Tokenized deposits are becoming one of the most important digital dollar topics for traders to understand. They sound similar to stablecoins because both can move value on blockchain-style rails, but the legal and market structure can be very different.

In June 2026, CoinDesk reported that major U.S. banks including JPMorgan Chase, Bank of America, Citigroup, and others plan a shared tokenized deposit network through The Clearing House by the first half of 2027. The point is clear: banks want blockchain-speed settlement without letting stablecoins own the digital dollar relationship.

What Is a Tokenized Deposit?

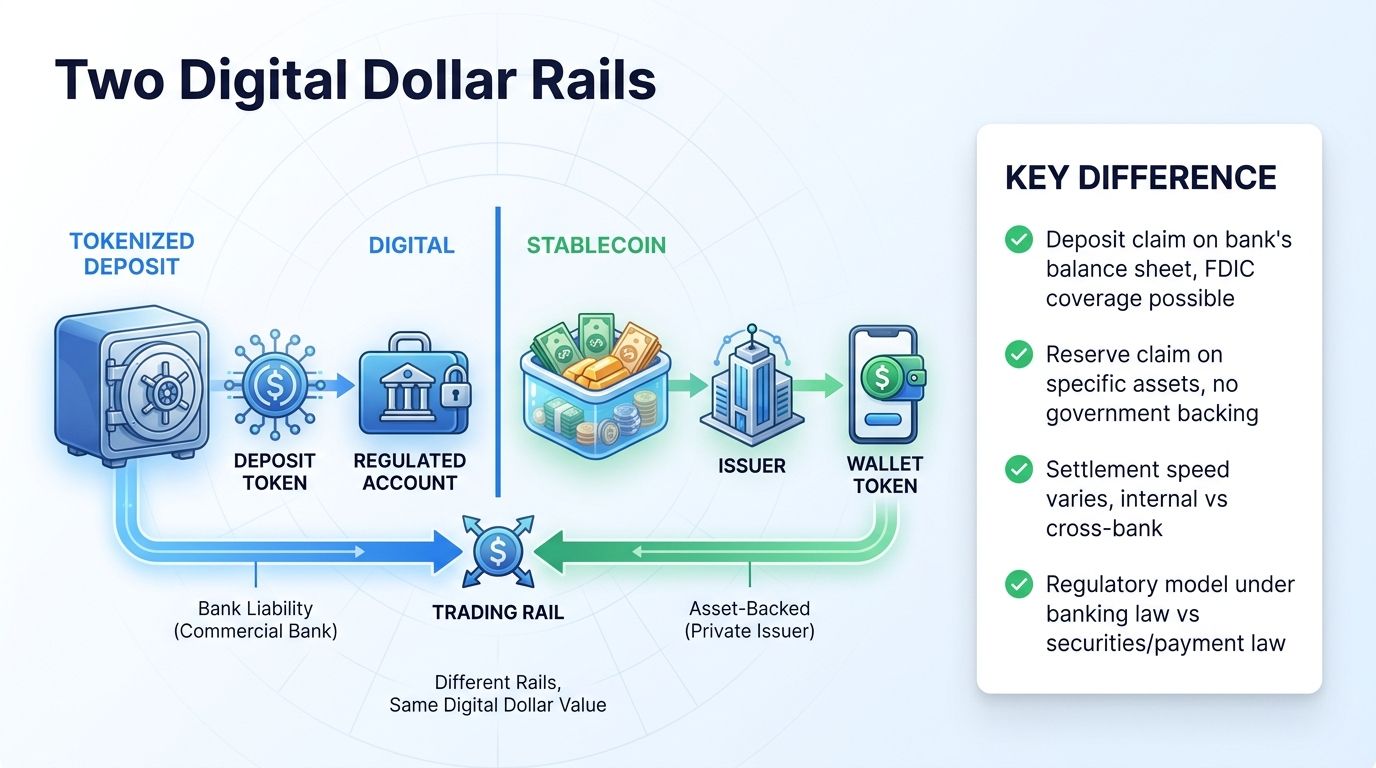

A tokenized deposit is a bank deposit represented as a digital token. The customer claim remains a deposit claim on a regulated bank, but the representation can move through a faster settlement network. In simple terms, it is bank money with a programmable wrapper.

That makes it different from a typical stablecoin. A stablecoin is usually issued by a non-bank or specialized issuer and backed by reserves such as cash, Treasury bills, or other approved assets. A tokenized deposit is designed to keep the money inside the banking system.

- Tokenized deposits represent commercial bank deposits.

- Stablecoins usually represent claims on an issuer's reserves.

- Both can improve digital settlement.

- The legal claim and risk profile are different.

Why Banks Are Building This Now

Stablecoins have become useful because they move quickly, operate outside normal banking hours, and plug into crypto markets, payment apps, and tokenized asset platforms. That creates pressure on banks because deposits are the core funding base of the banking system.

A shared tokenized deposit network is a defensive and offensive move. It defends bank deposits from stablecoin competition, while giving banks a way to offer faster corporate treasury movement, cross-border settlement, and richer payment data.

- Stablecoins showed demand for 24/7 digital dollars.

- Banks want faster settlement without losing deposits.

- Corporate treasury use cases may come first.

- Shared rails can reduce fragmentation between banks.

How This Competes With Stablecoins

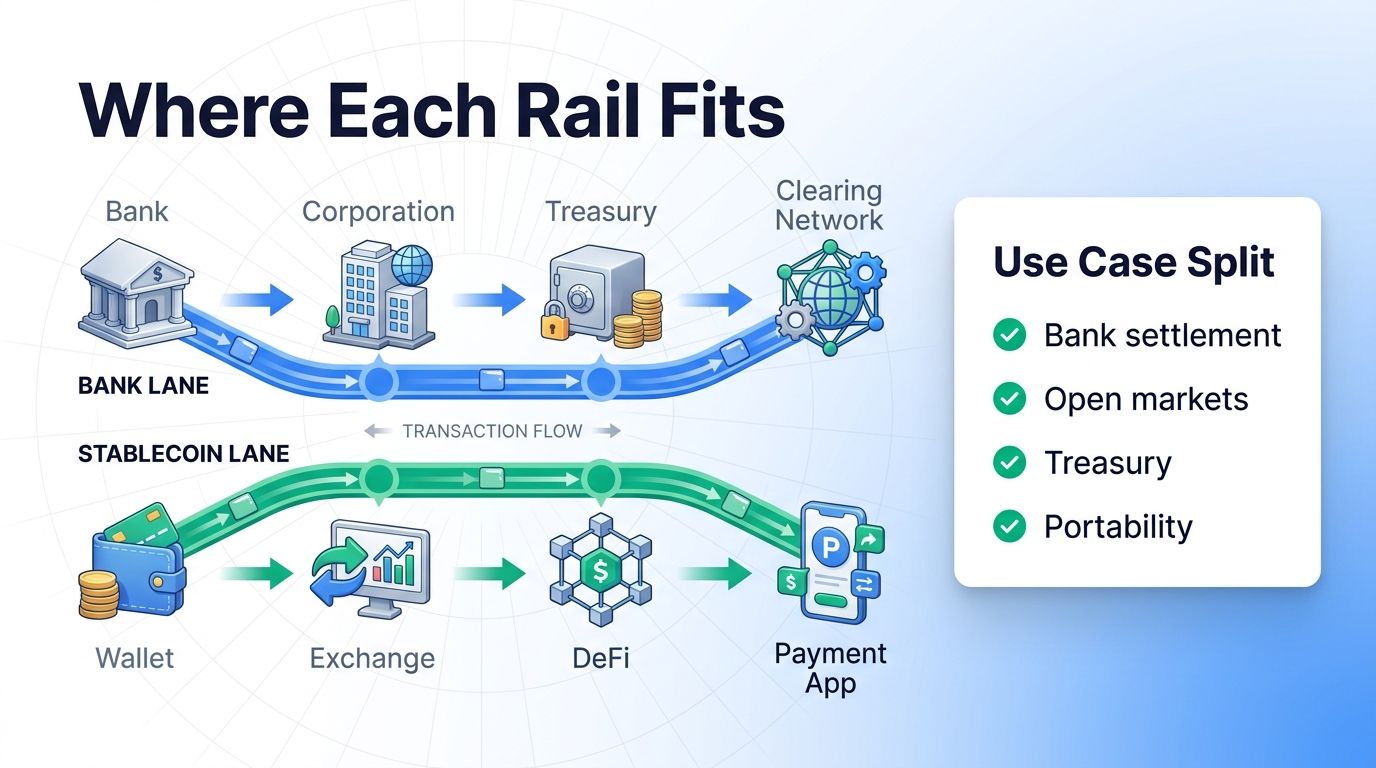

Tokenized deposits compete with stablecoins where users mainly want fast dollar settlement inside a regulated financial relationship. A company moving money between banks may prefer a deposit token because it already fits banking controls, balance-sheet treatment, and existing payment workflows.

Stablecoins may still lead in open crypto markets. They are easier to move between wallets, exchanges, DeFi protocols, and global trading venues. That openness is powerful, but it also creates compliance, custody, and issuer-risk questions that banks may want to avoid.

- Tokenized deposits fit bank-to-bank settlement.

- Stablecoins fit open wallet and exchange activity.

- Corporate users may care more about bank integration.

- Crypto-native users may care more about portability.

What Traders Should Watch

The first thing to watch is whether the network actually launches on schedule. The second is whether it supports meaningful transaction volume. A pilot with a few banks is not the same as a deep settlement rail used by major corporations every day.

The third thing is how stablecoin issuers respond. If tokenized deposits make bank settlement faster, stablecoin issuers may emphasize open networks, cross-border reach, developer tools, yield-bearing products, or integration with tokenized assets. The digital dollar market can grow while competition inside it intensifies.

- Track launch timing and participating banks.

- Watch transaction volume and use cases.

- Compare bank rails with stablecoin issuer growth.

- Look for tokenized asset settlement demand.

Why This Matters for Crypto Markets

Tokenized deposits could change the stablecoin story from a simple crypto adoption narrative into a competition between different forms of digital dollars. Stablecoins, tokenized deposits, money market tokens, and central bank systems can all serve different parts of the same value-transfer problem.

For traders, this matters because digital dollars are the base layer for many crypto markets. If bank rails become faster, some corporate payment activity may stay inside banks. If stablecoins keep winning in open markets, issuers and networks connected to stablecoin liquidity may keep growing.

The useful question is not which rail wins everything. The useful question is which rail wins each use case.

- Digital dollars are becoming more segmented.

- Bank settlement and open crypto markets may diverge.

- Stablecoin issuers still have open-network advantages.

- Use-case share matters more than broad labels.

Bottom Line

Tokenized deposits are bank money adapted for faster digital settlement. Stablecoins are issuer-backed digital dollars built for open networks. They overlap, but they are not the same product.

The 2027 tokenized deposit plans show that large banks take stablecoin competition seriously. They also show that traditional finance is adopting blockchain-style infrastructure in a controlled way.

Traders should watch launch timing, real usage, bank participation, stablecoin supply, and how tokenized asset markets choose settlement rails.

- Tokenized deposits keep money inside banks.

- Stablecoins remain stronger in open crypto markets.

- Competition may expand the whole digital dollar category.

- Real volume will matter more than announcements.

How to Compare Digital Dollar Rails

The cleanest comparison starts with the user. A corporate treasurer may value bank integration, clear account treatment, and familiar counterparties. A crypto trader may value fast exchange transfers, wallet portability, and access to DeFi liquidity. Both users want dollars, but they do not need the same rail.

The second comparison is access. Tokenized deposits may be limited to approved institutions or bank customers at first. Stablecoins are usually easier to move across exchanges, wallets, and applications, although that openness brings its own custody and compliance considerations.

The third comparison is market impact. If tokenized deposits mostly serve bank treasury movement, the direct effect on crypto exchange liquidity may be limited. If stablecoins keep growing as trading collateral and payment rails, they may remain more visible to crypto market structure.

A trader should track each rail by its own job. Bank money, exchange money, DeFi collateral, and payment app balances may all coexist.

This also keeps the stablecoin thesis from becoming too broad. A dollar token used for exchange liquidity should not be judged by the same metrics as a bank deposit token used for corporate treasury settlement. Different rails need different dashboards.

For traders, the best dashboard combines supply, transfer activity, venue support, issuer quality, and the type of user driving demand. That prevents a bank infrastructure story from being mistaken for exchange liquidity. It also helps separate payment adoption from speculative demand, which can move at very different speeds. The more specific the metric, the cleaner the conclusion. This is especially useful when headlines use the same digital dollar language across very different products.

- Start with the user and use case.

- Compare access and portability.

- Separate bank settlement from exchange liquidity.

- Expect several digital dollar rails to coexist.

FAQ

What is a tokenized deposit?

It is a commercial bank deposit represented as a digital token that can move on faster settlement rails.

How is a tokenized deposit different from a stablecoin?

A tokenized deposit is a claim on a bank deposit. A stablecoin is usually a claim on an issuer's reserve assets.

Why are banks building tokenized deposits?

Banks want faster digital settlement while keeping deposits within the regulated banking system.

Will tokenized deposits replace stablecoins?

Not necessarily. Tokenized deposits may fit bank settlement, while stablecoins may remain stronger in open crypto markets.