ETH stakers know the base yield. Around 3-4% APY for validating Ethereum. For users seeking more, the answer for the last two years has been EigenLayer, the protocol that pioneered restaking.

By April 2026, EigenLayer secured tens of billions of dollars in restaked assets across over 100 actively validated services. The protocol turned Ethereum's economic security into a commodity that other networks can rent, creating an entirely new layer of crypto infrastructure. The liquid restaking tokens (LRTs) you may have heard about, weETH from ether.fi, rsETH from Kelp, ezETH from Renzo, all flow through EigenLayer.

This guide explains what EigenLayer is, how restaking works at a technical level, the role of AVSs (Actively Validated Services), the specific risks restakers accept, and how to evaluate EigenLayer-based products before committing capital.

What Is EigenLayer?

EigenLayer is a protocol that lets ETH stakers extend their staked ETH to secure additional services on top of Ethereum. Without leaving the Ethereum validator set, a staker can also pledge their stake to validate other networks (called Actively Validated Services or AVSs).

The economic logic is simple. A new blockchain or middleware service needs security. Building that security from scratch is expensive (you would need to bootstrap a validator network with billions of dollars in staked value). EigenLayer lets that service borrow Ethereum's existing security, paying restakers in fees or token rewards.

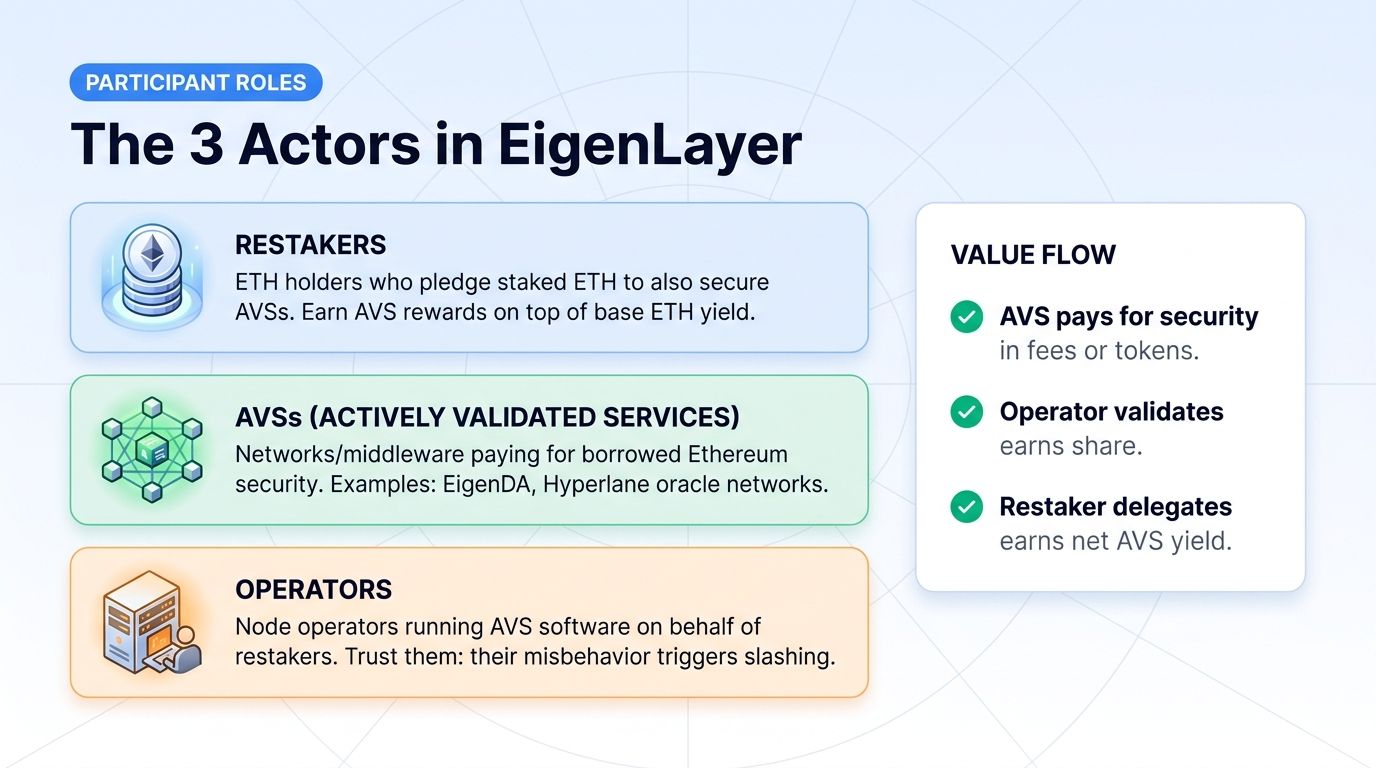

Three actors: - Restakers: ETH holders who pledge their staked ETH to secure additional services - AVSs (Actively Validated Services): Networks or middleware that pay for borrowed security - Operators: Node operators who run the validation software for AVSs on behalf of restakers

A concrete example. EigenDA is an AVS that provides data availability services. It needs validators to make sure data is published correctly. Instead of building its own validator set, EigenDA pays restakers via EigenLayer. Restakers earn EigenDA's reward tokens on top of their Ethereum staking yield.

Why EigenLayer Matters in 2026

Three forces drove adoption.

First, Ethereum staking saturated around 25-30% of total ETH supply. Marginal staking yields drift down as more ETH is staked. The base rate of 3-4% APY became the floor, with stakers looking for ways to compound additional yield on the same staked ETH.

Second, the AVS economy emerged. Data availability layers (EigenDA), bridges (Hyperlane), oracle networks (Eoracle), and shared sequencers all started borrowing Ethereum's security. By 2026, the AVS ecosystem included 100+ projects, each paying restakers for security.

Third, liquid restaking tokens (LRTs) made the user experience accessible. Before LRTs, restakers had to manage delegations to operators, choose AVSs, and monitor slashing risk. With LRTs (weETH, rsETH, ezETH), a user could deposit ETH and receive a token that automatically participates in the restaking economy.

By April 2026, EigenLayer secured tens of billions in restaked assets, with the broader restaking economy (including LRT protocols, AVSs, and supporting infrastructure) generating real fee revenue from the services using borrowed security.

How Restaking Works Technically

Three mechanics matter.

Stake Delegation

When you restake ETH through EigenLayer, you do not move your ETH from the Ethereum validator set. You add an additional commitment: your stake also backs the AVS you delegate to.

Specifically, you opt into AVS validation by signing a permission for a specific operator. The operator runs the AVS software and produces validator signatures. If the operator behaves correctly, you earn AVS rewards. If the operator behaves incorrectly, EigenLayer can slash a portion of your staked ETH as punishment.

AVS Selection

EigenLayer supports many AVSs. Each has different reward structures, slashing conditions, and risk profiles. Restakers (or LRT protocols acting on their behalf) decide which AVSs to validate.

Some AVSs pay in their native token. Some pay in ETH. Some pay in stablecoins. The composition of AVS rewards determines the effective yield for restakers.

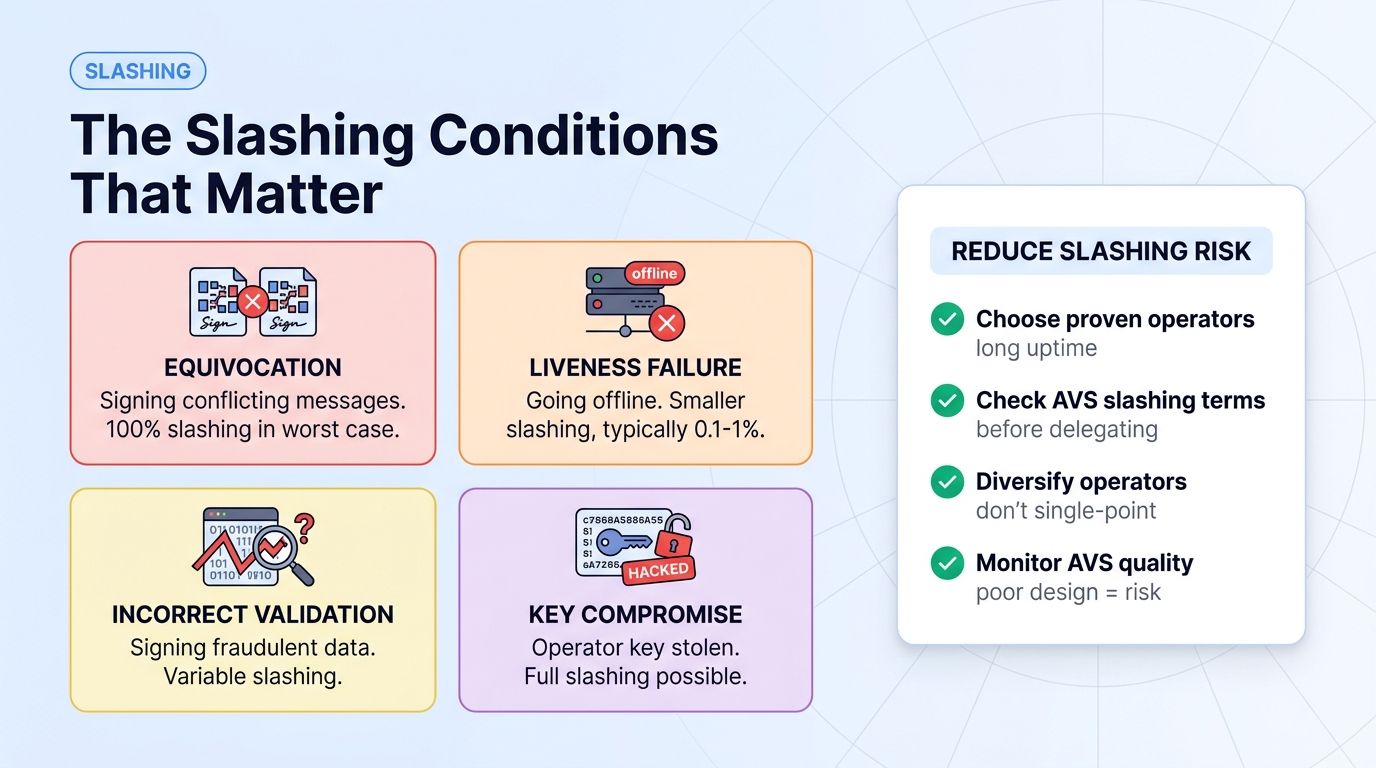

Slashing Conditions

EigenLayer's slashing mechanism is the protocol's biggest innovation and biggest risk. Each AVS defines its own slashing conditions, the specific bad behaviors that trigger penalties. Examples: - Equivocation (signing conflicting messages) - Liveness failure (going offline) - Incorrect validation (signing fraudulent data)

If an operator triggers a slashing condition on an AVS, all restakers delegated to that operator can lose a portion of their stake. The slashing percentage varies by AVS and offense type.

This is why operator selection matters. A poorly-run operator can trigger slashing on multiple AVSs simultaneously, draining a meaningful percentage of your restaked ETH.

The Liquid Restaking Token (LRT) Layer

Most retail users do not interact with EigenLayer directly. They use LRT protocols, which handle the complexity.

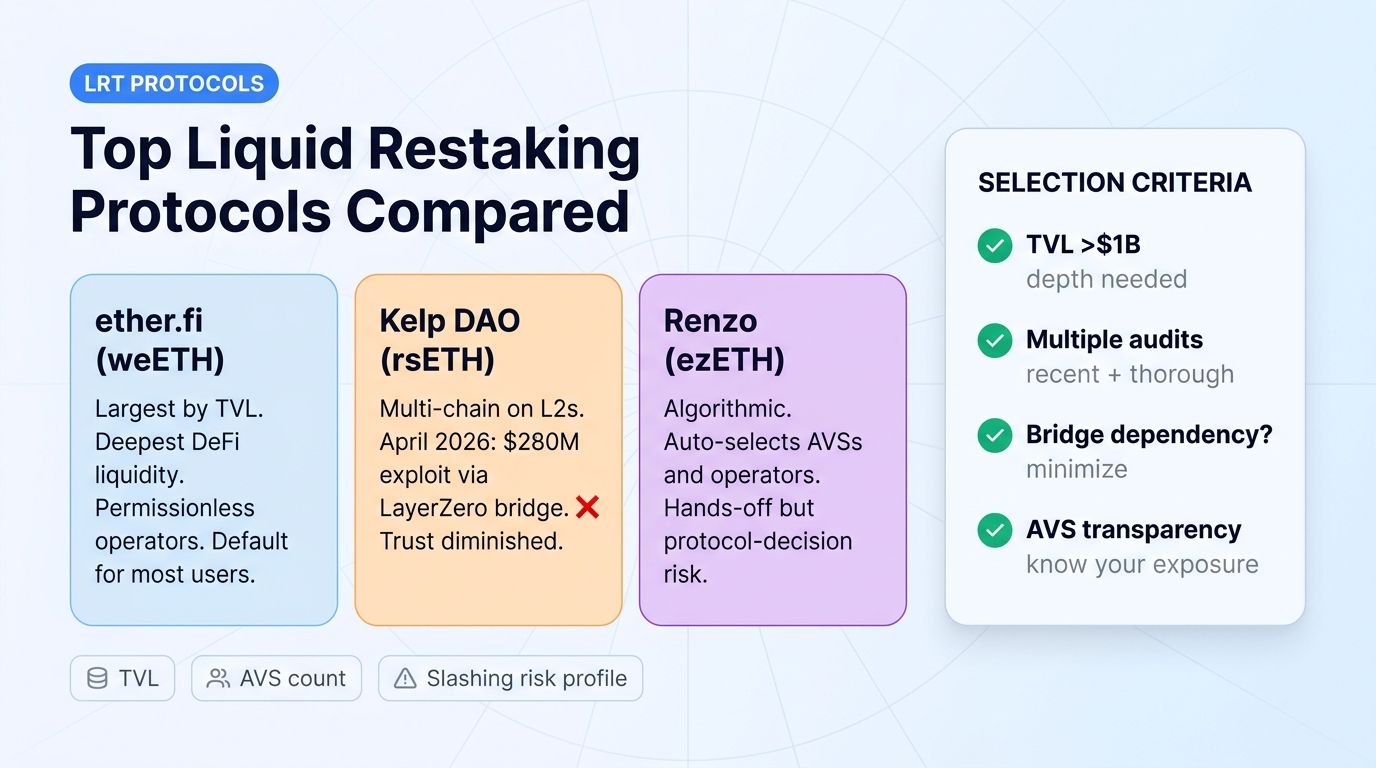

ether.fi (weETH) is the largest LRT by TVL. The protocol uses a permissionless node operator model and has the deepest DeFi liquidity. weETH is accepted as collateral on more lending platforms than any other LRT.

Kelp DAO (rsETH) focused on multi-chain availability, bridging rsETH to Ethereum Layer 2 networks. In April 2026, Kelp suffered a $280-293M exploit via a LayerZero bridge vulnerability, demonstrating that bridge dependencies are real risk for LRTs.

Renzo (ezETH) runs an algorithmic, hands-off model. The protocol automatically selects AVSs and operators. Users get hands-off exposure but accept protocol-decision risk.

Other LRTs (Puffer, Eigenpie, Swell) compete on specific features. For most retail users in 2026, ether.fi, Kelp, and Renzo cover the practical options.

When you hold an LRT, you are exposed to: - The LRT protocol's contracts - EigenLayer's contracts - The AVSs the LRT delegates to - The operators running those AVSs - Any bridges if the LRT moves cross-chain

This layered structure is the reason LRT yields are higher than base ETH staking, and the reason the risks compound.

How to Access EigenLayer Restaking

Three paths.

Path 1: Restake directly via EigenLayer interface. Connect a wallet to app.eigenlayer.xyz. Deposit ETH or wrapped staking tokens (stETH, rETH). Choose operators. Choose AVSs. Manage delegations. This path gives you the most control but requires understanding the AVS landscape and active management.

Path 2: Use a liquid restaking protocol. Deposit ETH on ether.fi, Kelp, or Renzo. Receive the LRT (weETH, rsETH, ezETH). The protocol handles operator selection, AVS choice, and reward distribution. This is the simplest path and what most users choose.

Path 3: Buy an LRT on a DEX. Major LRTs trade on Uniswap, Curve, and similar venues. You can buy with USDC or other stablecoins. Skip the deposit step but pay slippage and may trade at a small discount or premium to NAV.

For traders managing positions across multiple venues, the LRT layer typically lives in DeFi (self-custody wallets and DeFi protocols), while CEX-based positions are managed separately through a multi-exchange trading platform like Altrady that integrates with 19+ exchanges.

The Risks of EigenLayer Restaking

Slashing risk. AVSs define their own slashing conditions. An operator's misbehavior can drain a portion of restaked ETH. Some AVSs have aggressive slashing (10-100% of stake at risk for certain offenses).

Smart contract risk, layered. Holding an LRT exposes you to bugs in the LRT protocol, the EigenLayer protocol, and every AVS your stake is delegated to. The Kelp exploit in April 2026 (via LayerZero bridge) demonstrated that even non-EigenLayer contracts in the stack can be the failure point.

Operator risk. Operators run the actual validation software. A buggy operator, a malicious operator, or one with insufficient infrastructure can trigger slashing across multiple AVSs at once.

AVS quality risk. Not all AVSs are well-designed. Some have poorly-specified slashing conditions, low security budgets, or insufficient testing. LRT protocols that aggressively chase yield by validating poorly-designed AVSs put restakers at risk.

Withdrawal queue risk. Restaking withdrawals go through EigenLayer's escrow period (typically 7-14 days) plus the LRT protocol's internal queue. In a stressed market, exits can be slow or temporarily unavailable.

LRT depeg risk. LRTs can trade at a discount to NAV during stressed markets. A 5-10% depeg is not unusual when liquidations cascade through DeFi.

How EigenLayer Fits Into an ETH Holder Portfolio

A practical framework for ETH holders considering restaking:

- Base ETH (cold storage): 30-50% of ETH allocation. No yield, maximum security.

- Standard liquid staking (stETH from Lido): 30-50%. Modest yield (3-4% APY), strong DeFi composability, lower risk than restaking.

- Liquid restaking (weETH, rsETH, ezETH): 10-30%. Higher yield (6-12% APY typical), accept layered risks.

- Aggressive restaking strategies (LRT loops, leveraged positions): 0-10%. Only if you understand liquidation cascades.

After the Kelp exploit in April 2026, many traders reduced LRT exposure to single-digit percentages of total ETH allocation, treating restaking as one of the more aggressive corners of DeFi rather than a default holding strategy.

FAQ

What is the difference between staking and restaking?

Staking commits ETH to validate Ethereum, earning 3-4% APY. Restaking extends that staked ETH to also validate additional services (AVSs) on top of Ethereum, earning AVS rewards on top of the base staking yield. Restaking adds yield and adds slashing exposure.

Are EigenLayer rewards paid in ETH?

It depends on the AVS. Some AVSs pay in their own native token. Others pay in ETH or stablecoins. The composition of rewards across all the AVSs your stake is delegated to determines your effective yield. LRT protocols typically present a unified yield figure that bundles all reward types.

What is an AVS?

An Actively Validated Service is a network or middleware that uses EigenLayer's restaking to bootstrap security. Examples include data availability layers (EigenDA), oracle networks, cross-chain bridges, shared sequencers, and various middleware. AVSs pay restakers for borrowed security.

How does slashing actually work?

Each AVS defines specific bad behaviors that trigger slashing. If an operator commits one of these behaviors (signing conflicting messages, going offline, validating fraudulent data, etc.), EigenLayer can slash a percentage of the restaked ETH delegated to that operator. The exact percentage depends on the AVS and the offense.

Can I use EigenLayer on Altrady?

Altrady focuses on centralized exchange integration across 19+ exchanges. EigenLayer restaking and LRT positions typically live in self-custody wallets on DeFi protocols. For DeFi-native restaking management, you use a wallet (MetaMask, Rabby) and the relevant LRT protocol interface. CEX-listed wrapped versions of LRTs, where available, can be tracked through Altrady alongside other crypto holdings.

Conclusion

EigenLayer changed the math of Ethereum staking. By turning staked ETH into a tradable security resource, the protocol created an entirely new layer of crypto infrastructure. The AVS economy, the LRT layer, and the broader restaking ecosystem all flow through EigenLayer's primitive.

For traders and investors, the practical takeaway is this: EigenLayer is the infrastructure protocol behind the liquid restaking tokens you may already hold or be considering. Understanding how restaking actually works, including the slashing conditions, operator risks, and AVS dependencies, lets you make informed decisions about which LRT products to use and how much capital to allocate.

The restaking economy will continue to grow as more AVSs launch and more capital flows through EigenLayer-based products. The traders who understand the protocol's mechanics, not just the marketing yield numbers, will navigate the next two years of restaking with fewer surprises than those who treat LRTs as simple yield products.