalties on top of the debt repaid, making liquidation a net-negative event you want to avoid through proactive position management and conservative borrowing.

Is crypto lending taxable?

Tax treatment of crypto lending varies significantly by jurisdiction and should be verified with a qualified professional. In the United States, interest earned from lending crypto is generally treated as ordinary income in the year it is received, taxable at your marginal income tax rate. Borrowing against crypto is generally not a taxable event, though if your collateral is liquidated, that liquidation may trigger a capital gains event on the collateral. In the EU under current guidance, lending income is similarly treated as ordinary income in most member states, though reporting requirements vary. In Australia, lending interest is also treated as assessable income. The one relatively consistent rule across jurisdictions is that taking out a loan itself does not trigger a tax liability, making crypto-backed borrowing a tax-efficient way to access liquidity from appreciated holdings. Given the rapidly changing regulatory landscape, always consult a tax advisor familiar with digital assets in your specific country before making decisions based on tax considerations.

2026 Update: What to Check Before You Act

Crypto lending is most useful when the borrower understands collateral rules, liquidation mechanics, and the difference between protocol yield and counterparty risk.

| Check | What to review | Why it matters |

|---|---|---|

| Collateral ratio | Track loan-to-value, liquidation threshold, and maintenance margin. | Small price moves can trigger liquidation when collateral buffers are too thin. |

| Platform model | Separate DeFi protocol risk from centralized lender or exchange counterparty risk. | The failure mode is different depending on who controls assets. |

| Yield source | Identify whether yield comes from borrowers, incentives, market making, or token emissions. | High yield is not automatically sustainable or low risk. |

Quick trader checklist

- Stress-test collateral against a sharp market drawdown.

- Avoid borrowing against volatile collateral without alerts.

- Review withdrawal limits, audits, and incident history before depositing size.

FAQ

What is the main risk in crypto borrowing?

The main risk is forced liquidation when collateral value falls or loan terms change. Platform failure, smart contract bugs, and withdrawal limits are also important risks.