In May 2026, the US Securities and Exchange Commission was expected to release the Innovation Exemption framework that would enable tokenized stocks to trade on crypto-native platforms with lighter regulatory requirements. The framework, championed by SEC Chair Paul Atkins, would have allowed publicly traded stocks like Apple, Tesla, and Nvidia to trade as blockchain tokens around the clock, in fractional sizes, with near-instant settlement.

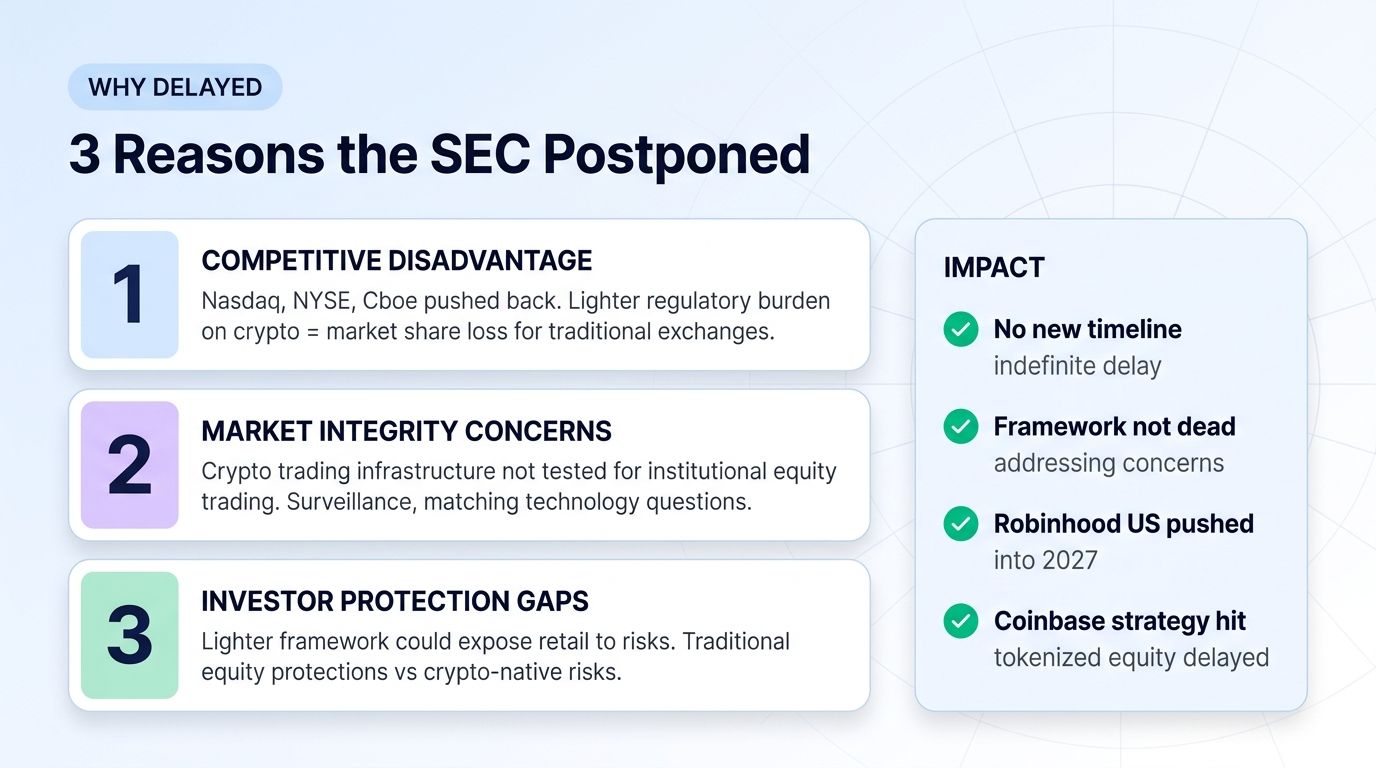

Then it didn't happen. On May 26, 2026, the SEC abruptly delayed the release after closed-door meetings in which Nasdaq, NYSE, and Cboe leadership pushed back hard on the proposed framework. As of late May 2026, there is no new timeline. Robinhood and Coinbase, both of which built US tokenized-equity product roadmaps assuming the exemption would ship in 2026, now face base-case launches pushed into 2027.

For traders watching the convergence of crypto and traditional finance, this delay matters. Tokenized stocks represent one of the most consequential potential expansions of crypto market access, and the regulatory uncertainty creates both risk and opportunity.

This guide explains what tokenized stocks are, the SEC's Innovation Exemption framework, why traditional exchanges pushed back, the impact on Robinhood and Coinbase's plans, the existing $1.4 billion tokenized stock market, and what traders should think about the delayed launch.

What Are Tokenized Stocks?

Tokenized stocks are blockchain tokens that represent ownership in publicly traded equities. Each token corresponds to a share (or fractional share) of a specific publicly traded company. The tokens trade on blockchain networks rather than traditional stock exchanges, offering specific advantages over conventional equity trading.

The structural advantages include:

24/7 trading: Traditional stock markets operate during business hours (9:30am-4:00pm ET for US exchanges). Tokenized stocks trade continuously across global time zones.

Fractional sizes: Buy 0.001 shares of a $500 stock. Traditional brokerages have moved toward fractional shares but tokenized stocks make sub-fractional trading native.

Near-instant settlement: Traditional equity settlement is T+1 (one business day). Tokenized stocks settle in minutes or seconds.

Cross-border accessibility: Tokenized stocks can be accessed globally via crypto wallets, removing geographic restrictions that limit traditional equity access.

Programmable composability: Tokenized stocks can be used as collateral in DeFi, programmed into smart contract systems, or combined with other onchain instruments.

The trade-off is regulatory uncertainty and operational complexity. Tokenized stocks operate in regulatory gray areas in most jurisdictions, which has been the primary barrier to mainstream adoption.

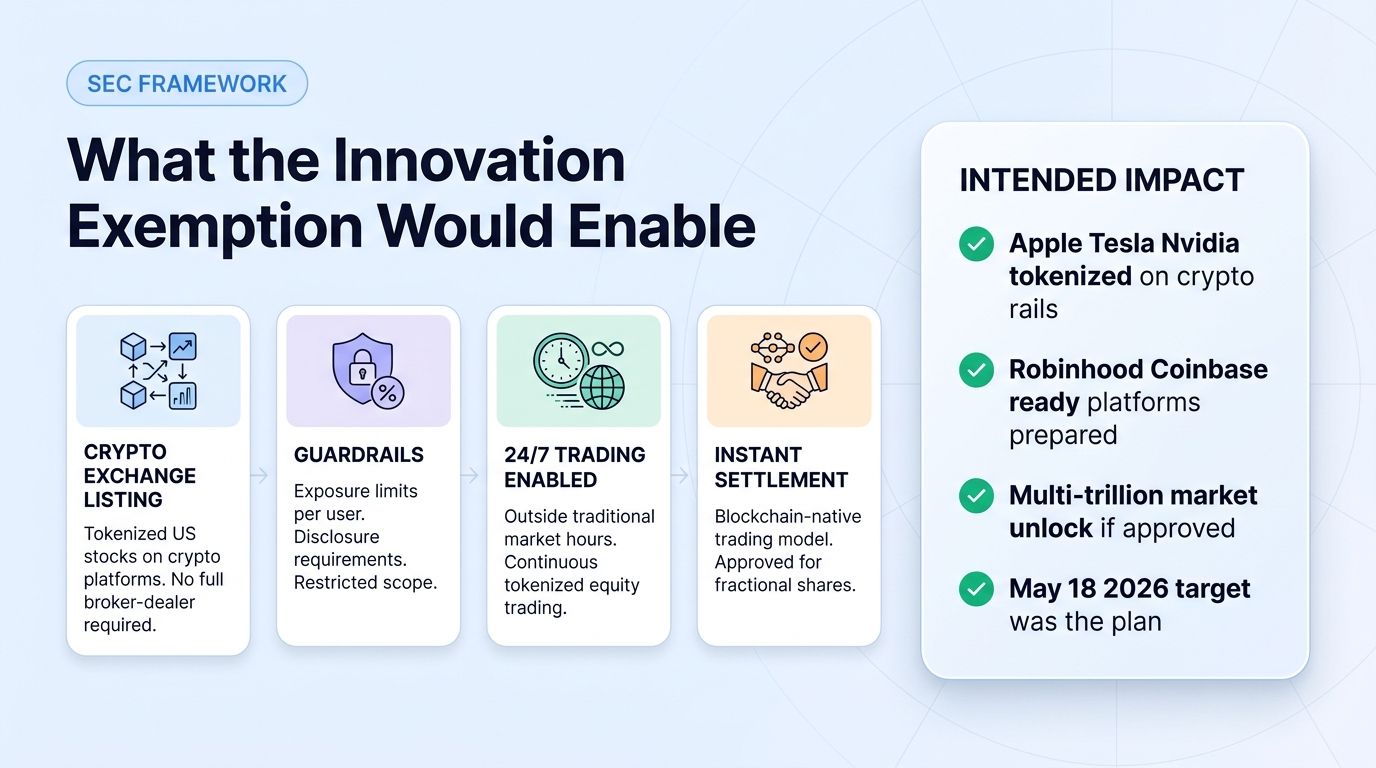

The SEC Innovation Exemption Framework

The proposed Innovation Exemption framework, championed by SEC Chair Paul Atkins through early 2026, would have provided regulatory clarity for tokenized stock trading on crypto-native platforms.

The framework was designed to:

Allow crypto exchanges to list tokenized stocks: Without requiring full broker-dealer or exchange licenses, crypto platforms could offer tokenized US equities to their users.

Set guardrails: Exposure limits per user, disclosure requirements, restrictions on which stocks could be tokenized, and temporal limits on the exemption.

Enable 24/7 trading: The framework would allow tokenized stocks to trade outside traditional market hours.

Allow fractional and instant settlement: The blockchain-native trading model would be permitted.

Maintain investor protections: Standard anti-fraud and disclosure requirements would apply.

The framework was widely seen as enabling Robinhood and Coinbase to launch US tokenized-equity products without overhauling their regulatory structures. The May 18, 2026 target release date had been telegraphed for months.

Why the Delay Happened

The delay was driven by significant pushback from incumbent exchanges. The closed-door meetings on the framework included leadership from Nasdaq, NYSE, and Cboe, who voiced strong opposition.

The incumbents' arguments centered on three themes.

Competitive disadvantage: If crypto platforms could trade tokenized stocks 24/7 with lighter regulatory burdens, traditional exchanges would lose market share without commensurate regulatory parity.

Market integrity concerns: Incumbents argued that crypto-native trading infrastructure had not been tested for institutional-grade equity trading. Order matching, price discovery, and surveillance technology at crypto platforms might be insufficient.

Investor protection gaps: The framework's lighter regulatory burden could expose retail investors to risks (manipulation, technical failures, custody issues) that traditional equity trading has guarded against.

The SEC postponed the release to address these concerns, though no specific timeline has been provided. The delay does not mean the framework is dead, but it does represent a significant setback for the tokenized stocks narrative.

The Existing $1.4 Billion Tokenized Stock Market

Despite the lack of US regulatory clarity, a tokenized stock market exists globally. By Q2 2026, the onchain tokenized stock market exceeded $1.4 billion in cumulative tokenized value.

Major participants include:

Backed Finance: Swiss-regulated issuer of tokenized stocks. Tokens represent shares in major US and European publicly traded companies. Tradable on DeFi protocols and select exchanges.

Robinhood (EU): Offers tokenized US stocks to European users through its EU subsidiary. Uses Arbitrum as the underlying blockchain. Has been operating since 2024-2025.

Backed bTokens: Tokenized versions of US stocks, ETFs, and other equity products. Compliant with Swiss MiCA framework.

Dinari: US-regulated platform offering tokenized stocks under existing securities frameworks. More restrictive than the proposed Innovation Exemption would be.

The existing market demonstrates that demand for tokenized stocks is real. The Innovation Exemption framework, if eventually approved, would significantly expand US-accessible tokenized equity trading.

The Impact on Robinhood and Coinbase

Both Robinhood and Coinbase had built tokenized-equity product roadmaps assuming the Innovation Exemption would launch in 2026. The delay materially affects their strategic plans.

Robinhood: Already operates tokenized stocks in Europe through its EU subsidiary. US launch was expected in mid-late 2026. With the delay, US launch pushes into 2027 at earliest. The Robinhood Crypto+ vision (combining crypto and traditional equity trading on a single platform) is delayed.

Coinbase: Has been preparing tokenized equity infrastructure as part of its broader institutional financial services expansion. The delay affects Coinbase's competitive positioning against traditional brokerages and Robinhood.

For both, the strategic implications include:

- Continued reliance on existing crypto-only revenue

- Potential regulatory arbitrage by competitors operating in other jurisdictions

- Slower path to becoming a unified crypto+traditional finance platform

- Potential strategic pivots toward other crypto-native opportunities

How Crypto Traders Should Think About the Delay

For traders, the delay creates several considerations.

Existing tokenized stock markets remain accessible: European Robinhood, Backed Finance products, and DeFi-native tokenized stock protocols continue operating. Traders seeking tokenized stock exposure have options outside the US Innovation Exemption framework.

Coinbase and Robinhood stock prices may be affected: Both companies' equity valuations partly depend on the tokenized equity expansion narrative. The delay may create short-term price pressure on these stocks.

Crypto exchange tokens benefit from delay: COIN, HOOD-related crypto products, and crypto-exchange tokens may temporarily benefit if delay reduces competitive pressure on crypto-only offerings.

Tokenized RWA category broadly continues growing: Tokenized Treasuries (BUIDL, Ondo USDY) and tokenized credit continue expanding even without the stock-specific framework. The broader tokenization theme remains intact.

Regulatory framework arbitrage: Crypto platforms in other jurisdictions (Switzerland, EU, Singapore) may capture tokenized stock activity that would have gone to US platforms.

How Tokenized Stocks Compare to Other Tokenized Assets

The tokenized real-world asset (RWA) landscape has multiple categories at varying levels of maturity.

Tokenized US Treasuries ($15B+): Most mature category. BUIDL, Ondo USDY, Franklin FOBXX leading. Regulatory framework relatively clear.

Tokenized credit ($5-8B): Centrifuge, Maple, Goldfinch. Private credit + lending. Mature but smaller scale.

Tokenized commodities ($1-2B): Mostly gold (PAXG, XAUT). Established but slower-growing.

Tokenized real estate (growing): Lofty, Cityfunds, others. Fractional ownership platforms.

Tokenized stocks ($1.4B existing, much more potential): Largest potential market by far given US public equity market is ~$50 trillion. Regulatory clarity remains the bottleneck.

The tokenized stock category, if fully unlocked, could grow to multi-trillion dollar scale. This is why the Innovation Exemption framework matters and why the delay is significant.

How to Get Tokenized Stock Exposure

Three practical paths for now.

Path 1: Use Robinhood EU or similar non-US platforms. European Robinhood users can access tokenized US stocks. Other jurisdictions have similar options.

Path 2: Trade DeFi-native tokenized equity products. Backed Finance bTokens trade on DEXs and selected exchanges. Provides access without requiring traditional brokerage relationships.

Path 3: Trade equity-adjacent crypto exposure. Holdings in major crypto exchanges (COIN), payment companies (PYPL), and crypto-active asset managers provide adjacent exposure to the broader theme.

For US-based traders, direct US tokenized stock access remains limited until the Innovation Exemption framework launches.

The Risks of Tokenized Stock Investment

Regulatory risk. The biggest risk. Without clear US framework, US-based participants operate in uncertain regulatory environment. Future enforcement actions could affect products.

Custody risk. Tokenized stock tokens depend on issuer custody arrangements. Issues at the issuer (insolvency, operational failures) directly affect tokens.

Liquidity risk. Most tokenized stocks trade with thin liquidity compared to underlying equities. Large positions face significant slippage.

Tracking error. Tokenized stock prices may diverge from underlying equity prices, particularly during volatile periods or after-hours.

Counterparty risk. Tokenized stocks rely on multiple counterparties (issuer, custodian, exchange). Issues at any layer affect end users.

Tax complexity. Tokenized stock tax treatment varies by jurisdiction. May be treated as crypto, securities, or hybrid depending on local rules.

What to Watch in the Next 12 Months

Three indicators.

Indicator 1: SEC Innovation Exemption status. Does the SEC re-engage on the framework or remain stalled? Any forward progress signals tokenized stocks gaining traction.

Indicator 2: Non-US tokenized stock market growth. Does the European/Swiss tokenized stock market grow beyond current $1.4B? Strong growth signals genuine demand independent of US clarity.

Indicator 3: Robinhood/Coinbase strategic pivots. Do these companies pursue alternative tokenized equity strategies (international expansion, partnerships, regulatory arbitrage)? Innovation responses signal commitment to the category.

If all three trend positively, tokenized stocks emerge as a category despite the US setback. If progress stalls broadly, the category may remain niche for the next 2-3 years.

FAQ

What is the SEC Innovation Exemption framework?

The framework, championed by SEC Chair Paul Atkins, would have provided regulatory clarity for crypto platforms to offer tokenized US stocks. It included guardrails (exposure limits, disclosures) but was significantly less restrictive than full broker-dealer requirements. The framework was scheduled for release on May 18, 2026 but was delayed indefinitely after pushback from Nasdaq, NYSE, and Cboe.

Are tokenized stocks legal in the US?

Tokenized stocks operate in a complex US regulatory environment. Currently, most tokenized stock platforms either don't serve US users, operate under restrictive securities frameworks, or use offshore subsidiaries. The Innovation Exemption framework would have provided clearer US-accessible pathways.

Can I trade tokenized Apple, Tesla, or Nvidia stocks now?

Outside the US, yes. Robinhood EU, Backed Finance, and some other platforms offer tokenized versions of US stocks. For US-based users, direct tokenized equity access remains limited until US regulatory clarity emerges.

What is the difference between tokenized stocks and ETFs?

ETFs are traditional securities that trade on stock exchanges and hold underlying assets. Tokenized stocks are blockchain tokens that represent ownership in publicly traded companies, tradable 24/7 on crypto infrastructure. ETFs provide regulated, traditional access; tokenized stocks provide crypto-native, programmable access. They serve different use cases.

Can I trade tokenized stocks or related products on Altrady?

Most tokenized stocks trade on DeFi protocols or specialized crypto-equity platforms rather than traditional exchanges. Altrady connects to 19+ exchanges and supports unified crypto portfolio tracking. For tokenized stock access, you would use the platforms that issue them; for related crypto exposure (COIN, exchange tokens), Altrady provides full coverage.

Conclusion

The SEC Innovation Exemption delay represents one of the most consequential regulatory setbacks of 2026 for crypto's mainstream financial integration. The framework would have unlocked tokenized stock trading on crypto platforms, potentially creating a multi-trillion dollar opportunity over time.

For traders, the practical takeaway is this: tokenized stocks as a category remain alive globally but US access is delayed indefinitely. Existing non-US platforms continue operating, and DeFi-native tokenized stock products remain accessible.

The longer-term trajectory depends on the SEC eventually engaging with the framework constructively (or being forced to via political or market pressure), and on tokenized stock platforms in other jurisdictions demonstrating sufficient scale to make US delay costly.

For diversified crypto portfolios, exposure to the tokenization theme can come through tokenized Treasuries (BUIDL, Ondo), tokenized RWA tokens (ONDO and similar), or adjacent crypto positions (COIN, exchange tokens). Direct tokenized stock allocation makes sense only for traders comfortable with the regulatory uncertainty. The next 12-24 months will produce decisive data on whether the Innovation Exemption framework eventually launches and on whether the broader tokenized equity category establishes durable traction.