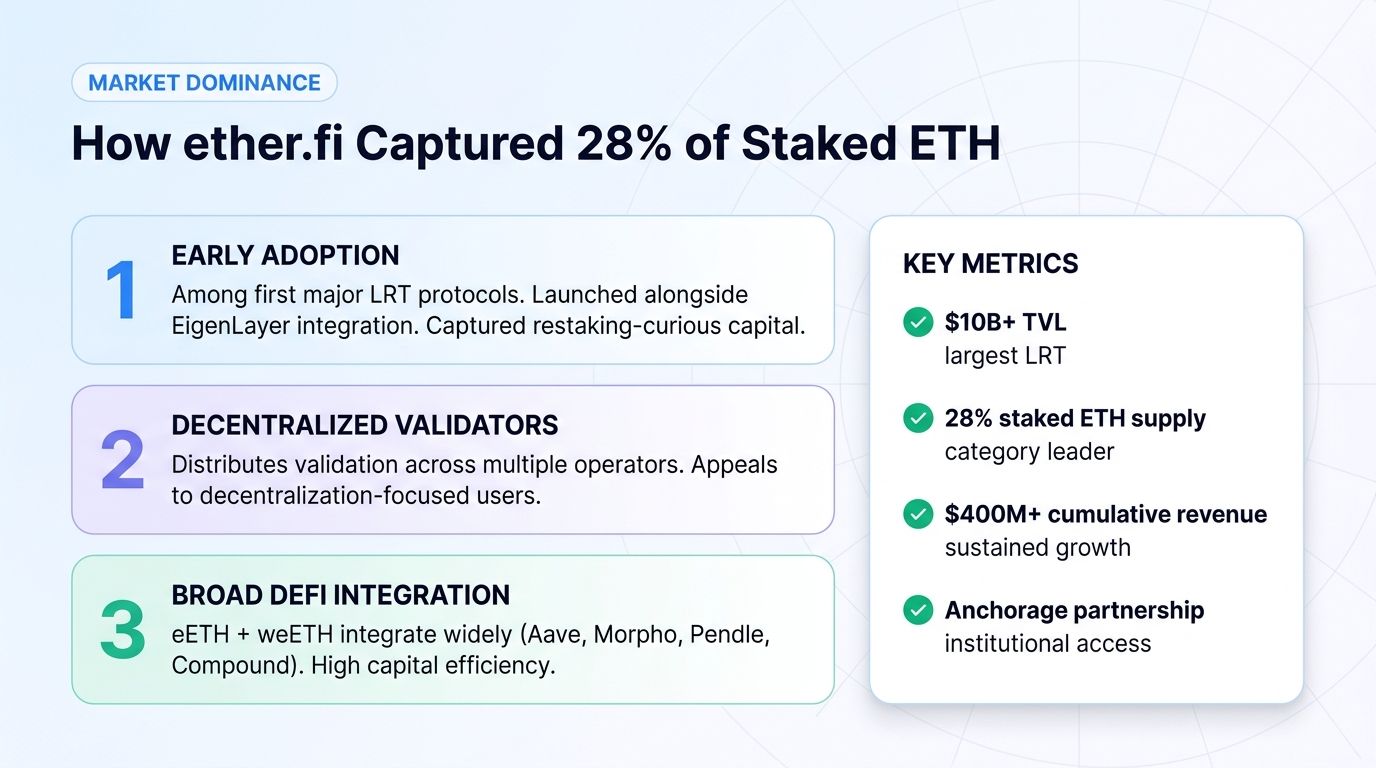

ether.fi has emerged as the largest liquid restaking protocol (LRT) of the current cycle. By Q2 2026, the protocol surpassed $10 billion in total value locked, captures approximately 28% of all staked ETH supply, and has generated over $400 million in cumulative staking revenue. The combination makes ether.fi the dominant LRT and one of the most consequential protocols in Ethereum's restaking ecosystem.

For traders and ETH holders, ether.fi represents a specific category of yield-bearing Ethereum exposure. By depositing ETH into ether.fi, holders receive eETH (a liquid token representing the staked position) and earn yields from both Ethereum staking and EigenLayer-based actively validated services (AVSs). The combination produces a yield stack that exceeds either standalone source.

This guide explains what ether.fi is, the EETH token mechanics, how it compares to other LRTs (Lido stETH, Renzo, Kelp DAO), the institutional partnerships expanding access, the risks, and how to think about ether.fi exposure in a broader ETH strategy.

What Is ether.fi?

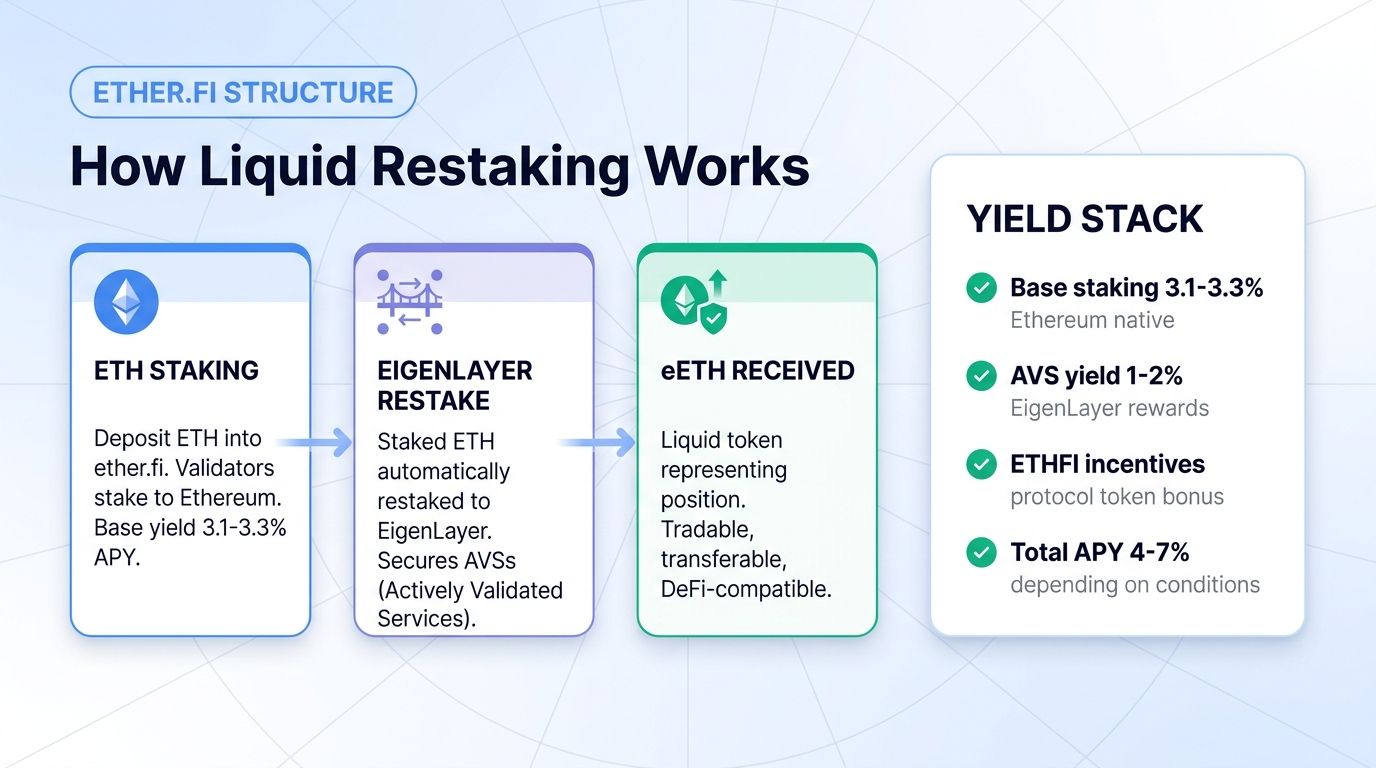

ether.fi is a decentralized liquid restaking protocol built on Ethereum. The protocol allows ETH holders to stake their ETH (gaining base staking yield) and simultaneously restake to EigenLayer (gaining additional yield from AVS rewards). Users receive eETH tokens representing their staked position, which can be transferred, traded, or deployed in other DeFi protocols.

The architecture has three core components.

First, native ETH staking. Users deposit ETH into ether.fi, which stakes the ETH through validator infrastructure. Stakers earn the base Ethereum staking yield (currently 3.1-3.3% APY).

Second, EigenLayer restaking. The staked ETH is also restaked to EigenLayer, providing security to AVSs (Actively Validated Services). Stakers earn additional yield from these services.

Third, liquid representation. Users receive eETH (or weETH, the wrapped version) tokens that represent their position. These tokens trade on DEXs, integrate with DeFi lending platforms (Aave, Morpho, others), and can be used as collateral.

The result is a single token (eETH) that captures Ethereum staking yield plus EigenLayer restaking yield, while remaining liquid and DeFi-compatible.

The Token Economics

ether.fi operates with two related tokens and a third governance token.

eETH: The primary staking token. Each eETH represents 1 ETH worth of staked + restaked exposure. Yield accumulates by increasing the underlying ETH balance over time (rebasing model).

weETH (wrapped eETH): A wrapped version of eETH that does not rebase. Each weETH represents a growing share of the ETH-backed pool. More DeFi-compatible than rebasing eETH.

ETHFI (governance): The governance token. Holders vote on protocol parameters, fee structures, and ecosystem grants. ETHFI also captures economic value through protocol revenue sharing.

The yield stack for eETH holders includes:

- Base Ethereum staking yield: 3.1-3.3% APY

- EigenLayer AVS rewards: 1-2% APY (variable based on AVS adoption and economics)

- ETHFI token incentives: distributed periodically as the protocol grows

- Cross-protocol points and incentives: variable

The combined APY typically falls in the 4-7% range, with periodic boosts from new product launches and incentive programs.

How ether.fi Achieved 28% of Staked ETH Supply

ether.fi's market share growth has been remarkable. The protocol launched in early 2024 and reached $10 billion TVL by early 2026, representing 28% of total staked ETH supply.

Three structural factors drove the growth.

First, early restaking adoption. ether.fi was among the first major LRT protocols to launch and integrated with EigenLayer at launch. Early movers captured the bulk of restaking-curious capital.

Second, decentralized validator architecture. Unlike some competitors that rely on centralized validator pools, ether.fi distributes validation across multiple operators. This appeals to users who prioritize decentralization and resilience.

Third, broad DeFi integration. eETH and weETH integrate widely across DeFi protocols (Aave, Morpho, Pendle, Compound, others). The liquid token can be used in many strategies, increasing its capital efficiency.

The growth trajectory has not been linear. ether.fi gained significant TVL during the 2024 "restaking summer" period, plateaued briefly in late 2024, then resumed growth as the broader restaking category matured.

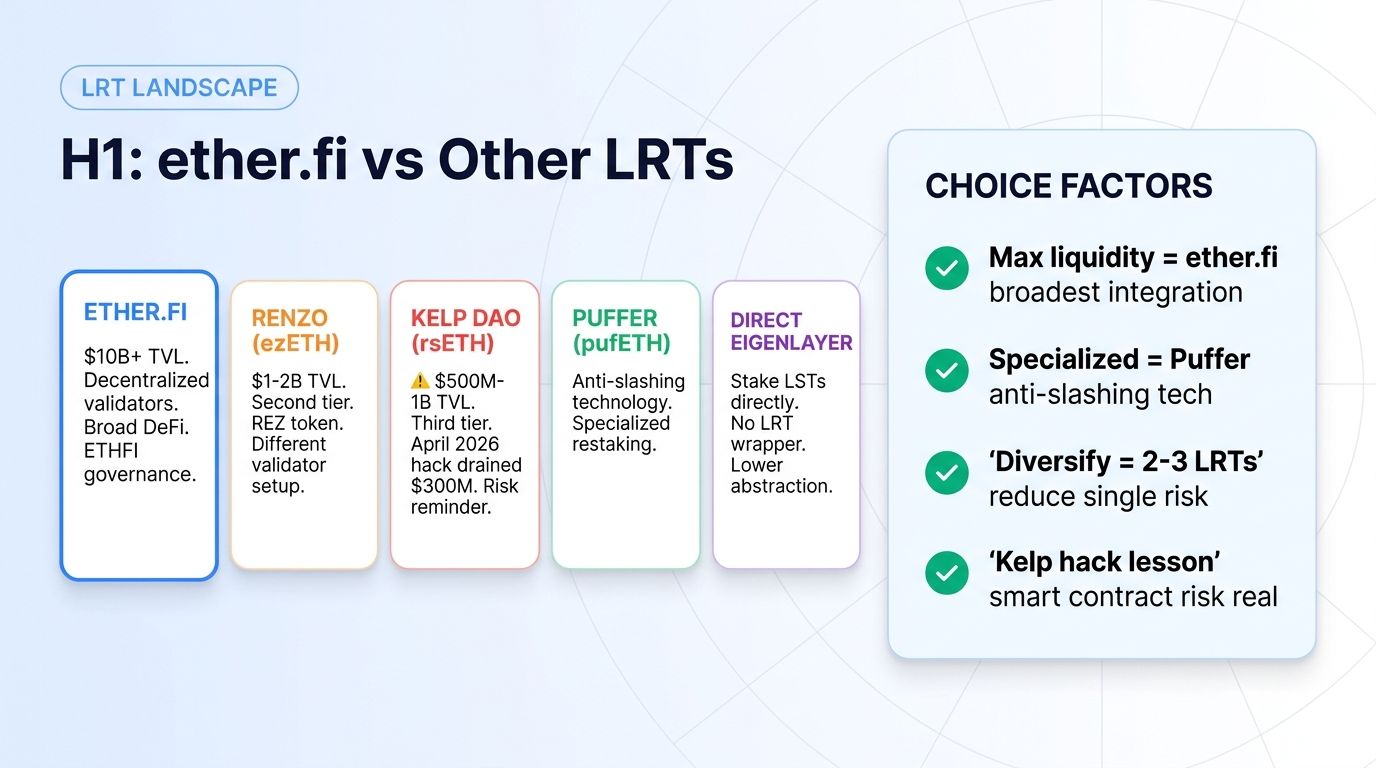

How ether.fi Compares to Other LRTs

The LRT landscape has multiple major protocols.

ether.fi: Largest LRT at $10B+ TVL. Decentralized validator architecture. Strong DeFi integration. ETHFI governance token.

Renzo (ezETH): Second-tier LRT. $1-2B TVL. Different validator setup. REZ token.

Kelp DAO (rsETH): Third-tier LRT. $500M-1B TVL. The Kelp DAO hack in April 2026 drained $300M from one part of the stack, demonstrating real-world LRT risks.

Puffer Finance (pufETH): Specialized in decentralized restaking with anti-slashing technology.

Eigenpie (mLRT variants): Aggregator approach across multiple yield sources.

Direct EigenLayer restaking (no LST): Stake LSTs directly to EigenLayer without wrapping in an LRT.

For traders, the choice depends on priorities:

- Maximum liquidity and DeFi integration: ether.fi

- Specialized features: Specific protocols (Puffer for anti-slashing, others for specific AVS exposure)

- Diversification across LRTs: hold smaller positions in multiple protocols

The Anchorage Institutional Partnership

In early 2026, Anchorage Digital announced expanded institutional access to ether.fi for ETH restaking. The partnership matters for several reasons.

First, institutional capital can now access ether.fi through regulated channels. Anchorage is a federally chartered crypto bank with strong institutional client relationships.

Second, the partnership validates ether.fi's institutional readiness. Major institutions don't partner with protocols they consider unsafe.

Third, the partnership creates structural demand. As institutions deploy ETH through ether.fi via Anchorage, TVL growth accelerates.

The Anchorage partnership is one of several institutional integrations. Other major custodians and institutional platforms are expected to add ether.fi access during 2026.

How Traders Can Get ether.fi Exposure

Three practical paths.

Path 1: Stake ETH through ether.fi to receive eETH or weETH. Direct exposure to the yield stack. Liquid token for DeFi integration. Requires using ether.fi's interface.

Path 2: Hold ETHFI governance token. Exposure to protocol growth and governance rights. Available on major exchanges. Altrady connects to 19+ exchanges and supports unified ETHFI position management.

Path 3: Indirect exposure through DeFi protocols using eETH. Some DeFi protocols use eETH as a yield-bearing asset. Holding tokens of these protocols provides indirect ether.fi exposure.

The Risks of ether.fi and LRT Investment

Smart contract risk. ether.fi's contracts and the EigenLayer infrastructure have undergone audits but complex DeFi systems can have unforeseen issues. The Kelp DAO hack in April 2026 demonstrated real-world LRT risk.

Restaking slashing risk. EigenLayer AVS slashing can affect underlying ETH. While slashing is rare under normal operations, the risk is real for any restaking position.

Withdrawal queue and liquidity risk. Withdrawing from ether.fi requires either using the protocol's withdrawal mechanism (which may have delays) or selling eETH on secondary markets (which may face slippage).

Concentration risk. ether.fi's 28% market share creates concentration risk for the overall LRT category. Issues at ether.fi would affect a significant portion of restaked ETH.

Validator operator risk. ether.fi distributes validation across multiple operators, but operator-specific issues (downtime, slashing) can affect users.

Token unlock pressure. ETHFI has multi-year vesting schedules. Continued unlocks create supply pressure that may affect price.

Regulatory risk. While the March 2026 SEC interpretive release clarified protocol staking, LRT-specific regulatory treatment continues evolving.

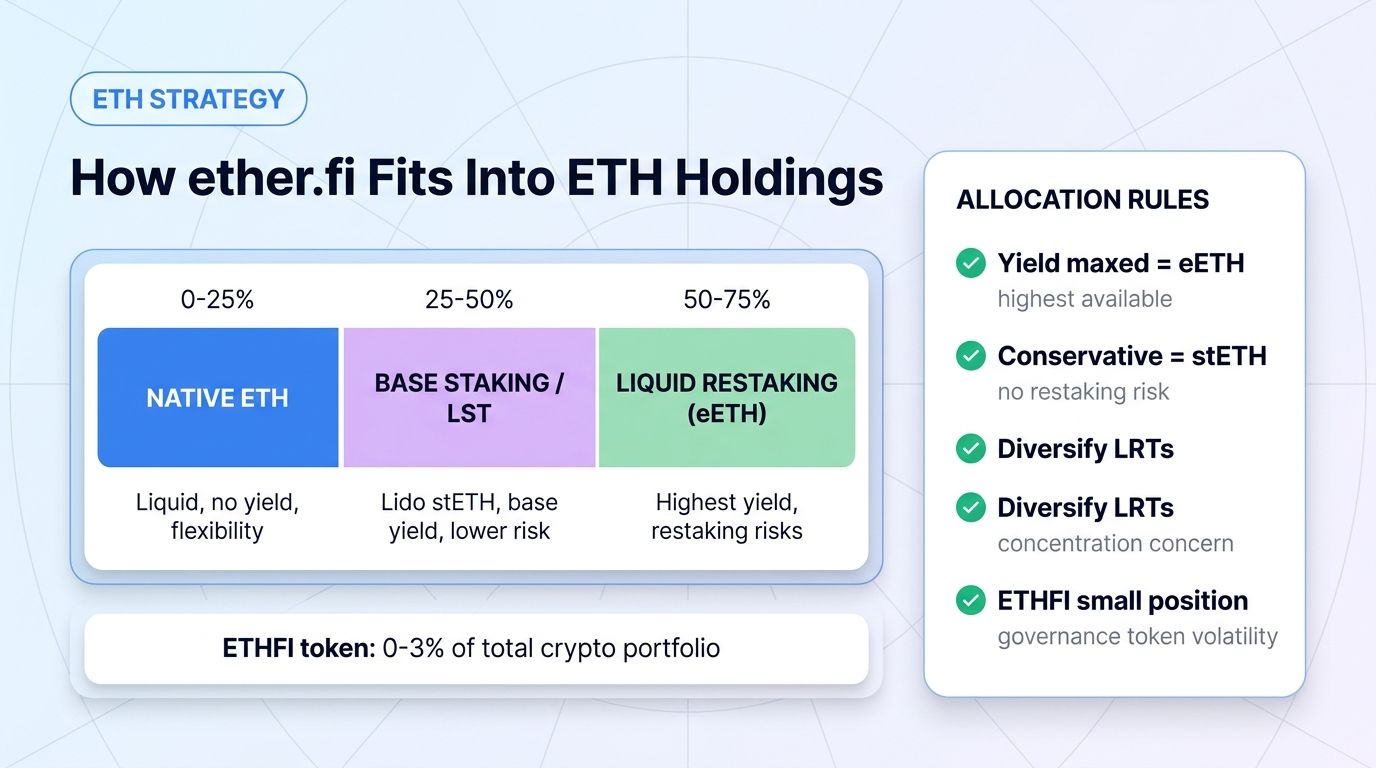

How ether.fi Fits Into an ETH Strategy

A practical framework for ETH holders:

- Native ETH (no staking): 0-25% of ETH allocation, depending on liquidity needs

- Direct ETH staking or LST (Lido stETH): 0-50% of ETH allocation

- Liquid restaking (ether.fi eETH): 25-75% of ETH allocation for those prioritizing yield

- Concentrated single-protocol risk awareness: Diversifying across 2-3 LRTs may be prudent

For ETHFI governance token specifically:

- 0-3% of total crypto portfolio as concentrated position on ether.fi protocol growth

- Higher conviction users may go to 5-7%; lower conviction users may pass entirely

What to Watch in the Next 12 Months

Three indicators.

Indicator 1: TVL trajectory. Does ether.fi continue growing beyond $10B? Strong growth signals continued LRT category expansion.

Indicator 2: AVS adoption. Do more AVSs launch on EigenLayer and generate meaningful yield for ether.fi stakers? Strong AVS economics validate the restaking thesis.

Indicator 3: Institutional partnership expansion. Do additional major custodians and institutional platforms integrate ether.fi? Broader institutional access supports continued growth.

If all three trend positively, ether.fi consolidates its category leadership. If issues emerge (AVS economics fail, security incidents), competitor LRTs or alternative approaches may gain market share.

FAQ

What is the difference between staking and restaking?

Staking is providing ETH to secure the Ethereum network and earning base staking rewards (currently 3.1-3.3% APY). Restaking takes the staked ETH and additionally uses it to secure other services (AVSs) through EigenLayer, earning additional yield on top of base staking yield.

How is ether.fi different from Lido?

Lido is the largest pure liquid staking protocol (no restaking). Lido stETH earns base Ethereum staking yield only. ether.fi adds the EigenLayer restaking layer, generating additional yield from AVSs. ether.fi typically yields slightly more than Lido but carries additional restaking-related risks.

Can ether.fi tokens lose value?

Yes. eETH tracks ETH price, so it loses dollar value if ETH price declines. ETHFI governance token is a separate volatile crypto asset subject to standard token volatility. Slashing events (rare) can also affect underlying ETH staked through ether.fi.

What was the Kelp DAO hack of April 2026?

In April 2026, a vulnerability in part of Kelp DAO's infrastructure drained approximately $300 million. The exploit was specific to Kelp DAO's implementation but affected withdrawal flows across multiple protocols that shared certain dependencies. The incident demonstrated that LRT smart contract risks are real and continue requiring careful protocol selection.

Can I trade ETHFI on Altrady?

ETHFI is listed on Binance, OKX, Bybit, KuCoin, MEXC, Bitget, and most major exchanges. Altrady connects to 19+ exchanges, so you can manage ETHFI positions alongside other crypto holdings, run automated strategies via the signal bot, grid bot, or DCA bot, and use unified portfolio tracking.

Conclusion

ether.fi has established itself as the dominant liquid restaking protocol of the 2024-2026 cycle. With $10B+ TVL, 28% of staked ETH supply, and over $400M in cumulative revenue, the protocol represents a meaningful category of Ethereum yield generation.

For traders, the practical takeaway is this: ether.fi provides one of the highest-yield ETH exposures available without abandoning self-custody or DeFi integration. The yield stack (Ethereum staking + EigenLayer AVS rewards + protocol incentives) typically exceeds either source alone.

The longer-term trajectory depends on AVS adoption growing meaningfully on EigenLayer (validating the restaking thesis), on competitor LRTs maintaining their market positions versus ether.fi, and on continued institutional partnership expansion. The next 12 months will produce decisive data on each.

For diversified crypto portfolios, allocating a portion of ETH exposure to ether.fi makes sense for yield-focused investors comfortable with restaking risks. ETHFI governance token allocation should follow standard high-volatility token sizing. Sizing positions to a level where worst-case scenarios do not damage your portfolio is the standard discipline.