Tokenized stocks are easy to describe and hard to make useful. Issuing a token that represents an equity exposure is only the first step. The harder step is building secondary markets where users can trade with real liquidity, legal clarity, and operational reliability.

That is why the Securitize, Jump Trading Group, and Jupiter announcement matters. The May 2026 launch brought together regulated infrastructure, institutional liquidity, and a user-facing DeFi interface for tokenized equities. It is a useful case study in what the next phase of RWA markets may require.

Why Issuance Is Not Enough

A tokenized equity can exist onchain but still be difficult to trade. If there are few buyers, wide spreads, limited transferability, or heavy compliance friction, the token exists but behaves like an illiquid wrapper. The user gets blockchain representation without the practical benefit of a strong market.

Secondary liquidity is the bridge between a tokenized asset and a useful trading product. It determines whether users can enter, exit, price, and transfer exposure in a way that feels closer to a real market.

- Issuance creates the token.

- Liquidity creates usable markets.

- Compliance defines who can hold and trade.

- Market makers help tighten spreads.

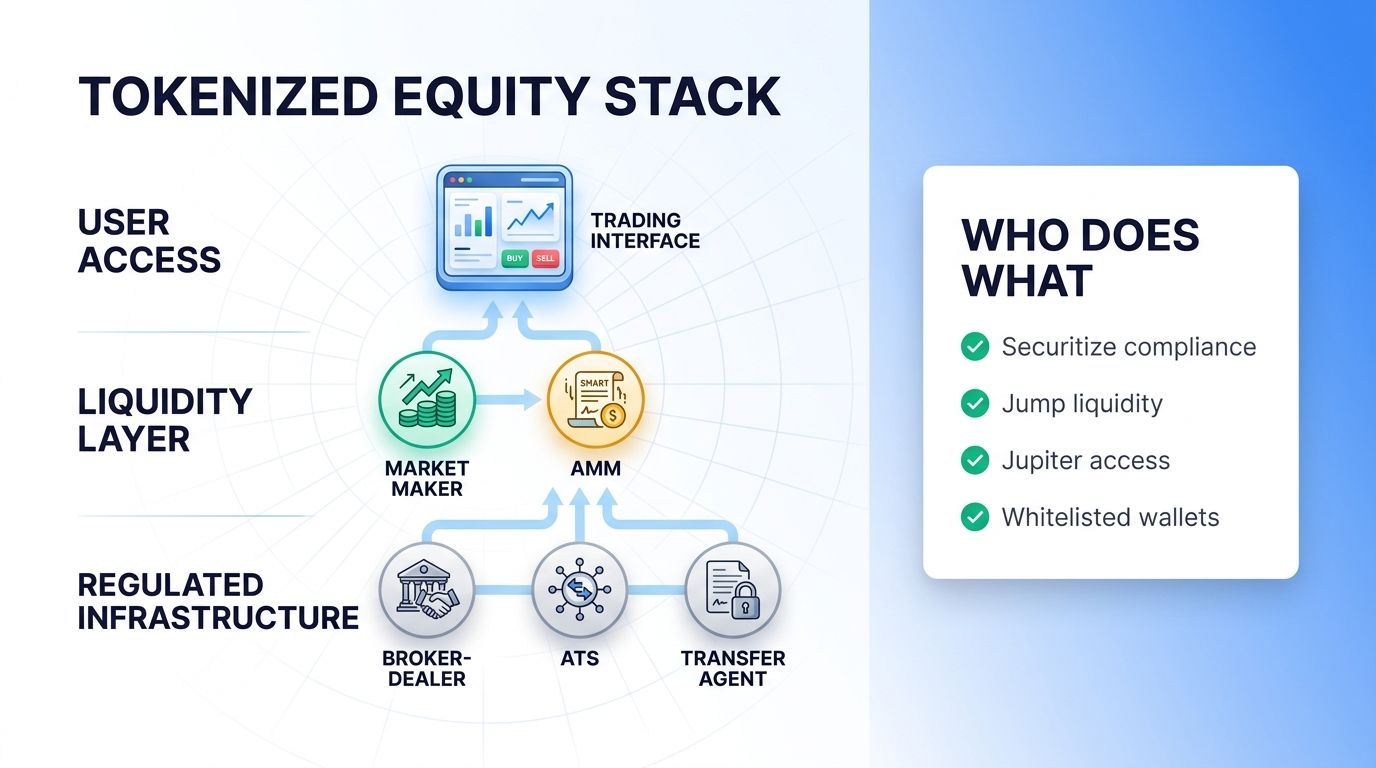

The Securitize, Jump, and Jupiter Stack

The announced stack divides responsibilities. Securitize provides regulated broker-dealer, alternative trading system, transfer agent, and whitelisted-wallet infrastructure. Jump provides liquidity through its PropAMM deployed on Solana. Jupiter provides the user-facing access point for discovery and trading.

This division is important because tokenized securities need more than a smart contract. They need legal ownership records, compliance gates, liquidity, routing, custody workflows, and user experience. The stack approach shows how tokenized equity trading may look less like one app and more like coordinated infrastructure.

- Securitize handles regulated market infrastructure.

- Jump supports liquidity and price discovery.

- Jupiter provides user-facing access.

- Whitelisted wallets help enforce compliance rules.

What Traders Should Watch

Tokenized equity markets should be judged by trading quality, not only announcement size. Useful signals include spread width, daily volume, number of eligible assets, holder growth, redemption mechanics, wallet eligibility, and whether liquidity remains healthy during volatile equity sessions.

Traders should also ask whether the asset is legally recognized, who maintains shareholder records, what jurisdictions are supported, and whether tokens can move freely or only among approved wallets. Those details decide whether the product is a real market or a limited pilot.

- Watch spreads and daily volume.

- Check transfer restrictions and wallet rules.

- Review redemption and ownership mechanics.

- Compare onchain liquidity with traditional market depth.

The Main Risks

Tokenized equities sit at the intersection of securities law, smart contract risk, custody, and market liquidity. A product can be technically impressive but still hard to access, limited by jurisdiction, or thinly traded. Traders need to treat these assets differently from ordinary crypto tokens.

The biggest risk is assuming that onchain equals liquid. A token may settle quickly but still have few active buyers. It may be legally compliant but limited to whitelisted users. It may track a real equity but trade differently after market hours.

- Compliance rules can limit access.

- Liquidity may be thin outside core assets.

- After-hours pricing can diverge from reference markets.

- Smart contract and custody risk still exist.

Why Secondary Markets Are the Real Test

Tokenized equities have already proven that assets can be represented onchain. The real test is whether those assets can support the behavior that traders expect from markets: quotes, depth, routing, compliance, settlement, and reliable ownership records. Without that, tokenization is mostly a wrapper.

Secondary markets matter because users need confidence that they can exit. A tokenized stock that trades only inside a narrow venue, with limited participants and wide spreads, may be useful for experimentation but not for serious allocation. Liquidity is what turns access into a market.

The Securitize, Jump, and Jupiter approach is notable because it recognizes that no single layer solves the whole problem. Regulated infrastructure, market-making, and user access have to work together. If one layer is weak, the experience can break.

- Issuance proves representation.

- Secondary trading proves usefulness.

- Liquidity needs market makers and participants.

- Compliance must be built into transfer rules.

How Tokenized Equities Could Affect Crypto Markets

If tokenized equities become liquid, they can change what crypto users trade onchain. Instead of leaving crypto rails to access traditional assets, users may hold stablecoins, tokenized stocks, and crypto positions in a more connected portfolio. That can increase demand for routing, custody, risk tools, and onchain execution.

The market impact may not flow to every token equally. Some value may accrue to regulated issuers. Some may accrue to liquidity providers. Some may accrue to the chains that host settlement. Some may accrue to wallets and interfaces that make the experience usable. Traders need to map the value chain rather than assume one obvious winner.

There is also a timing issue. Tokenized equity markets may grow in regulated pockets before becoming broadly accessible. That can make the theme important before it becomes easy to trade directly.

- Watch the full value chain.

- Separate issuer value from chain value.

- Track liquidity providers and interfaces.

- Expect gradual access expansion.

FAQ

What are tokenized equities?

They are blockchain-based representations of equity exposure or ownership records, subject to the structure and jurisdiction of the product.

Why is secondary liquidity important?

It determines whether users can enter and exit positions with reasonable spreads and reliable price discovery.

What did Securitize, Jump, and Jupiter launch?

They announced a regulated onchain trading stack for tokenized equities with compliance infrastructure, liquidity, and user access layers.

Are tokenized equities the same as normal crypto tokens?

No. They involve securities rules, transfer restrictions, ownership records, and different market risks.