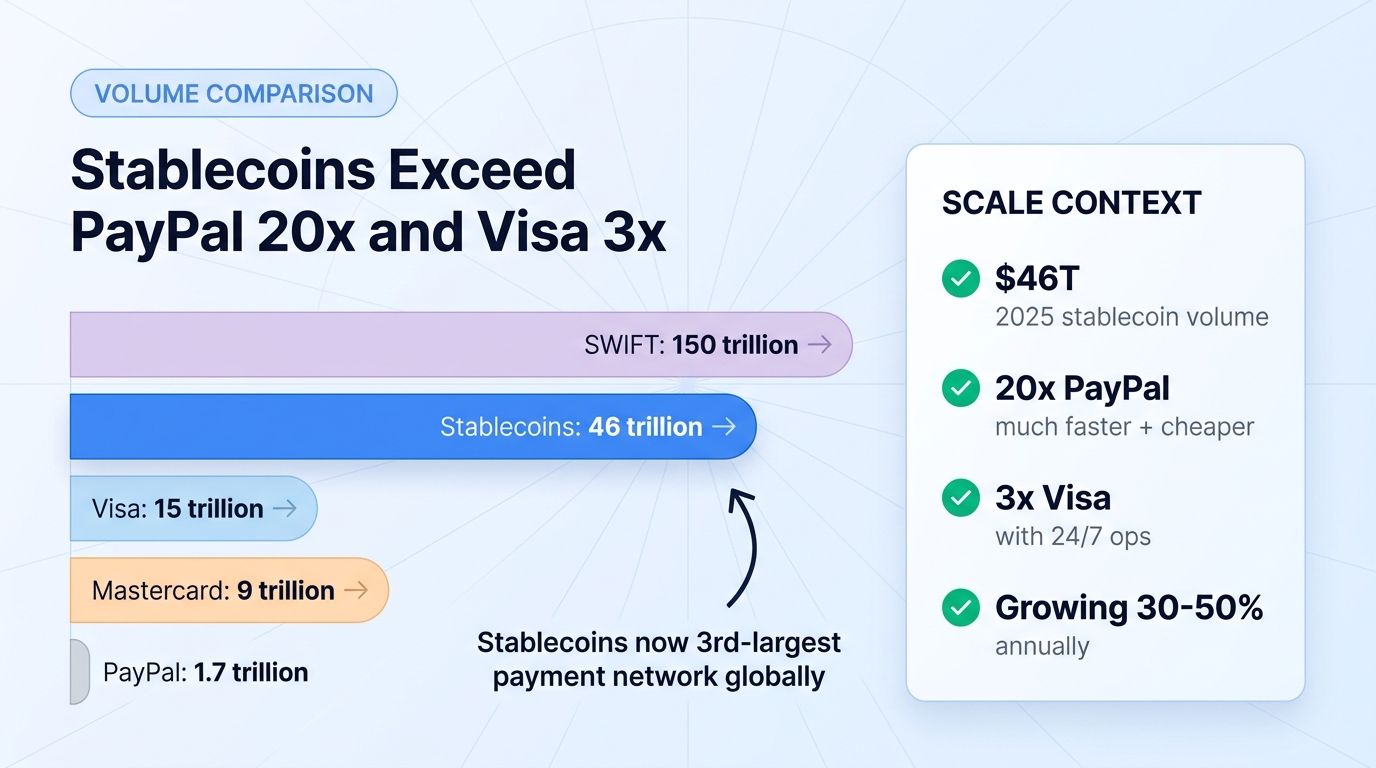

In 2025, stablecoins processed approximately $46 trillion in transaction volume. That's more than 20 times the annual volume of PayPal and roughly 3 times the volume of Visa. Yet most retail users and even many crypto traders don't perceive stablecoins as the dominant payment infrastructure they have become.

The thesis that "stablecoins are the internet's dollar" has moved from a16z prediction to operational reality. By 2026, stablecoins are not just a yield-bearing asset class or a trading pair convenience , they are foundational financial infrastructure being adopted by enterprises, governments, and consumers globally.

This guide explains how stablecoins became a $46 trillion infrastructure layer, the structural advantages over traditional payment rails, the major stablecoin categories, the regulatory framework that enabled the growth, and what 2026's adoption curve means for traders.

What Is the $46 Trillion?

The $46 trillion figure represents total annual on-chain stablecoin transfer volume across major networks (Ethereum, Tron, Solana, Polygon, BSC, others) in 2025. This includes all categories of stablecoin transactions: trading on DEXs, peer-to-peer transfers, payments to merchants, treasury operations, remittances, and DeFi protocol interactions.

For context, traditional payment networks compared on the same basis:

- PayPal: ~$1.7 trillion annual volume

- Visa: ~$15 trillion annual volume

- Mastercard: ~$9 trillion annual volume

- SWIFT: ~$150 trillion (large interbank settlements)

Stablecoins at $46 trillion exceed PayPal by 20x and Visa by 3x on transaction volume. They do not yet match SWIFT's interbank settlement role, but they have moved beyond pure crypto-trading utility into mainstream payment infrastructure.

How Stablecoins Became Infrastructure

Three structural forces converged.

Force 1: Settlement Speed and Cost

Traditional payment rails settle in days (ACH) or hours (faster rails). International wire transfers can take 1-5 business days. Stablecoin transfers settle in minutes (Ethereum) or seconds (Solana, Tron). At fractions of a cent per transaction on optimized networks.

For high-frequency commercial use cases (treasury operations, B2B payments, remittances), the speed and cost advantage compounds. Companies running treasury operations save substantially by moving from traditional rails to stablecoin rails.

Force 2: 24/7 Operations

Traditional payment networks have business-hour limitations. Settlement windows close on weekends and holidays. Stablecoin networks operate 24/7/365 without exception. For global businesses operating across time zones, the always-on availability is itself a competitive advantage.

Force 3: Regulatory Clarity

The major shift came in 2025-2026 with regulatory clarity in the US (CLARITY Act stablecoin provisions), EU (MiCA framework), and other jurisdictions. Once enterprises could integrate stablecoins with clear legal status, adoption accelerated rapidly.

The combination of speed, cost, availability, and regulatory clarity moved stablecoins from "crypto trading convenience" to "payment infrastructure" in a single 24-month window.

The Major Stablecoin Categories

By 2026, the stablecoin landscape has matured into distinct categories.

Fiat-Backed Stablecoins (USDC, USDT, PYUSD)

The largest category. Backed 1:1 by cash and short-duration Treasury reserves. Major issuers include Circle (USDC), Tether (USDT), PayPal (PYUSD), and others. Combined market cap exceeds $300 billion.

Used for: trading pairs, treasury operations, payments, remittances.

Yield-Bearing Stablecoins (USDY, USDe, sUSDS)

Stablecoins that pass Treasury yield through to holders. Ondo USDY, Ethena USDe, Sky sUSDS, and others. Combined market cap in the tens of billions.

Used for: idle dollar yield, treasury cash management, alternative to bank deposits.

Algorithmic Stablecoins (DAI, FRAX, others)

Decentralized stablecoins backed by crypto collateral or algorithmic mechanisms rather than fiat reserves. Smaller market share but important for DeFi composability.

Used for: DeFi protocol integration, decentralization-focused users.

Central Bank Digital Currencies (CBDCs)

Sovereign stablecoins issued by central banks. China's digital yuan is the most-deployed example. Most other major economies are in research or pilot phases.

Used for: government-backed digital cash, monetary policy implementation.

Tokenized Bank Deposits

Some banks (JPMorgan's JPM Coin, others) issue tokenized representations of bank deposits. Function as private stablecoins for institutional clients.

Used for: institutional liquidity management, interbank settlement.

The 2026 Use Cases

Stablecoin adoption has expanded across multiple use cases.

Use Case 1: Cross-Border Remittances

Workers sending money home no longer rely exclusively on Western Union or bank wires. Stablecoin remittances cost $0.10 to $1 per transaction versus $15-50 for traditional rails. Settlement in minutes versus days.

Major remittance corridors (US to Mexico, Gulf to South Asia, Europe to Africa) have meaningfully shifted toward stablecoin rails.

Use Case 2: Enterprise B2B Payments

Companies paying suppliers internationally, settling cross-border invoices, or managing global treasury operations use stablecoins for cost and speed advantages. Major enterprise software platforms (SAP, Oracle, others) are integrating stablecoin payment options.

Use Case 3: Merchant Payments

Crypto-friendly merchants accept stablecoins via Lightning Network, Solana Pay, and similar payment infrastructure. The merchant pays effectively 0% in fees compared to 2-3% for credit cards.

Use Case 4: Treasury Cash Management

Corporate treasuries holding excess cash use yield-bearing stablecoins as an alternative to short-duration Treasuries or money market funds. The yield is competitive, and the on-chain liquidity is superior.

Use Case 5: DeFi Protocol Liquidity

DeFi lending, AMMs, derivatives, and other protocols depend on stablecoin liquidity. Hundreds of billions in stablecoins sit in DeFi protocols generating yield, providing liquidity, or collateralizing positions.

Use Case 6: Personal Savings (Especially in High-Inflation Countries)

In countries with currency instability (Argentina, Turkey, Venezuela, others), residents use USD-pegged stablecoins as savings vehicles. Stablecoins effectively provide dollar access to populations whose banking systems make USD accounts difficult.

The Regulatory Framework

The regulatory clarity that enabled stablecoin adoption has three main pillars.

Pillar 1: Reserve Requirements

Stablecoin issuers must hold high-quality reserves (cash, short-duration Treasuries) at 1:1 with issued stablecoins. Monthly attestations and annual audits are required.

This protects holders from issuer insolvency while allowing issuers to earn yield on reserves.

Pillar 2: Issuer Licensing

Major stablecoin issuers must obtain specific licenses. Federal pathway in the US, MiCA-compliant pathway in EU, and equivalent frameworks in other major jurisdictions.

Licensing creates compliance overhead but provides legal certainty for institutional users.

Pillar 3: Yield Distribution Rules

Per the CLARITY Act compromise, issuers can share yield through related activities (trading rebates, fee waivers, loyalty programs) but cannot pay interest solely for holding.

This preserves the bank-deposit distinction while allowing innovation in yield delivery.

The Players Driving Adoption

Several categories of organizations are driving the $46 trillion volume.

Stablecoin Issuers

Circle (USDC), Tether (USDT), and PayPal (PYUSD) dominate the fiat-backed category. Ondo, Ethena, Sky, and others lead yield-bearing innovations.

Payment Infrastructure

Stripe, Visa, Mastercard, and other payment networks are integrating stablecoin rails. Visa's stablecoin settlement pilot processes billions in monthly volume.

Enterprise Treasuries

Companies including BlackRock, MicroStrategy (Strategy), Bitmine, and others hold significant stablecoin positions for treasury operations.

Banks and Financial Institutions

Major banks (JPMorgan, BNY Mellon, Standard Chartered) operate stablecoin services or tokenized deposit products.

Remittance Companies

Western Union, MoneyGram, Wise, and Remitly have integrated stablecoin settlement to compete with crypto-native remittance services.

What This Means for Crypto Traders

Three practical implications.

Implication 1: Trading Infrastructure Improvements

Stablecoin liquidity on major exchanges and DEXs has compounded. Trading USDC/BTC pairs has tighter spreads than 2-3 years ago. Cross-exchange arbitrage is faster as stablecoins move between venues nearly instantly.

For active traders, the improved liquidity directly translates to better execution. A platform like Altrady (connecting to 19+ exchanges) makes use of this improved stablecoin liquidity by enabling unified position management across venues.

Implication 2: Yield Opportunities Expanded

Idle stablecoin balances now have multiple yield options:

- Yield-bearing stablecoins (USDY, USDe, sUSDS): 4-10% APY

- DeFi lending (Aave, Compound, others): variable yields

- Tokenized Treasury platforms (Ondo, BUIDL): institutional-grade yields

- Centralized yield products (where regulated): variable yields

The 0% bank-deposit alternative is no longer acceptable for trading capital. Stablecoin yield is competitive with money market funds while offering 24/7 liquidity.

Implication 3: Reduced FX Friction

Trading across multiple fiat currencies historically incurred significant FX costs. Stablecoins (especially USD-pegged) eliminate intra-day FX cost for trading purposes. Traders can move USDC between Asian, European, and American exchanges instantly without FX fees.

The Risks and Considerations

Issuer risk. Stablecoin value depends on the issuer's solvency and operations. Diversify across multiple stablecoins (USDC + USDT + others) rather than concentrating in one.

Regulatory risk. While regulatory clarity has improved, future regulatory changes could affect specific stablecoins. Issuers in less-regulated jurisdictions face more risk than US/EU-licensed alternatives.

Smart contract risk. Yield-bearing stablecoins involve smart contract risk. Bugs or exploits could affect token value.

De-peg risk. Despite mature design, stablecoins have de-pegged historically (UST 2022, Tether briefly during banking stress). The risk has decreased with regulatory clarity but is not zero.

Concentration risk. USDC + USDT together account for the majority of stablecoin volume. Concentration in two issuers creates systemic risk if either faces operational issues.

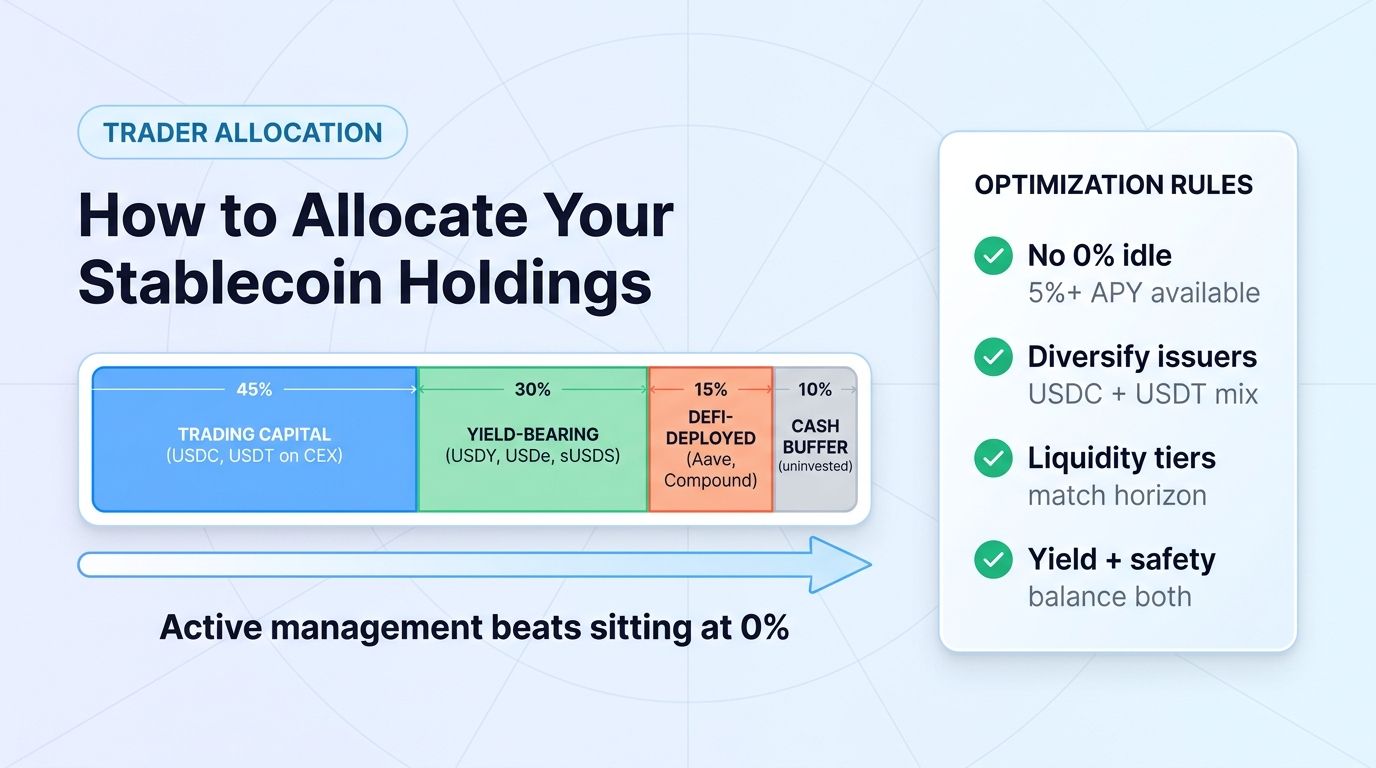

How to Position Stablecoin Allocation

A practical framework:

- Active trading capital (USDC, USDT on CEXs): 30-50%. Immediate availability for trades.

- Yield-bearing reserve (USDY, USDe, sUSDS): 20-40%. Earn 5%+ APY on capital waiting for opportunities.

- DeFi-deployed stablecoins (Aave, Compound, others): 10-20%. Variable yield with DeFi exposure.

- Cash buffer (uninvested stablecoins): 5-15%. Liquidity for opportunistic deployment.

Most professional traders hold significant stablecoin positions as part of normal portfolio management. The $46 trillion infrastructure thesis is supported by individual traders' allocation decisions in aggregate.

The Longer-Term Trajectory

Three structural trends to watch through 2027-2028.

Trend 1: Continued Volume Growth

If 2025 volume was $46 trillion and growth continues at 30-50% annually, stablecoins could exceed Visa volume (~$15 trillion) by 2027 and approach SWIFT volume by 2030.

Trend 2: CBDC Integration

Central bank digital currencies will integrate with private stablecoins, creating hybrid public-private digital cash infrastructure. The interoperability layer is being built in 2026-2027.

Trend 3: AI Agent Settlement

AI agents conducting autonomous transactions (per the Ethereum Foundation's framing) will primarily use stablecoins for settlement. The agent economy is being built on stablecoin rails.

FAQ

What's the difference between USDC and USDT?

Both are USD-pegged stablecoins backed primarily by Treasuries. USDC (issued by Circle) is US-licensed with more transparent reserves and US-regulated. USDT (issued by Tether) is offshore-licensed with somewhat less transparent reserves but larger market cap. Both have strong track records.

Is it safe to hold large amounts in stablecoins?

For short-term operational use (weeks to months), yes. Major regulated stablecoins (USDC, PYUSD) have strong reserve backing and regulatory oversight. For longer-term storage, diversifying across multiple stablecoins and using yield-bearing options reduces single-issuer risk.

Why are stablecoin transactions cheaper than Visa?

Stablecoin transactions on optimized networks (Solana, Tron, Polygon) cost fractions of a cent because the network operations are highly efficient and the protocols don't extract the 2-3% spread that credit card networks do. The cost structure is fundamentally different.

Can I use stablecoins for payments to merchants?

Increasingly yes. Solana Pay, Lightning Network, Stripe stablecoin integration, and other payment infrastructure now support stablecoin payments at major merchants. The adoption is uneven but growing rapidly.

Can I manage stablecoin positions on Altrady?

Yes. Altrady connects to 19+ exchanges that support major stablecoins (USDC, USDT, DAI, others). You can manage stablecoin positions alongside other crypto holdings, use the DCA bot or grid bot for stablecoin-based strategies, and view your full portfolio in one dashboard.

Conclusion

The $46 trillion stablecoin transaction volume in 2025 marks an inflection point in financial infrastructure. Stablecoins have moved from "crypto trading convenience" to "internet's dollar" , payment infrastructure that exceeds PayPal by 20x and Visa by 3x on volume.

For traders, the practical takeaway is this: stablecoins are no longer an asset class to ignore between trades. They are infrastructure that affects trading efficiency, yield opportunities, FX management, and broader portfolio construction. Optimizing your stablecoin positioning (which stablecoins, which yields, which networks) is now a meaningful component of overall returns.

The longer-term trajectory suggests stablecoins will continue scaling. Volume growth, CBDC integration, AI agent settlement, and continued regulatory clarity all point toward stablecoins capturing more of global payment volume over the next 5 years. The companies and protocols that build on stablecoin infrastructure are positioning for one of the most significant financial infrastructure shifts in decades.

The thesis "stablecoins are the internet's dollar" was a prediction in 2024. By 2026, it is an observation of operational reality. The next decade will determine how far that reality extends , and which networks, issuers, and platforms capture the resulting value.