Real-world asset (RWA) tokenization grew from $5.5 billion in early 2025 to $29.2 billion by April 2026, a more than fivefold expansion in 16 months. The early growth was dominated by tokenized US Treasuries (USDY, BUIDL, OUSG, BENJI). But by mid-2026, the focus has shifted to a more ambitious category: real estate.

Tokenized real estate represents the on-chain version of one of the world's largest asset classes. The global real estate market is estimated at $300+ trillion, dwarfing the entire cryptocurrency market by orders of magnitude. Even capturing a small fraction of real estate exposure on-chain represents one of the most significant growth opportunities in crypto.

This guide explains what tokenized real estate is, the leading platforms in 2026, how the structures work, the regulatory considerations, and how traders can participate in the category as it scales.

What Is Tokenized Real Estate?

Tokenized real estate is the representation of property ownership (or claims on property cash flows) as blockchain tokens. The model has several variations.

Type 1: Direct property tokenization. Specific properties are placed in a legal structure (typically an LLC or fund), and tokens representing ownership in that structure are issued on-chain. Each token represents a fractional interest in the underlying property. Income from rents flows through to token holders. Sale proceeds flow through when the property is sold.

Type 2: Property-backed fund tokens. A diversified fund holds multiple properties. Tokens represent shares in the fund. Investors get diversified exposure without selecting individual properties. Income and appreciation flow through to token holders proportionally.

Type 3: REIT-style tokens. Tokenized versions of traditional REITs. Provides equity-like exposure to real estate sectors (residential, commercial, industrial, etc.) through blockchain-native tokens.

Type 4: Mortgage and debt tokenization. Rather than equity ownership, these structures tokenize the debt side: mortgages, real estate loans, or debt funds. Investors earn interest income rather than rental income or appreciation.

The variation matters because each structure has different risk-return profiles, liquidity characteristics, and regulatory treatments.

Why Tokenized Real Estate Matters in 2026

Three forces converged.

First, the RWA tokenization category proved scalable. The growth from $5.5B to $29.2B in 16 months demonstrated that tokenized assets can attract real capital. Treasuries led the way; real estate is the next frontier with much larger total addressable market.

Second, regulatory clarity advanced. The CLARITY Act and broader regulatory progression provide clearer paths for tokenized securities. Real estate tokens that meet securities standards have a clearer compliance pathway than was available 18 months ago.

Third, the user experience improved. Early tokenized real estate platforms (2018-2020 vintage) had operational friction, limited liquidity, and unclear regulatory status. The 2025-2026 generation of platforms has matured. Better UX, more liquidity, clearer legal structures.

For crypto holders, tokenized real estate provides several attractive properties: hard-asset backing, income generation, lower correlation to crypto market volatility, and the potential to use crypto wealth (rather than fiat) to acquire real estate exposure.

The Leading Tokenized Real Estate Platforms

RealT

RealT is one of the longest-running tokenized real estate platforms. It tokenizes specific properties (typically residential rental properties in the US) and distributes rental income to token holders weekly or monthly.

Properties are placed in an LLC. Tokens represent membership interests in the LLC. Rental income (net of expenses) is distributed proportionally. When the property is sold, sale proceeds are distributed.

By 2026, RealT has expanded its property portfolio significantly. Minimum investment per property is typically $50-100, making it accessible for retail investors.

Lofty

Lofty is a US-focused tokenized real estate platform. Similar to RealT in structure (LLC-based property ownership, token represents membership interest), with focus on US residential real estate.

Lofty has built a secondary market for token trading, providing better liquidity than purely buy-and-hold structures.

Propy

Propy focuses on the broader real estate transaction infrastructure, including tokenized title and ownership records. The platform handles end-to-end real estate transactions on blockchain, with tokenization as one feature.

Ondo and Other Mixed-RWA Platforms

Ondo Finance (focused on tokenized Treasuries) has expanded its product line to include real estate exposure. Other mixed-RWA platforms are similarly expanding into property tokenization.

Tokenized REIT Tokens

Several platforms now offer tokenized exposure to existing REITs or REIT-like structures. These provide equity exposure to diversified real estate without requiring individual property selection.

How Tokenized Real Estate Compares to Traditional REIT Investment

Traditional REITs have been the standard real estate investment vehicle for decades. Tokenized real estate offers several advantages and a few disadvantages relative to traditional REITs.

Advantages of Tokenized Real Estate

Fractional ownership at smaller minimums. A traditional REIT may have a share price of $50-200. A tokenized property may have token prices of $50 with much lower minimum investment requirements. Specific property exposure at low capital outlay.

Direct property exposure. Tokens often represent specific properties or small property pools. Traditional REITs hold dozens or hundreds of properties. Tokenization allows targeted exposure to specific markets or property types.

Crypto-native settlement. Buy and sell using stablecoins or crypto. No traditional brokerage account required. International accessibility (where regulations permit).

Transparent on-chain record. Ownership and distribution records are on-chain and verifiable.

Disadvantages of Tokenized Real Estate

Lower liquidity than traditional REITs. Tokenized real estate secondary markets are smaller. Selling tokens may take longer than selling traditional REIT shares.

Regulatory uncertainty. While clarity is improving, tokenized real estate still faces some regulatory ambiguity. Traditional REITs have decades of regulatory precedent.

Custody complexity. Token holders need crypto custody. Traditional REITs use familiar brokerage accounts.

Smaller scale. Most tokenized real estate platforms hold smaller property portfolios than major REITs. Diversification within a single platform may be limited.

The Practical Steps for Investing in Tokenized Real Estate

Three concrete approaches.

Step 1: Choose your structure. Decide if you want direct property exposure (RealT, Lofty), diversified fund exposure (tokenized REITs, multi-property tokens), or debt exposure (real estate lending tokens). Each has different risk-return characteristics.

Step 2: Verify the platform's legal structure. Tokenized real estate involves legal entities (LLCs, trusts, funds) holding the underlying property. Verify the legal structure is sound, the custodian is reputable, and the property records are publicly verifiable.

Step 3: Size positions appropriately. Tokenized real estate provides exposure but is less liquid than mainstream crypto. Sizing discipline should reflect this. Most investors limit tokenized real estate to 5-15% of crypto allocation, with the rest in more liquid positions.

For traders managing tokenized real estate positions alongside spot crypto holdings, a platform like Altrady (connecting to 19+ exchanges) provides unified portfolio tracking. The platform aggregates positions across exchanges, useful for managing the broader portfolio while specific tokenized real estate positions live on their respective platforms.

The Risks of Tokenized Real Estate

Liquidity risk. Tokenized real estate is less liquid than traditional REITs. Exit liquidity may be limited, particularly during market stress. Plan for longer holding periods than typical crypto positions.

Legal structure risk. The underlying legal entity (LLC, trust, fund) must remain in good standing. Operational failures (compliance lapses, tax issues, custodial failures) can damage token value independently of the underlying property's value.

Property-specific risks. Real estate has its own risks: vacancy, repairs, market downturns, natural disasters, regulatory changes. Single-property tokens concentrate these risks.

Regulatory risk. Tokenized real estate may face changing regulatory treatment. The asset class is securities in most jurisdictions, but specific application of securities laws continues to evolve.

Platform risk. The platform that operates the tokens must remain solvent and operational. Platform failures could disrupt token operations even if underlying properties are sound.

Currency risk. Properties are typically denominated in dollars. Token prices may diverge from underlying property value due to crypto market dynamics or platform-specific factors.

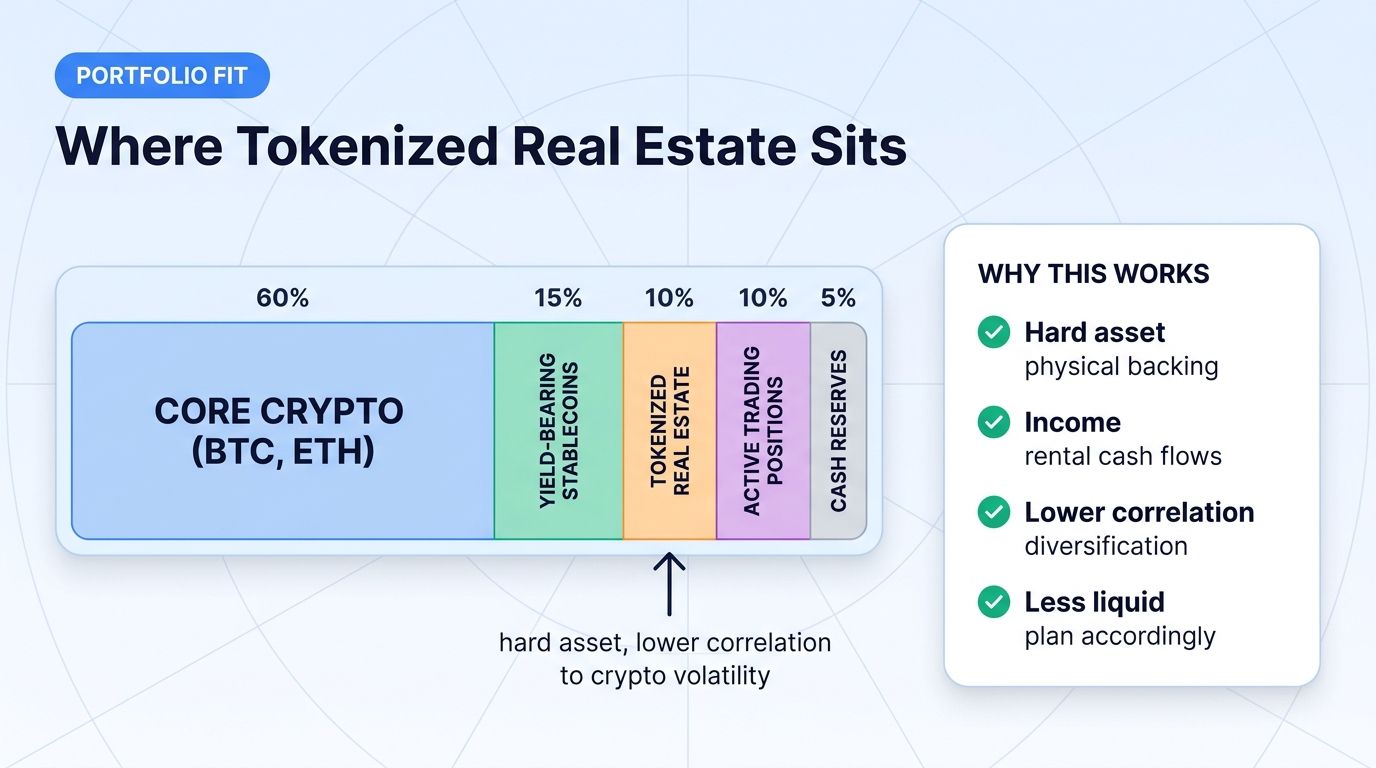

How Tokenized Real Estate Fits Into a Crypto Portfolio

A practical framework:

- Core crypto holdings (BTC, ETH): 50-70% of crypto allocation. Foundational exposure.

- Yield-bearing stablecoins (USDY, USDe, sUSDS): 10-20%. Stable yield while waiting for opportunities.

- Tokenized real estate: 5-15%. Hard asset exposure with income potential. Lower correlation with crypto.

- Active trading capital: 10-20%. Spot, derivatives, DeFi positions.

- Cash for opportunistic adds: 5-10%.

The tokenized real estate allocation provides diversification from crypto-pure exposure. During crypto bear markets, real estate tokens may hold value better than spot crypto due to underlying property cash flows.

Tokenized Real Estate vs. Buying Crypto Then Mortgaging

A specific use case worth understanding.

With the FHFA's May 2026 directive allowing crypto holdings to count as mortgage assets, traders now have multiple paths to real estate exposure:

Path A: Tokenized real estate. Hold tokens representing fractional property ownership. Receive rental income. Sell tokens for liquidity. No leverage, no debt obligation.

Path B: Hold crypto, mortgage a property. Use bitcoin or other crypto as qualifying asset for a traditional mortgage. Acquire a physical property. Pay mortgage over time. Build equity in the physical property while keeping crypto positions intact.

Path C: Hybrid. Hold core crypto, smaller tokenized real estate allocation for diversification, and use crypto as qualifying asset for an eventual physical property purchase.

Each path has different risk-return profiles, tax implications, and operational complexity. Most investors who care about real estate exposure use a combination depending on their stage of life, capital availability, and tax situation.

FAQ

How much income do tokenized real estate tokens pay?

Yields vary significantly by platform, property type, and market conditions. US residential tokenized properties typically yield 5-10% annually in rental income before appreciation. Commercial property tokens may yield 6-12%. International properties yield more in some jurisdictions but carry additional currency and regulatory risk.

What happens if the underlying property loses value?

Token value reflects the underlying property value. If the property declines (market downturn, area depreciation, structural issues), token value declines proportionally. Income may also decline if rental rates decrease. This is fundamental real estate risk, not specific to tokenization.

Are tokenized real estate tokens securities?

In most jurisdictions, yes. The tokens represent equity interests in legal entities that own property. They typically meet the definition of investment contracts and are treated as securities for regulatory purposes. The CLARITY Act and similar regulatory frameworks are clarifying how tokenized securities are treated, which should reduce ambiguity over time.

Can I use crypto to buy tokenized real estate?

Yes. Most tokenized real estate platforms accept USDC or other stablecoins for purchase. Some accept BTC and ETH directly, often with on-the-fly conversion to stablecoins. The ability to use crypto directly is one of the structural advantages over traditional REIT investing.

Can I trade my tokenized real estate alongside crypto on Altrady?

Tokenized real estate positions typically live on the issuing platform's secondary market (RealT, Lofty, etc.) rather than on standard crypto exchanges. However, Altrady connects to 19+ exchanges where you manage the rest of your crypto portfolio. For the tokenized real estate portion, you would use the issuing platform directly. Altrady provides the unified view for your broader exchange-held crypto positions.

Conclusion

Tokenized real estate represents one of the most significant frontier categories in the broader RWA tokenization story. With the category growing from $5.5B to $29.2B in 16 months, and total addressable market in the $300+ trillion range, the upside is substantial.

For traders, the practical takeaway is this: tokenized real estate provides hard-asset exposure with income generation, lower correlation to crypto volatility, and a path to participate in real estate without traditional brokerage relationships. The category is still early, and risks (liquidity, regulatory, platform) require careful sizing discipline.

The longer-term trajectory looks structural. As regulatory clarity improves (CLARITY Act, FHFA directives), as platforms mature, and as institutional capital recognizes the on-chain real estate category, the category should continue scaling. The biggest beneficiaries will be the platforms that build durable operating infrastructure and the early-positioning investors who acquire exposure before the category fully reprices.

The next 12-24 months will produce decisive data. Continued growth from $29B toward $100B+ would mark tokenized real estate as a mature crypto category. Stagnation or regulatory pushback would slow the thesis. Either way, the category is now worth serious attention from any trader thinking about long-term portfolio construction.