Pendle Finance has emerged as one of the most distinctive DeFi protocols of the 2024-2026 cycle. By splitting yield-bearing assets into two tradable components (Principal Tokens and Yield Tokens), Pendle created an entirely new asset class within crypto: tradable yield rights. By Q2 2026, Pendle holds approximately $5 billion in total value locked and captures 50-60% of all DeFi yield trading activity, making it the dominant venue for yield speculation and fixed-yield positioning.

For traders, Pendle represents a fundamentally different way of interacting with crypto yields. Rather than holding a yield-bearing asset directly, traders can isolate the principal value (PT) and the yield stream (YT) and trade each separately. This allows specific strategies (fixed yield lock-in, leveraged yield speculation, structured yield products) that did not exist in earlier DeFi.

This guide explains what Pendle is, how PT and YT tokens work, the specific strategies traders use, the risks, and how to think about Pendle exposure in a broader portfolio.

What Is Pendle Finance?

Pendle is a decentralized protocol that enables yield trading by tokenizing the principal and yield components of yield-bearing assets. The protocol launched in 2021 and has scaled significantly through 2024-2026 alongside the broader DeFi recovery.

The core innovation has three components.

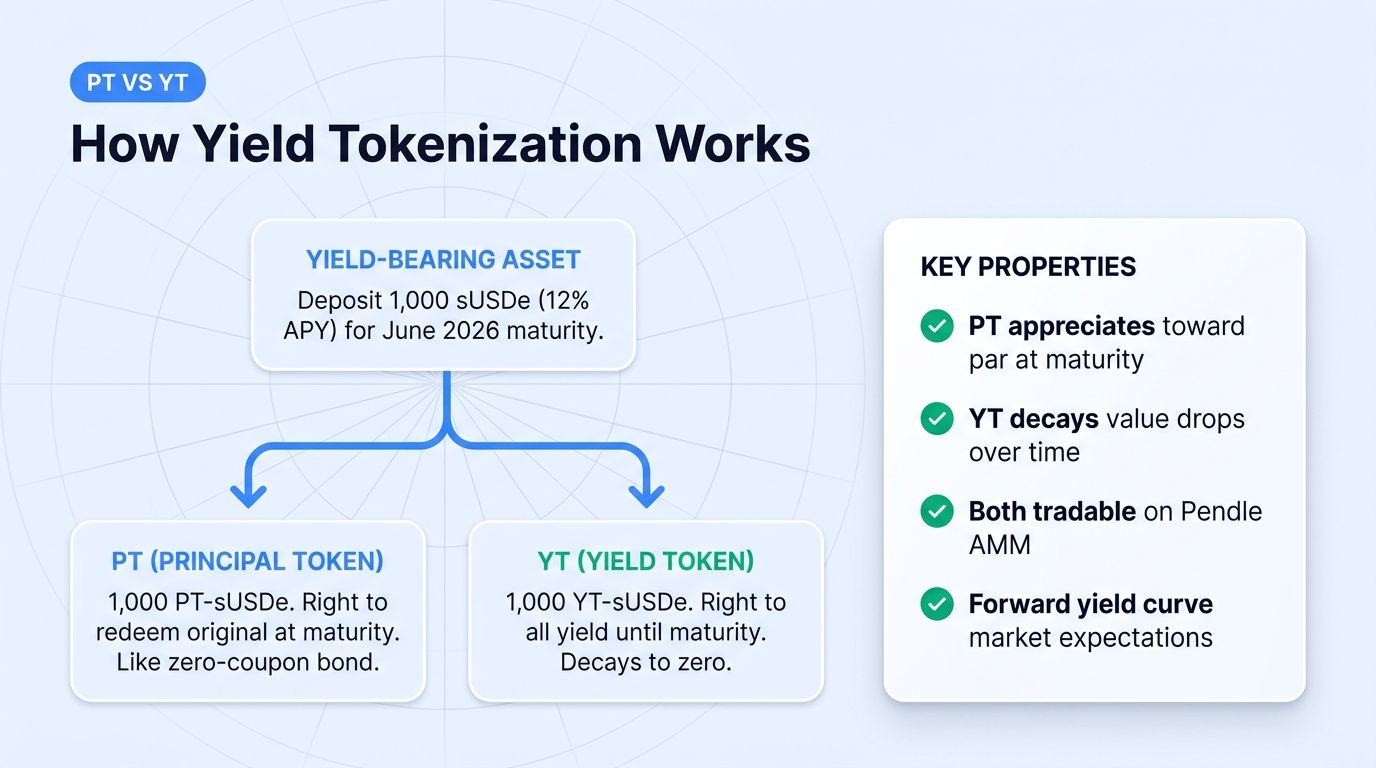

First, yield-bearing asset deposit. Users deposit yield-generating assets (stETH, USDe, eETH, sDAI, others) into Pendle's contract. The contract holds the asset for a specified maturity date.

Second, PT and YT issuance. The protocol issues two new tokens to the depositor. The Principal Token (PT) represents the right to redeem the original asset at maturity. The Yield Token (YT) represents the right to all yield earned by the asset between now and maturity.

Third, secondary market trading. PT and YT can both be traded on Pendle's automated market maker (AMM). Each token has its own price, supply, and demand dynamics. The trading activity creates a yield curve that reveals market expectations about future yield rates.

The result is a protocol where yield itself becomes a tradable asset, separable from the underlying principal.

How PT and YT Work in Practice

A concrete example illustrates the mechanics.

Consider a depositor with 1,000 sUSDe (Ethena's yield-bearing staked USDe stablecoin) that currently yields approximately 12% APY. The depositor wants to hold the sUSDe until June 2026 (six months from now).

Path 1: Deposit and split. 1. Deposit 1,000 sUSDe into Pendle's June 2026 maturity pool 2. Receive 1,000 PT-sUSDe (redeemable for 1,000 sUSDe at June 2026) 3. Receive 1,000 YT-sUSDe (right to all yield earned by 1,000 sUSDe through June 2026) 4. Now hold both tokens, can trade either independently

Path 2: Sell PT, keep YT (leveraged yield speculation). 1. Sell the 1,000 PT-sUSDe at current market price (e.g., 920 USDe equivalent, reflecting 8% discount) 2. Keep the 1,000 YT-sUSDe 3. Use the 920 USDe to buy more YT-sUSDe (or other positions) 4. Total exposure to yield = significantly higher than initial 1,000 sUSDe equivalent

Path 3: Sell YT, keep PT (fixed yield lock-in). 1. Sell the 1,000 YT-sUSDe at current market price 2. Keep the 1,000 PT-sUSDe 3. At maturity, redeem PT for 1,000 sUSDe = 1,000 USDe 4. Effective yield = (1,000 sale of YT) / (initial 1,000 sUSDe value), locked in regardless of actual future rates

The two paths illustrate the protocol's core utility. Traders bullish on yields (expecting them to stay high or increase) buy YT. Traders wanting fixed returns regardless of yield direction buy PT.

The Specific Strategies Traders Use

Several strategies have become standard on Pendle.

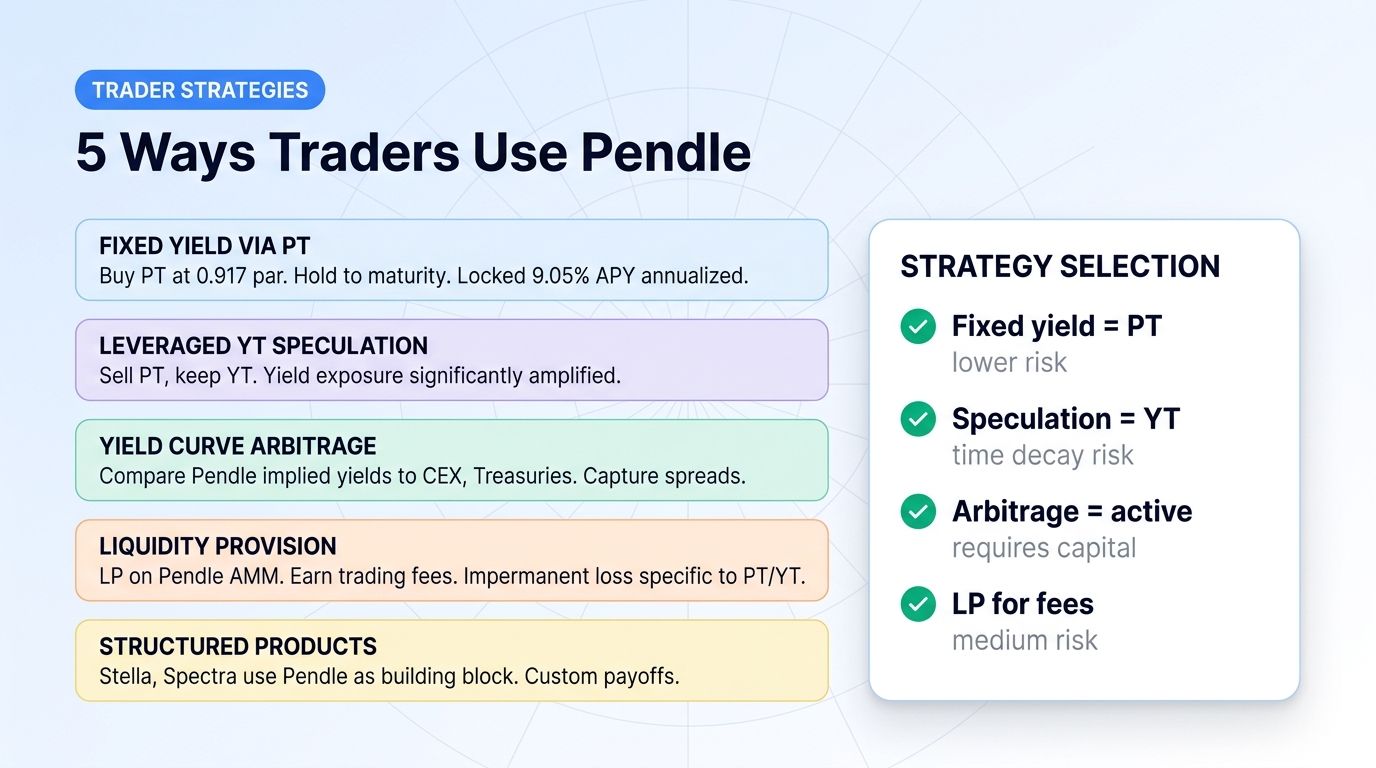

Strategy 1: Fixed Yield via PT

Traders looking to lock in current yields buy PT at a discount and hold to maturity. The implicit yield is fixed at the time of purchase.

Example: PT-sUSDe with June 2026 maturity trading at 0.917 of par. Buying 1,000 PT-sUSDe at $917, holding to June, redeeming for 1,000 sUSDe ($1,000) produces $83 profit on $917 invested = 9.05% annualized.

This strategy is comparable to buying a zero-coupon bond at a discount. It is attractive when traders believe future yields will decline (current rates won't be available later).

Strategy 2: Leveraged Yield Speculation via YT

Traders bullish on yield rates buy YT. YT prices decay toward zero as maturity approaches (since the right to remaining yield diminishes), but if yields increase faster than expected, YT can profit significantly.

Example: YT-eETH (EigenLayer-restaked ETH) traders speculating on points farming or AVS rewards. If actual rewards exceed market-implied expectations, YT generates leveraged returns.

This strategy is high-risk. Time decay is constant, and YT can lose significant value if yields disappoint.

Strategy 3: Yield Curve Arbitrage

Pendle's PT and YT prices imply a forward yield curve. Sophisticated traders compare implied yields across maturities and identify arbitrage between Pendle and other yield sources (CEX lending, DeFi lending, Treasury bills).

When Pendle's implied yield diverges significantly from other markets, arbitrage opportunities exist. Implementing these requires capital, multiple positions, and careful timing.

Strategy 4: Liquidity Provision

Pendle's AMM uses a specialized formula optimized for yield-bearing assets. Liquidity providers earn fees from PT/YT trading. The strategy is comparable to providing liquidity on Uniswap or Curve but with different risk-return characteristics.

LP yields range from modest (low-volume pools) to attractive (high-volume pools), with impermanent loss dynamics specific to the PT/YT structure.

Strategy 5: Structured Products

Pendle's PT and YT serve as building blocks for more complex structured products. Other protocols (Stella, Spectra, others) use Pendle outputs to construct leveraged yield products, capped yield products, and other custom payoffs.

This area is technically complex but represents a growing component of Pendle's ecosystem.

The Pendle Token Economics

The protocol's native token PENDLE has multiple functions.

Staking for vePENDLE: Holders stake PENDLE for vote-escrowed vePENDLE, which provides governance rights and protocol fee sharing. The vePENDLE structure resembles Curve's veCRV.

Liquidity incentives: PENDLE is distributed as incentives to liquidity providers, driving TVL growth.

Protocol fees: Trading fees on PT/YT pairs and other protocol revenue flow partially to vePENDLE holders.

The token has appreciated significantly through 2024-2026 as DeFi yield activity has grown. The economic alignment between protocol growth and token value is relatively direct.

How Pendle Compares to Other Yield Protocols

The DeFi yield landscape has multiple categories.

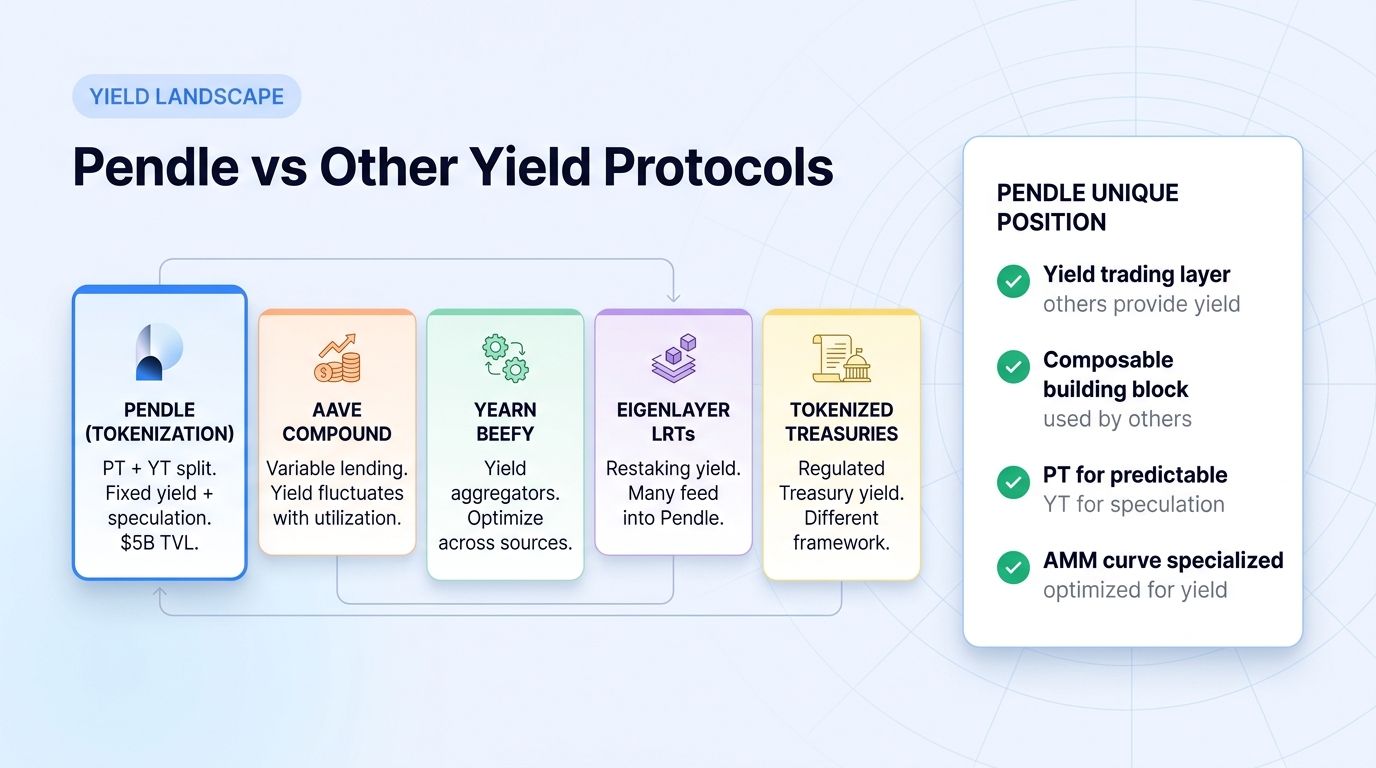

Lending platforms (Aave, Compound): Provide variable-rate lending and borrowing. Yields fluctuate with utilization. No fixed-rate option natively (some innovative products layer on top).

Pendle (yield tokenization): Splits principal and yield into tradable components. Enables fixed yields, leveraged yield speculation, and structured products.

Yield aggregators (Yearn, Beefy, others): Optimize across multiple yield sources. Provide aggregated yields but no direct yield trading.

Restaking and LRT protocols (EigenLayer, ether.fi, others): Generate yield from restaking. Some integrate with Pendle for yield trading.

Tokenized treasury platforms (Ondo, BlackRock BUIDL, others): Provide regulated yield from short-term Treasury bills. Different regulatory framework than DeFi-native yields.

Pendle's unique position is in providing the actual yield trading infrastructure that other protocols' yields can flow through. Many yield-bearing assets are designed with Pendle compatibility in mind.

How Traders Can Get Pendle Exposure

Three practical paths.

Path 1: Trade PT and YT directly on Pendle. Active traders use Pendle's interface to buy and sell PT and YT tokens. This requires understanding the yield mechanics and managing positions through maturity.

Path 2: Hold PENDLE token. Investors who want exposure to the protocol's growth without active yield trading hold PENDLE. Major exchanges (Binance, OKX, others) list PENDLE. Altrady connects to 19+ exchanges and supports unified PENDLE position management.

Path 3: Stake PENDLE for vePENDLE. Long-term holders stake PENDLE for vote-escrowed tokens that share in protocol fees. Yields depend on protocol activity but provide alignment with long-term value.

The Risks of Pendle Trading

Time decay risk on YT. YT loses value as maturity approaches. Holding YT through maturity without realizing gains can result in significant loss.

Underlying asset risk. PT redeems at maturity in the underlying asset, not in dollars. If the underlying loses value (e.g., stETH if Ethereum drops significantly), the PT redemption is in a depreciated asset.

Smart contract risk. Pendle's contracts are complex. Bugs or exploits could affect both PT and YT holders.

Liquidity risk. Specific maturity pools may have thin liquidity. Exiting positions before maturity can face slippage.

Yield variability risk. YT's value depends on actual future yields. If actual yields differ significantly from market expectations, YT performance varies.

Maturity management. Traders must remember maturity dates and manage positions accordingly. Forgetting maturity can leave value uncollected.

How Pendle Fits Into a DeFi Portfolio

A practical framework:

- Yield-bearing stablecoins: 30-50% of DeFi allocation

- Yield aggregators and lending: 20-30%

- Pendle PT (fixed yield): 5-15% for predictable yield lock-in

- Pendle YT (yield speculation): 2-5% maximum due to time decay risk

- Liquidity provision: 10-20%

The PT/YT allocation varies significantly with trader strategy. Active yield traders may concentrate more in Pendle. Conservative investors may use only PT for fixed yield exposure.

What to Watch in the Next 12 Months

Three indicators.

Indicator 1: Pendle TVL growth. Does TVL continue growing beyond $5 billion? Strong growth signals expanding yield-trading category. Stagnation suggests category limits.

Indicator 2: New yield-bearing asset integrations. Are major new yield assets (Western Union USDPT yield variant if launched, additional LRT tokens, tokenized treasury products) adding Pendle compatibility?

Indicator 3: Boros and additional product launches. Pendle has been developing Boros (a new product for trading perp funding rates) and other extensions. Product roadmap execution will affect category growth.

If all three trend positively, Pendle establishes itself as core DeFi infrastructure. If they stagnate, the protocol remains a niche yield-trading venue.

FAQ

What is the difference between PT and YT?

PT (Principal Token) represents the right to redeem the underlying asset at maturity, like a zero-coupon bond. YT (Yield Token) represents the right to all yield earned by the asset until maturity. PT prices appreciate toward par as maturity approaches. YT prices decay toward zero.

Is Pendle safe to use?

Pendle has operated since 2021 without major exploits, undergoing multiple audits. Smart contract risk exists with any DeFi protocol. The yield mechanics are complex and require understanding to use effectively.

Can I lose money on Pendle?

Yes. YT can lose significant value due to time decay. PT can lose value if the underlying asset depreciates. Liquidity provision can experience impermanent loss. As with all DeFi, capital can be lost to smart contract bugs.

What yield-bearing assets work with Pendle?

Pendle supports many yield-bearing assets including stETH, eETH (EigenLayer restaked), sUSDe (Ethena), sDAI, tokenized treasuries, and others. The protocol adds new assets based on market demand and security review.

Can I trade Pendle on Altrady?

PENDLE is listed on Binance, OKX, Bybit, KuCoin, and other major exchanges. Altrady connects to 19+ exchanges, so you can manage PENDLE positions alongside other crypto holdings, run automated strategies via the signal bot, grid bot, or DCA bot, and use unified portfolio tracking. Direct PT/YT trading happens on Pendle's protocol interface.

Conclusion

Pendle Finance represents one of the most distinctive DeFi protocols of the current cycle. By creating tradable yield rights through PT and YT tokens, the protocol enabled an entirely new category of crypto trading: yield speculation and fixed-yield positioning.

For traders, the practical takeaway is this: Pendle is technically sophisticated and primarily appeals to active DeFi yield traders. Casual investors should focus on the simpler PT (fixed yield) products rather than YT (yield speculation) products that require careful time-decay management.

The longer-term significance is that Pendle has created infrastructure that other protocols can build on. Many yield-bearing assets are now designed with Pendle integration in mind. As DeFi continues maturing, yield trading is likely to become a standard component of the DeFi infrastructure stack.

For diversified crypto portfolios, a moderate Pendle allocation makes sense: small PT positions for predictable yield, very small YT positions for high-conviction yield-speculation opportunities, and possibly PENDLE governance token exposure for those bullish on the protocol's long-term growth. The next 12 months will produce decisive data on whether Pendle scales beyond $5 billion TVL or stabilizes at current levels.