On April 10, 2026, the Hong Kong Monetary Authority (HKMA) awarded the first stablecoin issuer licenses under the city's new regulatory regime. HSBC received approval for an HSBC-issued Hong Kong dollar stablecoin. Anchorpoint (a consortium between Standard Chartered and Animoca Brands) received approval for a separate HKD-backed stablecoin. The two licenses positioned Hong Kong as the first major Asian financial center with operating regulated stablecoin issuers.

The licensing event matters for three reasons. First, it confirms a regulatory framework that Asia's other financial centers will likely emulate. Second, it puts major traditional banks (HSBC, Standard Chartered) directly in the stablecoin business at scale. Third, it diversifies the global stablecoin landscape away from US dollar dominance.

This guide explains what the Hong Kong stablecoin framework requires, the strategic positioning of HSBC and Anchorpoint, the impact on Asian crypto markets, and what the implications are for the broader stablecoin category.

Key Licensing Facts Traders Should Check First

For traders, the important question is not only who received a license, but what each license means for liquidity, settlement, and counterparty risk. The table below summarizes the practical checks before treating any HKD stablecoin as tradeable collateral or a settlement asset.

| Item | What changed | Why traders should care |

|---|---|---|

| Regulator | The Hong Kong Monetary Authority (HKMA) supervises licensed fiat-referenced stablecoin issuers. | Regulated issuance reduces some reserve and redemption uncertainty, but it does not remove market, liquidity, or exchange-listing risk. |

| Issuer profile | HSBC focuses on bank-led payment and treasury use cases; Anchorpoint combines Standard Chartered's banking infrastructure with Animoca's Web3 network. | The two issuers may serve different venues and customer types, so liquidity will not necessarily appear in the same trading pairs. |

| Reserve and redemption checks | Stablecoin users should look for reserve disclosures, redemption terms, audit or attestation cadence, and clear issuer contact points. | A licensed token can still trade at a discount during stress if redemption access, exchange liquidity, or market confidence weakens. |

| Token verification | Before depositing or trading, confirm the official issuer name, ticker, chain, and contract address through the issuer or exchange. | New regulated brands attract copycat tokens, fake listings, and phishing campaigns soon after launch. |

What the Hong Kong Stablecoin Licensing Regime Requires

The HKMA's stablecoin regime was finalized in 2025 and the first applications were processed in early 2026. The framework has several key components.

First, full reserve backing. Issuers must hold reserves equivalent to 100% of the outstanding stablecoin supply. Reserves must consist of high-quality liquid assets (cash, short-term government bonds, qualifying money market funds).

Second, redemption rights. Holders have the right to redeem stablecoin tokens for the underlying fiat currency at par value, subject to standard verification procedures. Redemption must be processed within reasonable timeframes (typically same-day or next-day).

Third, separation of reserves. The reserve assets must be held in custodial accounts separate from the issuer's other corporate assets. In the event of issuer insolvency, holders have priority claims on the reserve assets.

Fourth, ongoing reporting. Issuers must publish daily attestations of reserves and quarterly third-party audits. The HKMA conducts regular supervisory reviews.

Fifth, AML and KYC requirements. Issuers must implement transaction monitoring, sanctions screening, and customer identification for direct redemption customers.

Sixth, technical and operational standards. Smart contracts must meet security requirements. Operational continuity, cybersecurity, and incident response procedures are reviewed.

The regime resembles in spirit the US frameworks emerging under the CLARITY Act and the EU MiCA framework, but with Hong Kong-specific implementation details.

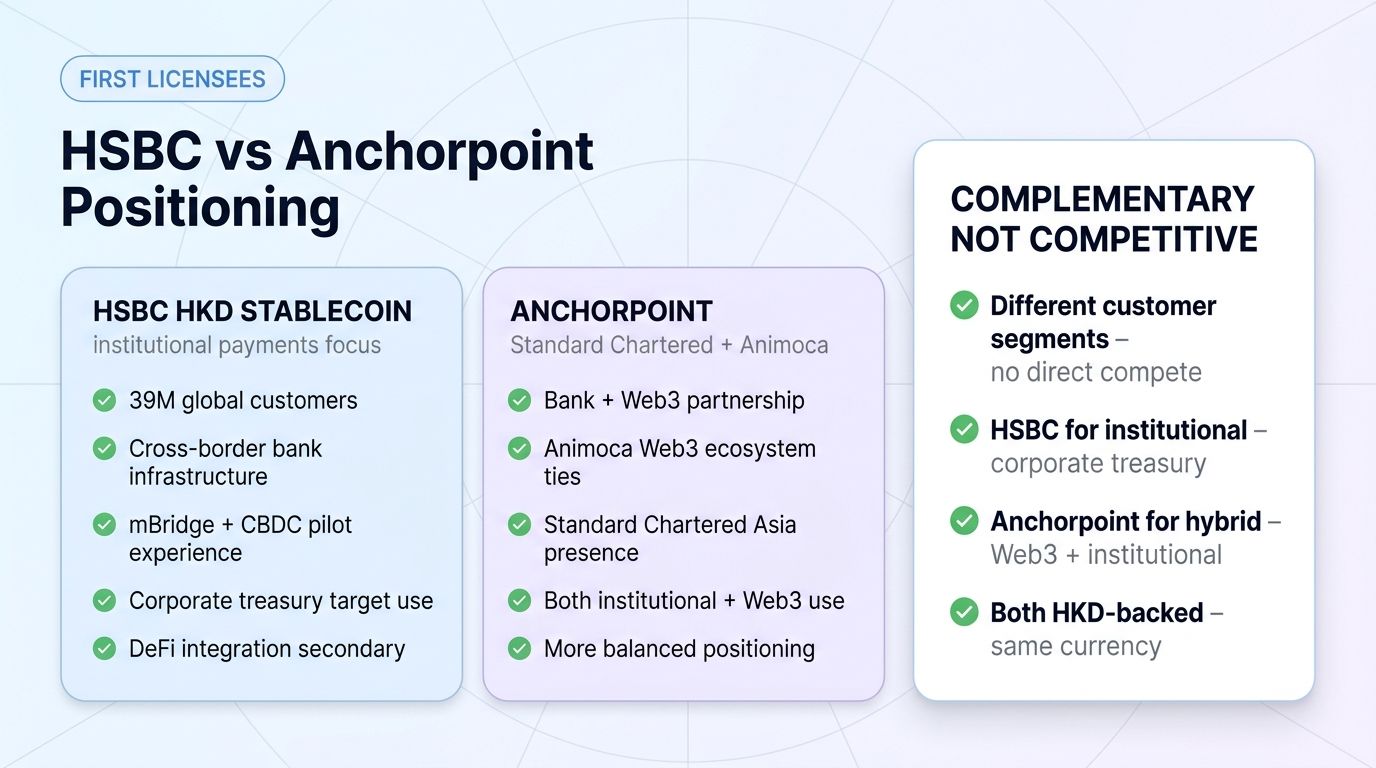

HSBC's Hong Kong Dollar Stablecoin

HSBC's stablecoin is positioned as a payments and corporate treasury product. The bank's strategic intent is to provide a regulated digital HKD instrument for institutional clients (corporate treasuries, fund managers, settlement infrastructure).

Three structural advantages position HSBC well.

First, HSBC has approximately 39 million customers globally with deep penetration in Hong Kong's banking sector. This existing customer base provides a natural distribution channel for the stablecoin.

Second, HSBC has been investing in blockchain and digital currency infrastructure for several years. The bank has participated in major central bank digital currency pilots (mBridge, Project Dunbar) and has internal digital asset capabilities.

Third, HSBC is uniquely positioned for cross-border use cases. As a global bank with operations across major Asian markets (Hong Kong, Singapore, mainland China access), HSBC can facilitate HKD stablecoin use across regional corridors.

The token initially supports payment and settlement use cases. DeFi integration is expected but secondary to the institutional-payments focus.

Anchorpoint and the Standard Chartered + Animoca Partnership

Anchorpoint's stablecoin reflects a different strategic positioning. The consortium combines Standard Chartered (a major global bank with strong Asian presence) and Animoca Brands (a leading Hong Kong-based crypto and Web3 company).

The combination is unusual but logical.

Standard Chartered provides the banking, custody, and compliance infrastructure. The bank has been increasingly active in crypto, including investments in major crypto firms and pilot programs across multiple jurisdictions.

Animoca brings the Web3 expertise and ecosystem connections. The company has investments in dozens of major crypto and gaming projects, providing natural integration paths for the Anchorpoint stablecoin into Web3 use cases.

The combined positioning suggests Anchorpoint will pursue both institutional and Web3-native use cases more equally than HSBC's payments-focused stablecoin. The two banks are not competing for identical customer segments.

Why Hong Kong's Move Matters for Asia

Three structural impacts.

First, regulatory precedent. Hong Kong's framework provides a working model that other Asian financial centers (Singapore, Tokyo, Seoul, Dubai) can study and adapt. Regulatory diffusion may accelerate.

Second, USD stablecoin diversification. The vast majority of existing stablecoin liquidity is denominated in US dollars. HKD stablecoins, if successful, represent the start of non-USD regulated stablecoin issuance. This may eventually reduce the dollar-centric concentration of crypto markets.

Third, traditional finance acceleration. With HSBC and Standard Chartered now operating crypto stablecoins, peer banks in Asia will face strategic pressure to follow. DBS in Singapore, MUFG in Japan, and other major regional banks are likely watching closely.

For traders, the implications are mixed. The new stablecoins are unlikely to materially affect USD stablecoin trading liquidity in the near term. However, they may catalyze new use cases (regional payment flows, RWA-style products denominated in non-USD currencies) that grow the broader crypto-finance market.

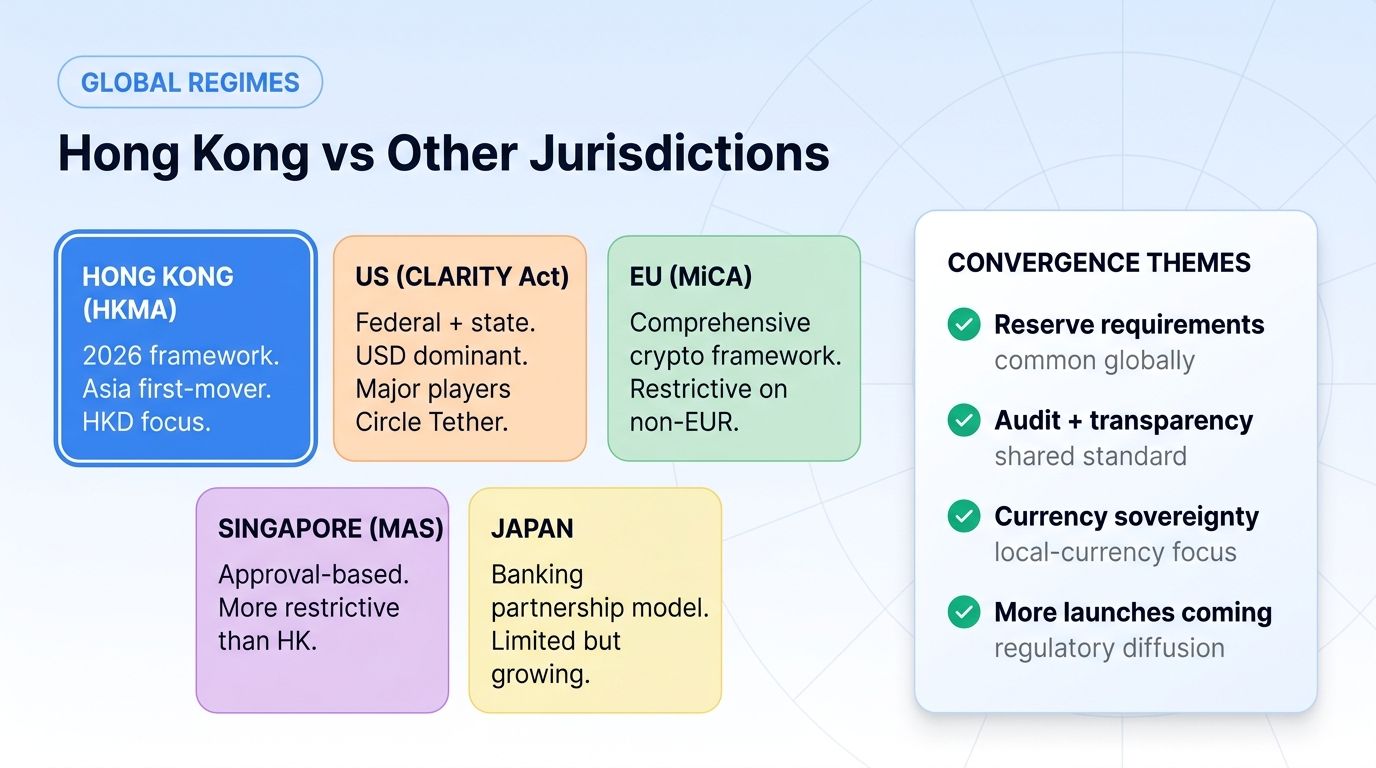

Comparison to Other Stablecoin Regimes

Multiple jurisdictions now have working stablecoin regulatory frameworks.

United States (CLARITY Act 2026): Federal framework for payment stablecoins with state-level variations. Major dollar stablecoin issuers (Circle, Tether for international) are increasingly compliant. The framework emphasizes reserve quality, audit requirements, and consumer protections.

European Union (MiCA, 2024 implementation): Comprehensive crypto framework that includes stablecoin requirements. Notable for restrictive limits on non-EUR stablecoin transactions in certain contexts. The framework has been controversial but operational.

Hong Kong (HKMA framework, 2026): Newer framework with similar reserve and audit requirements. Smaller scale than US/EU but strategically positioned for Asia.

Singapore (MAS framework): Stablecoin issuance subject to specific regulatory approvals. More restrictive than Hong Kong in scope but operational.

Japan: Stablecoin issuance approved through specific banking partnerships. Limited but growing.

The frameworks differ in details but share common themes: reserve backing requirements, audit transparency, redemption rights, and AML compliance. The next 12-24 months will likely produce additional jurisdiction frameworks as regulators globally converge on similar standards.

How Traders Should Think About Asian Stablecoins

For traders primarily active in crypto markets, the practical impact is modest in the near term.

First, USD stablecoins remain dominant for active trading. USDT and USDC liquidity is too deep to be displaced by HKD stablecoins in trading pair contexts.

Second, regional and corridor-specific use cases may benefit from HKD stablecoins. Traders running cross-border payment or arbitrage strategies between Hong Kong and US/European venues may find HKD stablecoins useful for settlement.

Third, the broader theme is positive for crypto infrastructure. More regulated stablecoin issuers create more institutional participation in crypto, which supports broader market growth.

Fourth, the announcement may catalyze related positions. Crypto-adjacent banks (with significant institutional crypto operations) may benefit. Companies like Standard Chartered, HSBC, DBS, and others have explicit crypto strategies. Their performance is partly tied to crypto adoption.

What the Hong Kong Stablecoin Race Tells Us About 2026

Three observations.

Observation 1: Traditional banks are now real stablecoin players. The era of crypto-native dominance (USDT, USDC) is being challenged by regulated traditional finance entries. HSBC and Standard Chartered are joined by PayPal (PYUSD), Western Union (USDPT), and likely more upcoming launches.

Observation 2: Regulatory clarity creates competitive launches. Where regulatory frameworks exist, major institutions launch products. The pattern is repeating across the US, EU, Hong Kong, and emerging frameworks.

Observation 3: Asia is positioning for crypto leadership. Hong Kong, Singapore, and other Asian financial centers have invested significantly in regulatory infrastructure. The result is increasingly Asian-anchored crypto activity that competes with US and European venues.

The Risks of Asia Stablecoin Investing

Several risks apply.

Adoption uncertainty. HKD stablecoins are new products with no operational history. Whether they achieve meaningful adoption beyond initial institutional pilots remains to be seen.

Liquidity risk. Initial trading liquidity is modest. Active traders may face slippage in non-trivial size.

Regulatory risk. Stablecoin regulation continues to evolve. The current HKMA framework may be amended over time as the market develops.

Competitive risk. Hong Kong's framework may be copied or improved upon by other jurisdictions. The first-mover advantage may be smaller than expected if Singapore, Dubai, or other centers launch competing regimes.

Geopolitical risk. Hong Kong's relationship with mainland China and the US creates complex regulatory dynamics that could affect the local crypto ecosystem.

Trader Checklist Before Using HKD Stablecoins

Before using any Hong Kong dollar stablecoin in a trading workflow, run a short checklist instead of assuming that a bank brand automatically removes risk.

- Check the official source first. Confirm that the issuer, ticker, chain, and contract address match the HKMA register, issuer announcement, or exchange listing page.

- Watch liquidity depth. A stablecoin can be fully backed and still be hard to enter or exit if exchange order books are thin.

- Separate payment use from trading use. HSBC's product may initially be more useful for treasury and settlement flows, while Anchorpoint may reach Web3 venues faster.

- Track redemption terms. The practical value of a stablecoin depends on whether users can redeem quickly, at par, and through clear procedures.

- Keep risk tools active. Use position sizing, portfolio tracking, alerts, and automated exit rules when experimenting with new stablecoin pairs or collateral markets.

For Altrady users, the practical workflow is to monitor exchange listings, add supported HKD stablecoin markets to watchlists, and track the effect on portfolio exposure before deploying larger automated strategies.

What to Watch in the Next 12 Months

Three indicators.

Indicator 1: HSBC and Anchorpoint adoption metrics. What is the supply of each stablecoin? What transaction volumes flow through them? Public reporting will reveal trajectory.

Indicator 2: Follow-on issuer applications. Are other Hong Kong banks and financial institutions applying for licenses? Strong demand signals market validation.

Indicator 3: Other Asian financial center frameworks. Do Singapore, Tokyo, Seoul, or Dubai launch competing stablecoin regimes? Regional regulatory diffusion would accelerate the category.

If all three trend positively, Hong Kong establishes itself as a stablecoin hub. If they stagnate, the launch remains a regulatory milestone without major commercial impact.

FAQ

What is the difference between HSBC's stablecoin and Anchorpoint?

Both are HKD-backed stablecoins, but they have different strategic positioning. HSBC's product is positioned for institutional payments and corporate treasury use cases. Anchorpoint (Standard Chartered + Animoca) pursues both institutional and Web3 native use cases. The two are complementary rather than direct competitors.

Why HKD stablecoins rather than USD stablecoins from Hong Kong?

The HKMA framework specifically focuses on HKD-backed stablecoins as part of Hong Kong's monetary sovereignty. USD stablecoins issued from outside Hong Kong continue to operate under different regulatory regimes.

Can I trade HSBC or Anchorpoint stablecoins on global exchanges?

Initial trading is concentrated on major Hong Kong and Asian exchanges. Broader integration will develop over time. Most active crypto traders globally will continue using USDC and USDT for trading pairs while HKD stablecoins develop liquidity.

Are these stablecoins safer than USDT or USDC?

The HKMA framework requires reserves and audits comparable to or stronger than US frameworks. The "safety" of any stablecoin depends on issuer reliability, reserve quality, and regulatory oversight. HKD stablecoins benefit from the HKMA's strong regulatory reputation but lack the operational track record of established players.

Can I trade Hong Kong stablecoins on Altrady?

Trading availability depends on exchange listings. Altrady connects to 19+ exchanges, so you can manage HKD stablecoin positions alongside other crypto holdings on exchanges that list them, run automated strategies via the signal bot, grid bot, or DCA bot, and use unified portfolio tracking.

How can traders verify a Hong Kong stablecoin before using it?

Start with the HKMA register or the issuer's official announcement, then confirm the ticker, chain, and contract address on the exchange where you plan to trade. Do not rely on social posts, unofficial token explorers, or copied brand names. New regulated stablecoin launches often attract fake tokens and phishing pages.

Conclusion

The Hong Kong stablecoin licenses awarded to HSBC and Anchorpoint represent a significant evolution in the global stablecoin landscape. The era when "stablecoin" effectively meant "USD-backed crypto-native token issued by Tether or Circle" is shifting. Major traditional banks, in collaboration with regulators in major financial centers, now operate competing stablecoins under regulated frameworks.

For traders, the practical takeaway is this: USD stablecoins remain dominant for active trading, but the broader category is fragmenting. The next 12-24 months will likely produce additional jurisdiction launches and additional traditional finance issuer entries.

The longer-term implication is positive for crypto infrastructure broadly. More regulated stablecoin issuers create more institutional participation, more compliance clarity, and more capital flowing through crypto rails. The result is a maturing category with reduced existential regulatory risk.

For positioning, the immediate trading impact is modest. The longer-term thesis remains that crypto infrastructure becomes increasingly embedded in traditional finance. Hong Kong's stablecoin licenses are one data point supporting that thesis. Watching how the launches progress over the next year will help confirm or revise the broader narrative.